OpenAI Plans Delaying IPO Until 2027, Blames SpaceX

One month ago, during the height of the tokenmaxxing craze - when companies were spending ridiculous amounts of money, in many cases without knowing they were even doing so, just to test out the latest agentic craze - first OpenAI and then Anthropic rushed to announce they will follow in the footsteps of the SpaceX IPO, and were planning (or rather hoping) to go public in the next quarter or two. To validate its euphoric IPO dreams, Anthropic even trotted out a lafughable ARR of $47 billion, a number which besides being laughably incoherent and a non-GAAP mish-mash of adjustments and double counting, also took advantage of said tokenmaxxing frenzy.

Then following a furious blowback against said tokenmaxxing which has seen a collapse in agentic spending and an aggressive shift to much cheaper Chinese models, we said two weeks ago that we are eagerly awaiting Anthropic's new ARR, one which reflects the revulsion to Claude's stratospheric token costs.

Meanwhile, Anthropic quietly annualized the one-time bumper revenue from Feb-May on the agentic splurge when nobody had any idea what they were paying, to come up with the ludicrous $47BN ARR.

— zerohedge (@zerohedge) June 11, 2026

Let's see what ARR is next month after clients finally checked their token bills.

And while we wait, Anthropic's biggest competitor, OpenAI - which unlike its peer has been far less vocal about its latest annualized revenue numbers - appears to have realized that going public at a time when agentic spending is suddenly in freefall (Goldman's best "efforts" to predict 120 quadrillion monthly tokens by 2030 notwithstanding) may not be the best idea, and according to the NYT is now leaning toward punting its IPO until next year in hopes that the AI bubble will be even bigger next year.

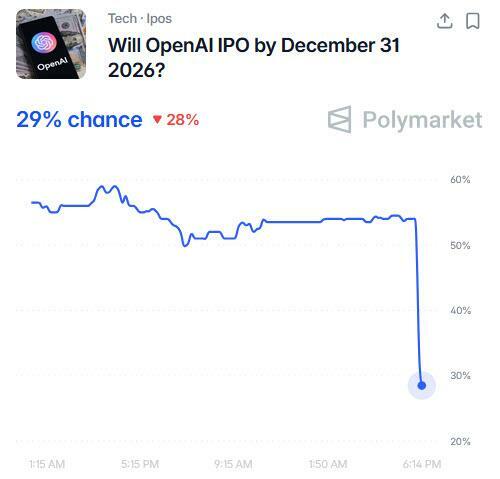

OpenIA's odds of a 2026 IPO promptly tumbled on Polymarket, and were last below 30% from over 50% before the report.

So what is going on, and how did OpenAI - which earlier this month said it had filed confidential paperwork with securities regulators to kick off the process for going public, but it did not commit publicly to any time window - frame the delay so it doesn't sounds like it rushed out its plans to IPO on a one-time bumper revenue burst, only to reverse them as the overpaid agentic euphoria has fizzled?

Why blame Elon of course.

The NYT reports that when the ChatGPT maker hired bankers and lawyers with an eye toward IPOing as soon as the third or fourth quarter of this year, Sam Altman pushed those advisers to find a way for the start-up to be valued at $1 trillion, up from the company’s last private valuation of $730 billion.

OpenAI’s advisers presented company executives with the option of waiting until 2027 to go public with a $1 trillion valuation, or lower the targeted valuation for a quicker IPO, which would be a disaster as the IPO would effectively admit that OpenAI can't keep up with the growth rate of Anthropic which a month ago raised $65 billion in a $965 billion private funding round. Altman responded that any change to the trillion-dollar valuation was a nonstarter.

But, the report goes on, "a cascade of recent developments has caused OpenAI’s executives to shift away from their most aggressive aspirations" and the primary scapegoat is Elon Musk’s, and specifically the performance of SpaceX after its I.P.O. this month. "It was the largest ever, raising more than $85 billion and reaching a valuation of $1.77 trillion on its debut. Since then, SpaceX’s stock has been on a downward slide, as shares slumped to $153 at the end of the trading day on Thursday after reaching a high of $202 last week."

Realizing it would look very stupid if it just blamed the very same company that prompted it to rush its IPO in the first place, the NYT also blamed global markets which "have also been choppy in recent weeks, with tech stocks dragging down indexes as investors question whether AI companies will live up to their sky-high promises."

Nowhere in this above is there a mention of the only thing that actually does matter to investors: the financials, and one can only imagine what is going on there after the early Q2 "tokenmaxxing" agentic burst which has now fizzled. OpenAI said this year that it was generating $2 billion in revenue each month but we are patiently waiting for an update now that the latest series of open Chinese models offer 95% of the US frontier performance for 10% of the price (as discussed in "Answering The "Trillion Dollar Question": Are China's AI Models A Better Value Than US Models").

It's not just China: OpenAI faces acute pressures at home too. Anthropic, which offers a Claude Code tool for creating sophisticated software code, has been far more successful in selling its service to enterprises (at least until the tokenmaxxing fiasco). At the same time, Google’s Gemini, the tech giant’s flagship consumer AI product, has become popular with users.

The NYT however is correct that OpenAI’s postponing its IPO plans - for whatever reason - will disappoint Wall Street and Silicon Valley, especially not if but when its main rival Anthropic, which has been in very hot water with the Trump admin for months, does the same.

There's more.

Besides creating SpaceX strawmen, OpenAI is also grappling with other issues. Late last year, CFO Sarah Friar said it was not pursuing an I.P.O. at the time and was focusing on shoring up its finances. However, since then the company has done just the opposite as it has continued to pour money into data centers and computing power, with no indications of slowing down.

Some OpenAI executives appeared to have changed their minds about an IPO just a few months after Friar said the company was not looking to go public. The Wall Street Journal reported that the company planned to go public by the end of 2026. That surprised some employees because they thought the company was not on a strong enough financial footing.

The company has also been spending like a drunken sailor on marketing and recruiting high-profile engineering talent from companies like Meta and Google. Realizing that it is losing market share to both Anthropic and Chinese open-sourced models, ChatGPT is also searching for other lines of revenue, including dabbling with placing ads inside ChatGPT and striking e-commerce deals with companies like Shopify and Stripe that would allow people to buy things from online stores directly inside ChatGPT.

The biggest problem facing OpenAI, however, is that growth has plateaued: after years of surging downloads of ChatGPT’s consumer app, those numbers have slowed and continue to hover around 900 million users, surprising investors who believed the company would easily hit one billion.

And the wildcard is now that the US government is actively throttling the latest frontier models over concerns they may hack sensitive government agencies, today the Information reported that OpenAI is releasing its latest GPT-5.6 model only as a limited preview to a small group of partners. The reason, according to Sam Altman: the U.S. government asked it to. Altman reportedly told staff that the government will be "approving access customer by customer" during the preview period, with a broader release potentially following a couple of weeks later. This comes after Anthropic took a similar path with Mythos, and after the White House forced Anthropic to withdraw Fable and Mythos over national security concerns.

And now that the "uncorruptible" Trump admin is actively involved in picking winners and losers in the frontier model race, both OpenAI and Anthropic will watch their ARR collapse as most enterprise clients realize they will have better productivity gains by going with the latest Chinese models which, paradoxcially, are now easier to access in the US than domestic made versions.

Tyler Durden Fri, 06/26/2026 - 07:25

via Reuters

via Reuters

via US Navy

via US Navy

The Supreme Court in Washington on June 23, 2026. Madalina Kilroy/The Epoch Times

The Supreme Court in Washington on June 23, 2026. Madalina Kilroy/The Epoch Times A 12-year-old boy watches YouTube on his smartphone on March 27, 2026. Ulet Ifansasti/Getty Images

A 12-year-old boy watches YouTube on his smartphone on March 27, 2026. Ulet Ifansasti/Getty Images via Reuters

via Reuters

Recent comments