Futures Flat As Traders Brace For Weekend Iran Escalation

US equity futures are flat on the final trading session of the week, with Tech lagging, as traders hold off on big bets ahead of the weekend, with the fragile truce in the Middle East keeping geopolitical risk front of mind. Overnight, the US said Iran talks will continue, a positive step amid the recent escalation near the Strait of Hormuz (then again the market never reacted negatively to the latest strikes in the first place). As of 7:45am ET, S&P futures are flat and Nasdaq futures are down 0.2%; pre-market, Mag 7 stocks are mixed: META +1.8%, MSFT +0.9%, while NVDA and AAPL are down 0.6% and 0.4%, respectively. Notably, META has been outperforming since the announcement of its Muse Spark AI model and its strategy for the cloud business. SemiAnalysis, whose "unbiased", often wrong but never in doubt, views at some point be investigated by a regulator, also struck a positive note on META’s AI development (here). Bond yields are 1–2 bp lower, and USD is mostly unchanged. Commodities are mixed: WTI is down 0.2%; base metals are higher, while precious metals are mostly lower. The US economic data calendar empty for the session. Next week includes June CPI, PPI data. Fed calendar empty for the session.

In premarket trading, Magnificent 7 stocks are mixed with Meta rising 3% after research firm SemiAnalysis posted a positive report on the social media giant’s AI compute business (Microsoft +0.4%, Amazon unchanged, Alphabet +0.1%, Apple -0.4%, Tesla unchanged, Nvidia -0.4%).

- CCC Intelligent Solutions (CCC) jumps 9% after Reuters reports that the insurance software company is exploring a sale.

- Circle Internet Group (CRCL) gains 13% after the stablecoin issuer received approval from the US Comptroller of the Currency to establish “First National Digital Currency Bank, N.A.,” a national trust bank that will offer digital asset services.

- Delta Air Lines (DAL) slips 2.8% after the airline posted second quarter results.

- EquipmentShare.com (EQPT) gains 13% after the company announced a $500 million share buyback.

- Fermi (FRMI ) down -17% after offering $350 million in convertible senior notes

- Twilio (TWLO) climbs 2% as Stifel upgrades to buy on the company’s potential to capitalize on the current AI cycle.

- WD-40 (WDFC) rises 14% after the lubricant spray maker boosted its net sales forecast for the full year.

In other AI news, JPMorgan has built an array of AI-powered investing agents that beat 60/40 portfolio in back-tests. OpenAI and Google confirmed they have been supplying AI services to Singapore-based subsidiaries of Alibaba, Baidu and Tencent, the Financial Times reports. Netflix is said to be considering steps to deal with signs of declining subscriber engagement, according to the WSJ. Bayer sold a minority stake in its contraceptives business to Apollo for €3 billion ($3.4 billion) and will use the funds raised to help cover its ballooning litigation costs tied to the herbicide Roundup. Polymarket is seeking regulatory approval to offer margin trading in the US, which would let users bet on events with less capital upfront.

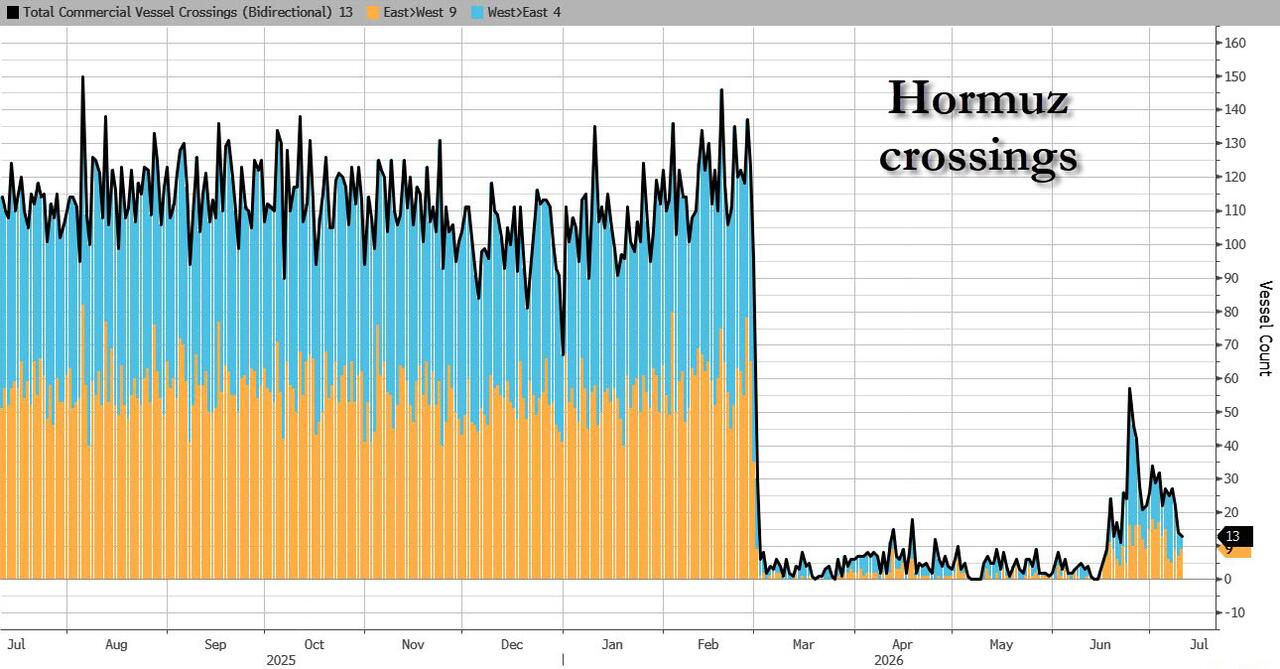

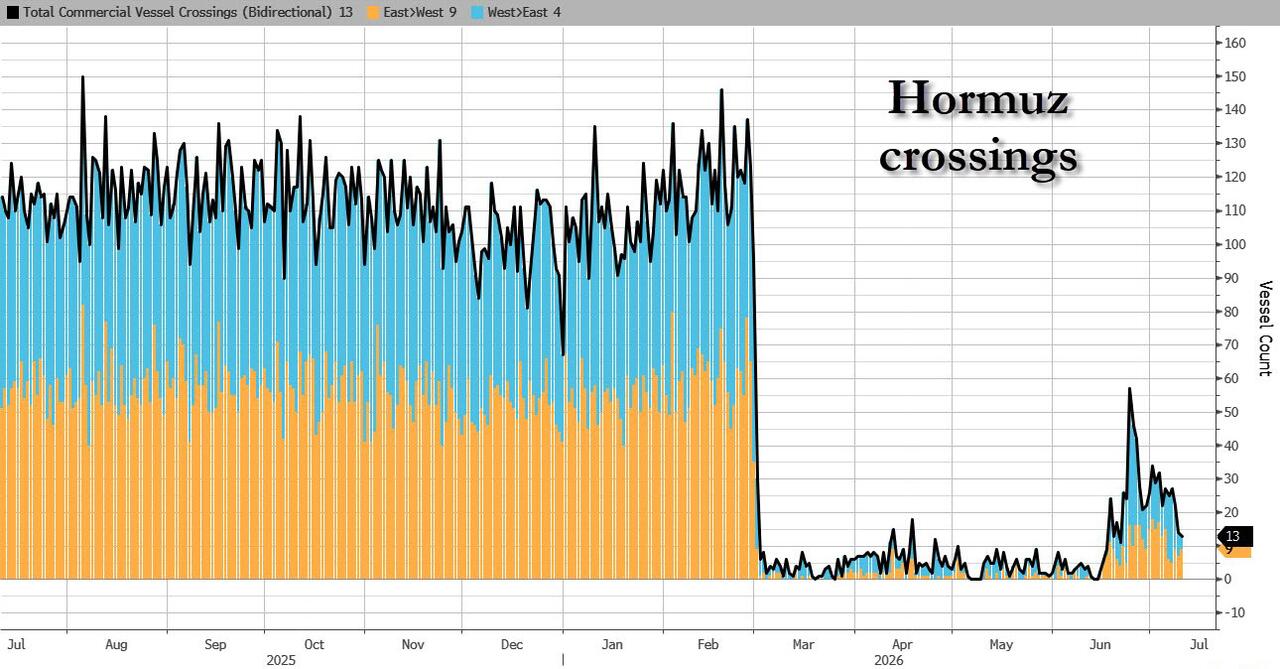

We end a week characterized by thematic rotations, signs of a summer trading lull and low volatility at the index level. Brent crude traded near $76.50 a barrel, swinging between small gains and losses after a volatile stretch. Talks between the US and Iran are continuing despite days of fighting that drove a steep drop in traffic through the Strait of Hormuz. The risk of further escalation is expected to keep investors cautious as they close out the week.

“Over the weekend, discussions between the US and Iran are expected to continue,” said David Manso, chief investment officer at CaixaBank AM. “Oil prices could provide a useful gauge of investor sentiment and expectations regarding the evolution of the situation.”

Yet away from geopolitics, things are about to get busier soon, with Tuesday’s blitz of five major US bank results heralding the start of the earnings season. And speaking of rotation, Lilian Chovin at Coutts in London, notes that the firm has moved a bit underweight US equities. “Other regions are probably better placed right now to navigate the coming few months. Obviously by reducing our US exposure, we have reduced our exposure to tech mega cap.” The Coutts team remains positive on the AI theme, he explains. “It’s more nuanced than people selling tech to go into defensive sectors. We’ve seen a rotation within tech, caused by some noise around semiconductors.”

After an unprecedented rally in chipmakers and other AI buildout stocks helped markets shrug off higher oil prices and elevated bond yields, the bar is now high for companies to justify their lofty valuations. For hyperscalers, the onus is on proving that the spending can generate strong returns.

“What remains to be confirmed is whether growth can hold up despite that pressure, with the AI capex cycle continuing to support investment, revenues and earnings,” said Florian Ielpo, head of macro at Lombard Odier Investment Managers. “Expectations are high, but the real test is whether earnings can keep validating the expansion story.”

This morning another company capitalized on the chip bubble when SK Hynix raised $26.5 billion in its ADR offering, the largest ever US first-time share sale by a foreign company. The company sold 177.9 million ADRs for $149 apiece, each equivalent to a 10th of a Seoul-traded common share. Hynix’s US debut is set to spur a wave of leveraged ETF product launches.

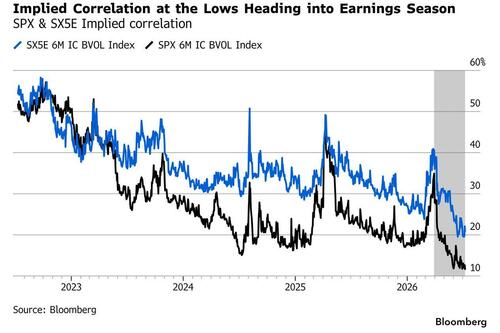

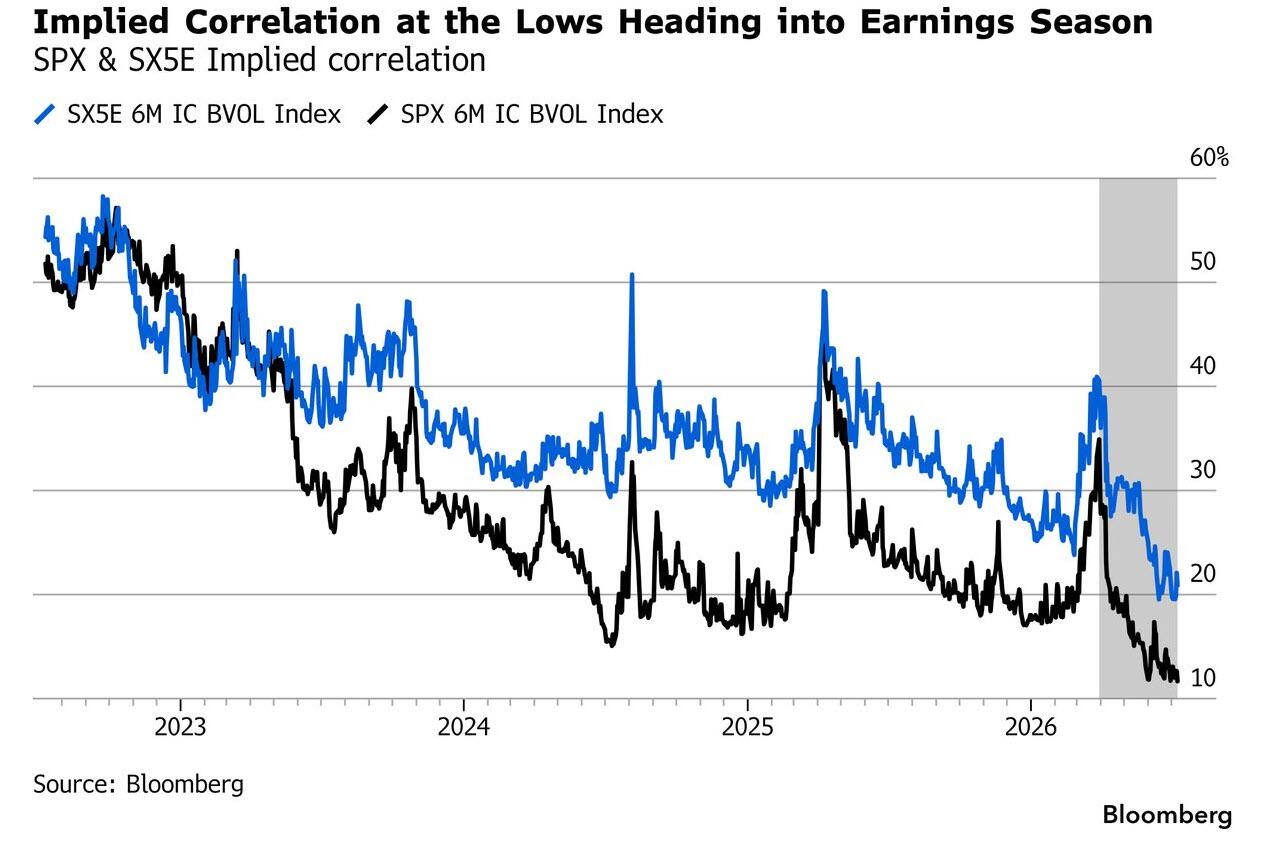

Analysts have upgraded S&P 500 earnings estimates ahead of the second-quarter reporting season, setting the bar high in “an atypical move,” according to HSBC strategists. The Street now expect profits to rise 22% from a year earlier, the highest in the post-pandemic period. Meanwhile, with Q2 reports due shortly, an interesting set-up is emerging between earnings season expectations and headline risk, notes Bloomberg’s equity derivatives specialist Christian Dass. Persistently low implied correlation leaves the VIX vulnerable to a sharp repricing if markets become increasingly driven by macro headlines rather than stock specific fundamentals.

In politics, Trump fired two Democratic members of the US Election Assistance Commission, while the Republican member resigned. Graham Platner’s exit from the Maine Senate race has set off a scramble to find a replacement to take on Republican incumbent Senator Susan Collins, with at least six Democrats entering the field.

In other assets, carry trades are seeing the most compelling backdrop in more than two decades, according to Goldman Sachs, while an unprecedented divergence in the oil-market crack spread gauge are prompting Vanguard to buy insurance against stickier-than-expected US inflation.

Trade during the European session has been indecisive and non-committal alongside a particularly slow news cycle. The Stoxx 600 has oscillated around the unchanged mark: tech and energy sectors are the worst performers, while telecoms and miners are the biggest gainers. Here are some of the biggest movers on Friday:

- EasyJet shares jump as much as 15% after the budget airline received a fresh bid from private equity firm Apollo that beats a rival proposal from Castlelake. The shares remain below both offer prices.

- Vodafone shares soar as much as 14% after its biggest shareholder Emirates Telecommunications Group agreed to sell its entire 16% stake in the firm to a vehicle controlled by billionaire Xavier Niel.

- Voestalpine, Salzgitter and ArcelorMittal rose after JPMorgan upgraded the steel producers. The bank says it expects 2Q reporting to focus on the impact of cuts to EU steel imports and import tariffs effective from July, which have the potential to transfer demand to EU steel producers.

- EMS-Chemie shares gain as much as 3.5% after it reported better-than-expected first-half sales and profit and raised its net sales forecast for the year.

- Hays shares rise as much as 13% after the recruitment company reported stronger-than-expected fourth-quarter fees and forecast full 2026 profit to be at top end of the consensus range.

- St James’s Place shares fall as much as 7% after Financial News reported that one of the wealth manager’s largest advice firms has decided to exit the group, spotlighting ongoing retention troubles.

- Duerr shares fall as much as 4% as Berenberg downgrades the German stock to hold from buy and slashes its price target almost in half, citing dependency to automotive original equipment manufacturers.

- Glenveagh Properties drops as much as 5.1% after being downgraded at Deutsche Bank, as analysts believe the Irish housebuilder is fairly valued following recent gains.

- Troax shares fall as much as 6.6% after Berenberg downgraded the Swedish maker of machinery parts and warehouse fittings to hold from buy, citing a tough automotive end-market and the likelihood of a slow margin recovery.

The mood in Asia was more upbeat with the MSCI APAC index up 0.8%, boosted by a rally in tech shares. Asian stocks climbed, boosted by a rally in tech shares amid optimism ahead of the US listing by South Korean chipmaker SK Hynix. The MSCI Asia Pacific Index jumped as much as 1.7%, the most in a week. Shares of Samsung Electronics and SK Hynix were the top contributors to the benchmark’s advance and led a 5% surge in the Kospi. Japan’s Nikkei 225 was up almost 2%. SK Hynix raised $26.5 billion in its American depositary receipt offering, powering through recent volatility in global semiconductor stocks. Meanwhile, Samsung Electronics’ Executive Chairman Jay Lee is seeking to meet with Nvidia’s Jensen Huang in the US late July to discuss the former’s investment plans in South Korea’s southwest area, according to a media report. Elsewhere, trading in Taiwan was halted as a strong typhoon approached the island. Japan called on its pension funds, which include one of the world’s largest, to invest in domestic assets. Here Are the Most Notable Movers

- Shares of Japanese wafer maker Sumco rallied as much as 15% to hit their upper daily limit after Micron’s plan to invest in Taiwan’s GlobalWafers was seen as a sign of rising demand in the sector.

- Lenovo’ shares rise as much as 9.2% after Morgan Stanley upgrades the Chinese device maker and more than doubles the price target, citing its ability to pass through higher component costs amid AI-driven demand.

- Zhipu shares drop as much as 9.7% in Hong Kong, paring a sharp three-day rally, after Goldman initiated coverage at neutral, saying their valuation fairly reflects the competitiveness of the company’s AI models.

- Mitsubishi Motors shares climbed as much as 17%, the most since December 2024, after the vehicle maker announced a tie-up to produce humanoid robots with a Tokyo-based startup.

- Fast Retailing shares slipped as much as 3.7%, the most since May 12, after the Uniqlo owner’s 3Q earnings beat was seen as priced in

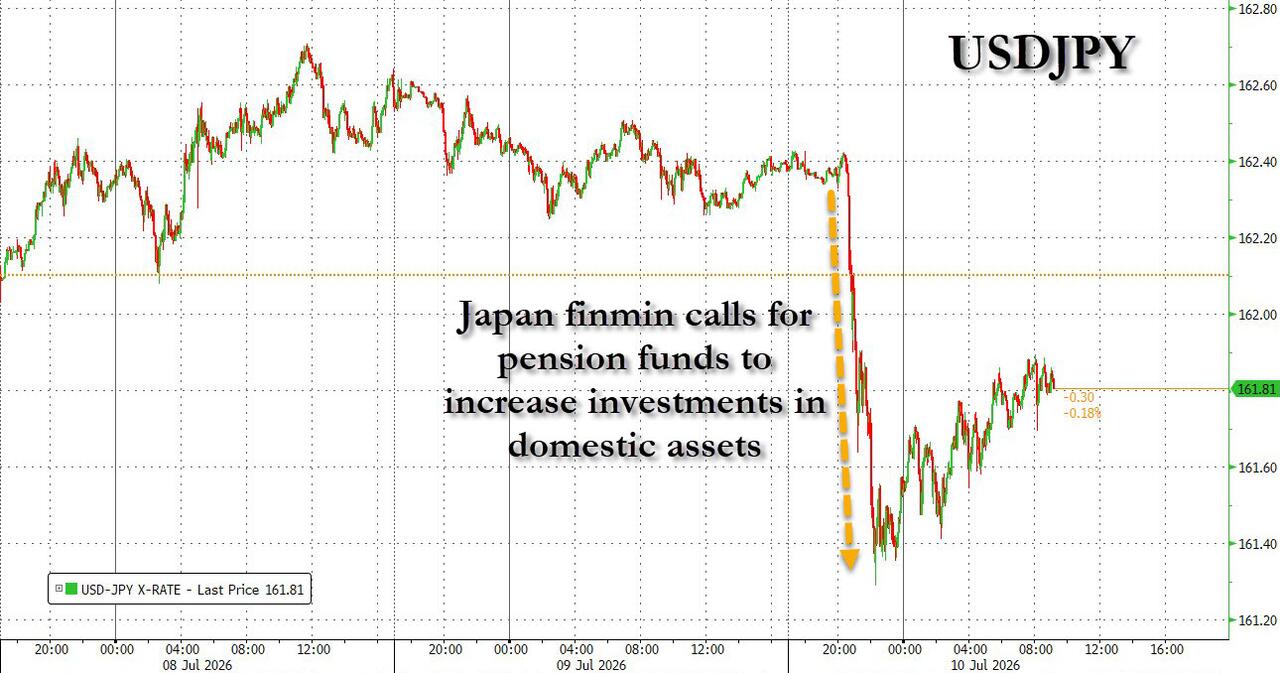

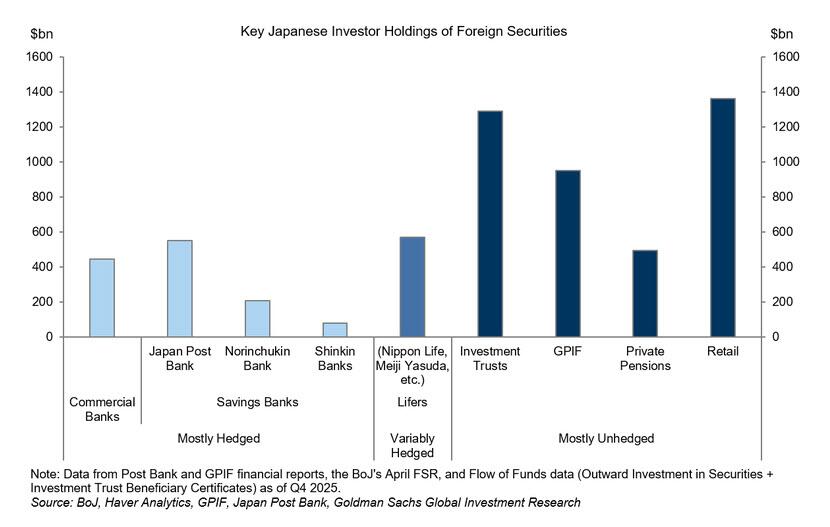

In FX, the dollar dipped 0.1% in a third straight day of losses. Bonds extended a rebound, with the yield on 10-year Treasuries falling two basis point to 4.54%. The yen outperformed major currencies, rising 0.4% after Japanese Finance Minister Satsuki Katayama said the government wants pension funds to increase investment in domestic assets.

In rates, treasuries are slightly richer across the curve following similar price action across European bonds with oil prices steady. US yields are 1bp-2bp lower with curve spreads within a basis point of Thursday’s close, 10-year near 4.535% with bunds and gilts in the sector also about 1.5bp richer on the day. During Asia session, yen and JGBs advanced after Japan’s Finance Minister Satsuki Katayama called on pension funds, including the GPIF, to invest in domestic assets. Long-end JGB yields ended more than 10bp lower. US session has no major scheduled events. IG dollar issuance slate empty so far. Four borrowers priced $2.25b in new US investment-grade bonds Thursday, pushing weekly volume through $51b and more than double forecasts. Issuers paid about 2bps in new issue concessions on deals that were 4.2 times covered.

In commodities, Brent crude futures are down 0.5% and around the $76/bbl mark with traders awaiting further directional clues from events in the Middle East. WTI crude oil futures little changed as US and Iran continue talks despite a flare-up in fighting. Precious metals are on the back foot with spot gold and silver down 0.6% and 0.8% respectively. Bitcoin is higher by 1.5%.

The US economic data calendar empty for the session. Next week includes June CPI, PPI data. Fed calendar empty for the session. Next week Federal Reserve Chairman Warsh testifies before the House Financial Services and Senate Banking Committees on its Semi-Annual Monetary Policy Report.

Market Snapshot

Top Overnight News

US-Iran negotiations on a permanent peace deal are continuing, according to an American official, despite two days of clashes that threatened to unravel the ceasefire. BBG

Israel shared new intelligence with the U.S. that it said indicated a fresh Iranian plan to kill President Trump, people familiar with the matter said, a finding that would mark an escalation in the war between Washington and Iran. This news that comes just 24 hours after Trump unexpectedly switched back to the old Air Force One for his return flight from the NATO summit in Turkey as a “security precaution” (the New Air Force One doesn’t have the same security features as the old one). Iran for years has vowed openly to retaliate against Trump for the assassination of Qassem Soleimani, who was a top general in the Islamic Revolutionary Guard Corps, in the president’s first term. WSJ

The UAE boosted crude production to an all-time high last month, pumping 4.1 million b/d on average in June. IEA

Global diesel market faces a significant supply crunch as Russia bans exports due to domestic shortages following Ukraine strikes. FT

Japan’s Finance Minister, Satsuki Katayama, sparked a jump in the yen on Friday when she said the government would pursue policies to encourage pension funds to buy more Japanese assets. Japan’s biggest public pension fund will likely ignore the call to boost domestic investment, at least in the short run, because of strict rules governing asset allocation and its public mandate. BBG

Japan’s producer prices picked up in June to the fastest pace since early 2023, reinforcing the case for the BOJ to keep hiking rates. BBG

Taiwan halted trading on its stock exchange and closed schools as Typhoon Bavi approached the island. TSMC postponed its monthly sales disclosure to Monday. BBG

South African economic growth is on an upswing as efforts to improve governance and critical infrastructure are lifting bottlenecks that have held it back for years, according to Standard Bank’s chief economist. BBG

SemiAnalysis thinks Meta should be talked about alongside OpenAI and Anthropic as the top three frontier AI labs in the world (of the hyperscalers, SemiAnalysis thinks Meta, not Google, has the best chance of catching up with Anthropic and OpenAI). SemiAnalysis, which may or may not have a conflict of interest

Trump fired two Democratic members of the US Election Assistance Commission, while the Republican member resigned.

Graham Platner’s exit from the Maine Senate race has set off a scramble to find a replacement to take on Republican incumbent Senator Susan Collins, with at least six Democrats entering the field: BBG

A more detailed look at global markets courtesy of Newsqauwk

Asia-Pac stocks traded entirely in the green, as they followed the tech-led gains seen stateside. Military strikes continued on Thursday, but energy prices and equity markets seemed to have brushed it aside and instead took a stronger liking to President Trump’s comments, in which he said Iran had reached out to the US and wanted to make a deal, easing concerns over a further escalation that could threaten energy infrastructure. To note, the Taiwan markets were closed due to the typhoon, and worries of the typhoon hitting China and Japan. ASX 200 initially opened with modest losses but has since reversed and printed modest gains. Metals & Mining topped the sector pile, cutting 4 consecutive days of losses, while Health Care was the sector laggard. Nikkei 225 gained, with SUMCO leading the way as it benefited from the semiconductor strength stateside. On the earnings front, Seven & I and Fast Retailing both posted strong earnings and raised their FY guidance; however, shares traded lower after highlighting the effects of a weaker yen. KOSPI surged, helped by gains in Samsung Electronics while SK Hynix shares traded choppy ahead of its US ADR listing. The choppiness in SK Hynix comes as investors position themselves for the ADR, with analysts stating that the US ADR may be preferred over its domestic listing, due to US ADRs commonly trading at a premium (typically at a 5-15% premium). Shanghai Comp. and Hang Seng were firmer, with another set of IPOs in Hong Kong, resulting in 15 listings this week. Today, markets were focused on Nexchip Semiconductor. The IPO price was set at HKD 32.30/shr, and shares rose at the open and briefly topped HKD 36/shr but have since come off.

Top Asian News

- Japanese Finance Minister Katayama said they are to pursue steps to promote investment in Japanese assets by GPIF and others.

- Japanese Finance Minister Katayama does not comment on specific bond yield levels; specific monetary tools are up to the BoJ, closely monitoring economic indicators and market situations. Important that the government position secures market confidence. Will ensure fiscal sustainability to gain market trust. BoJ can adjust monetary policy regardless of what the government said. Predicts gradual increases in interest rates as the government is engaged in a proactive fiscal policy. Want to speed up discussions on expansion of JGB products targeting households.

- Japan's GPIF spokesperson said they are aware of Finance Minister Katayama's comments but declines to comment.

- Japan's Economy Minister Kiuchi said the government has consistently communicated its stance of taking policy that heeds to fiscal sustainability.

European bourses (STOXX 600 -0.1%) began the session on a weaker footing despite APAC optimism ahead of SK Hynix’s US debut (KOSPI +2.5% at close). Geopolitical newsflow quietened overnight, as such energy benchmarks are off best levels with Brent around USD 75/bbl. IBEX continues to outperform after it slumped earlier in the week (also has more defensive composition), while tech heavy AEX is the worst performer as top constituent ASML looks to SK’s ADR debut. European sectors opened with a positive bias and continue this way. Comms and Travel/Leisure outperform, Tech and Energy are the laggards for the above factors. In terms of individual movers, Infineon (-2.7%) said it is raising prices in some segments; EasyJet (+14%) agreed to a GBP 5.7bln takeover by Apollo at 715p/shr; Vodafone (+11%) French telecom tycoon Niel acquired E&’s stake for a GBP 0.15/shr premium.

Top European News

- UK Chancellor Reeves is to announce a new City "skills compact" that will commit financial firms to retraining thousands of workers for the AI revolution, The Guardian reported.

FX

- G10s are mixed against the Buck. JPY leads after FinMin Katayama touted measures to promote domestic inflows, Kiwi continues to eek gains post-RBNZ as markets look to price a cumulative 50bps tightening by year end and NOK is the worst performer after broadly cool inflation data.

- USD a touch weaker as JPY firms alongside the tempered recent Gulf updates. Geopolitical newsflow quietened overnight, with energy benchmarks off best levels with Brent around USD 75/bbl, about 5 Bucks off the week’s highs. DXY slipped throughout APAC as the JPY firmed, but found buyers below 21DMA at 100.85 which has proven support in recent sessions.

- JPY digests updates from FinMin Katayama who said she was to pursue steps to promote investment in Japanese assets by GPIF and others. This, on the face of it, would be a textbook tactic to encourage domestic investment and passively limit outflows, especially with a large composition (50%) of pension funds allocated to foreign investments. Several strategists note this is a positive sign in attempts to shore up the currency; though CapEco said “Much of its domestic bond portfolio is invested passively, and shifting more assets into domestic bonds would come at a sizeable fiscal cost if it requires selling equities”, and others highlight Katayama is not in a position to direct changes, it would be under the jurisdiction of the Labour Ministry. USD/JPY gradually trundled lower from a 162.50 peak, to mark a trough below 161.30 (session low 161.28), with a modest kneejerk lower on not-too-surprising BoJ sources. ING notes the JPY-funded carry keeps risks to the upside for the pair.

- NOK is the clear underperformer vs. both the USD and SEK after the soft inflation data series. Most metrics cooled beneath expectations, core Y/Y the sole figure rising above consensus, albeit unch. from May. CPI-ATE, the Norges Bank’s preferred gauge of inflation fell was 2.9%, well below the Bank’s estimate of 3.3%, will likely provide conviction for doves with the bank likely to remain on hold in the August meeting; then tighten in September should the next (August) CPI metrics not provide a dovish surprise. NOK/SEK fell from a 0.9940 peak to mark a trough at 0.9882. 8th July low at 0.9861 is the next level below.

- South Korean Forex Authority said USD/KRW market remains misaligned with economic fundamentals.

Fixed Income

- Overall, fixed benchmarks are firmer in reaction to the modest but increasing pullback seen in the energy space overnight and as JGBs lead on domestic updates.

- JGBs got to a high of 127.76 in the European morning, continuing the overnight rally after comments from Japanese Finance Minister Katayama, who said that pension funds should be encouraged to invest more in the domestic market. Commentary that underpinned Japanese assets across the board, and sent the 10yr yield lower by around 16bps on the day, down to 2.71% and now essentially flat on the month, reversing from the 2.89% YTD high.

- Commentary that also lifted peers at the time. While the shift would be a positive for the Japanese market generally, there are a few unknowns, most pertinently being whether Katayama can make such an announcement as the GPIF is under the Labour Ministry, not the Finance Ministry. As such, for FX in particular, there is an argument that Katayama’s commentary is conducting another form of jawboning, and therefore the move may well fade in the days/weeks ahead, unless a relevant official to the GPIF (i.e. Ueno, or PM Takaichi) backs the shift publicly.

- USTs got to a 109-12 peak in the early morning, as energy hit a low and the JGB-driven move topped out. Since, newsflow has been particularly light with the market essentially waiting for a resumption of negotiations or strikes, though as is often the case we might not get clarity on the next step until the weekend.

- Bunds followed suit, peaking at 125.74 with gains of around 35 ticks. Specifics limited. Continued focus on the EU funding plans, and the lack of agreement on the next 7yr plan is arguably supporting EGBs for net-contributing nations, as no agreement would see the current EUR 1.4tln figure continue as opposed to the planned uplift to EUR 2tln.

- Gilts opened lower by a few ticks, before then swiftly moving above the 88.00 mark to a 88.07 peak, in-fitting with the above. Action that leaves it just above Wednesday’s high but someway shy of the 88.93 opening level at the start of the week. Last night the first tally was done for the Labour nominations, and while the count theoretically leaves space for a challenger it is not realistic and therefore Burnham is now formally, for all intents and purposes, the incoming UK PM.

- Italy sold EUR 7.5bln vs exp. 6.0-7.5bln 3.00% 2029, 3.35% 2033 & 3.95% 2041 BTPs.

- China's MOF sold 2-year and 3-year bonds. 2-year sold at 1.2305%. 3-year sold at 1.2629%.

- Australia sold AUD 900mln 1.75% 2032 AGBs: b/c 3.16x (prev. 4.10x), average yield 4.6189% (prev. 4.1987%).

Commodities

- The geopolitical situation appears to have calmed down this morning, with no fresh reports of strikes on Iran/regional neighbours. However, the situation remains tense given some of yesterday’s actions. Iran reported a couple of strikes at two military bases, but US officials denied any involvement of this. Despite the earlier reports, some Iranian officials denied any explosions taking place.

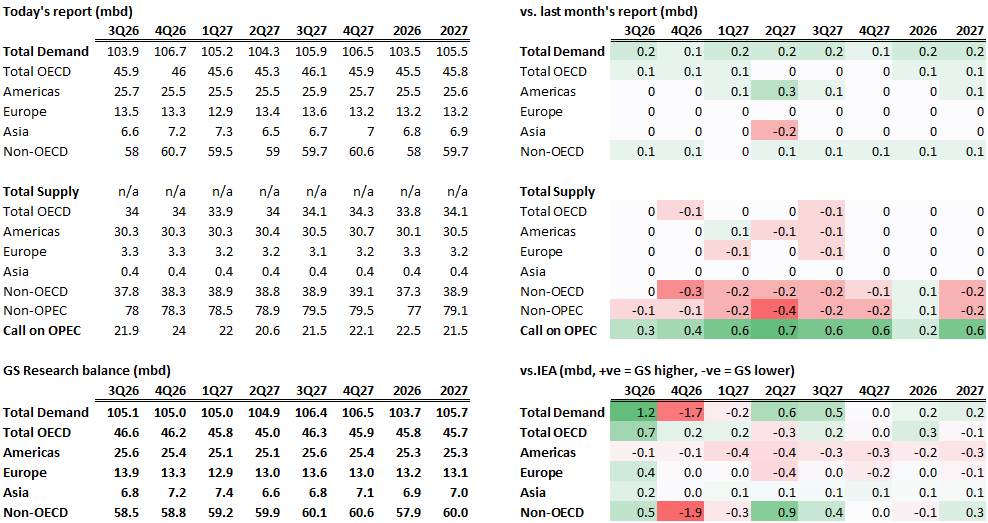

- Despite the recent flare-up, a US official stated that the US remains committed to a resolution with Iran and technical discussions are ongoing. This, alongside the lack of new strikes overnight has led to a bearish bias in crude benchmarks this morning. Brent Sep’26 (-0.2%) is only mildly lower and trades at the towards the mid-point of a USD 75.36-76.95/bbl range. Some mild downticks were seen in the benchmark after the release of the IEA Oil Market Report. It cut 2026 oil demand, noted that the UAE is upping its supply and oil transits are passing through the Hormuz.

- Spot gold (-0.6%) trades lower this morning, hovering on either side of the USD 4.1k/oz mark; currently within a USD 4,094-4,134/oz band. The range today is very thin, amidst the lack of pertinent newsflow and fairly steady USD. Elsewhere, base metals hold a negative bias. 3M LME Copper trades within a USD 13,455-13,562/t range. For aluminium, analysts at Morgan Stanley recently stated that they see a smaller supply deficit in 2026, and likely to move into a surplus from 2027.

- Oman has set its OSP at USD 69.29/bbl for September delivery.

- IEA OMR: forecasts global oil demand in 2026 to fall by 1.05mln BPD (prev. exp. 1.12mln); global oil demand recovery is under way. Global oil demand estimated at 103.46mln bpd for 2026 and is expected to grow by 2mln BPD in 2027 and reach 105.47mln BPD. Oil supply may expand 7.5mln BPD in 2027 if transits improve.

- A fire broke out at two oil product storage facilities due to a UAV attack in the Rostov region, according to the governor; fires are being pushed out in Taganrog's Seaport, reported no injuries.

- Krasnodar task force said a fire has broken out at the Ilsky oil refinery due to the fall of a drone's debris, Interfax reported.

- QatarEnergy set August Marine Crude OSP at Oman/Dubai -USD 5/bbl; Land Crude OSP at -USD 4.50/bbl, according to a pricing document.

- China National Summer grain output reached 150.7mln tonnes, +0.7% Y/Y.

Trade/Tariffs

- China's MOFCOM announces a temporary ban on helium exports.

- US White House announces the adjustment of imports of commercial aircraft, jet engines, and aircraft and engine parts into the US; no immediate tariffs be imposed under section 232 to address the threatened impairment to the national security.

Central Banks

- BoJ reportedly to keep rates unchanged in July but maintain policy guidance and also raise growth outlook, according to sources.

- PBoC injected CNY 20bln via 7-day reverse repos with rate maintained at 1.40%.

- PBoC set USD/CNY mid-point at 6.7989 vs exp. 6.7931 (prev. 6.8036); strongest midpoint since February 2023.

- NBP's Wnorowski said signal about possible motion to cut interest rates in September is premature; do not see space for more than one cut this year.

Geopolitics: Middle-East

- Qatar, Pakistan and other regional mediators are trying to de-escalate tensions between the US and Iran and revive negotiations on a nuclear deal, Axios reported citing sources.

- A member of the National Security Commission of Iran's parliament said the UAE will pay the price for cooperating with America.

- A US official said talks with Iran will continue, Fox's Hasnie reported; The administration is still committed to finding a resolution so technical talks continue to prevent Iran from having a nuclear weapon. Iran's attacks on ships in the streets are acts of terrorism. The MoU is performance-based, and Iran's actions constitute failed performance at an unacceptable level.

- Israel reportedly shared new intelligence with the US that indicated a new Iranian plan to kill US President Trump, WSJ reported citing sources.

- A US official said the US remains committed to a resolution with Iran and technical discussions are ongoing.

- Turkey has decided it will not join the Canadian Defence Bank initiative at this point, sources suggest.

- The Israeli army said "we will continue our operations to eliminate any threat and will not allow Hezbollah to harm us", Al Jazeera reported.

- Al Jazeera reported that Israeli forces are conducting extensive demolitions in southern Lebanon.

- Krasnodar task force said a fire has broken out at the Ilsky oil refinery due to the fall of a drone's debris, Interfax reported.

- Pakistan has begun mediating between Libya's rival eastern and western data centres with the backing of the US and Saudi Arabia, Nikkei reported citing sources.

- Lebanese media reported of new Israeli drone strikes in southern Lebanon, Tasnim reported.

- Four Japanese-linked vessels remain in the Persian Gulf, Kyodo reported.

- Konarak Governor said this area was targeted by enemy fighter jets in two stages on Thursday evening.

Geopolitics: Ukraine

- Ilsky (138k BPD), Russia oil refinery fire has now been extinguished.

US Event Calenadar

- The US economic data calendar empty for the session

DB's Jim Reid concludes the overnight wrap

I was hoping that by now the latest on the Iranian conflict wouldn’t be the lead story but it has of course returned to the top of the headlines this week. The latest is that Bloomberg reports overnight indicate that “technical talks” continue between US and Iranian officials despite the clashes this week. There were also Bloomberg reports that President Trump and PM Netanyahu spoke Thursday according to the PM’s office. To be fair sentiment turned back more positively late Wednesday night when Trump suggested that the Iranians were desperate for a deal. So markets have generally been more positive since.

So for now we can go back to trying to guess whether we’ll wake up to the KOSPI being up or down more than 5%. If you guessed in the positive side this morning you’d be correct as it’s surging +5.11% as I type, after officially entering bear-market territory yesterday. The rally has of course been driven by strong gains in semiconductor stocks with the record-breaking $26.5 billion listing by chipmaker SK Hynix helping to reinforce confidence that the AI investment cycle remains intact. Elsewhere in the region, Hong Kong’s Hang Seng Index (+1.85%) has climbed to its highest level since June 17, while Japan’s Nikkei 225 (+1.77%) is also posting strong gains. The CSI 300 (+0.49%), Shanghai Composite (+0.75%), and S&P/ASX 200 (+0.51%) are also up. US and European futures are down between a tenth and two tenths of a percent though. 10yr USTs are -1.2bps lower trading at 4.54% and oil is fairly flat.

In Japan, long-dated government bond yields are falling and the yen strengthening after Finance Minister Satsuki Katayama indicated that the government intends to encourage pension funds, including the Government Pension Investment Fund (GPIF), to increase allocations to domestic financial assets. The 20-year JGB yield is down -7.8bps at 3.78%, while the 10-year is -8.7bps lower at 2.778%. The Japanese yen (+0.51%) is rallying for a second consecutive session, trading at 161.54 against dollar as we go to print. There is some scepticism here internally as to whether it'll be easy to encourage domestic pension funds to automatically buy more JGBs. The view is that asset allocations decisions are more slow moving and might actually favour equities first. However for now the move is being seen as a sign that action is being considered.

Ahead of all that, markets saw a bit of a relief rally yesterday, thanks to easing geopolitical fears, decent tech headlines, and a respectable batch of data. So collectively, that helped to power bonds and equities on both sides of the Atlantic, particularly as falling oil prices reassured concerns about a fresh surge of inflation. So by the close, that meant the S&P 500 (+0.81%) and Europe’s STOXX 600 (+0.78%) both advanced, whilst yields on 10yr Treasuries (-4.2bps) and bunds (-0.8bps) also fell back.

Those oil price declines followed headlines suggesting that the escalation between the US and Iran might not prove as serious as initially feared. Most notably, sentiment was supported by comments from President Trump late on Wednesday night, that we mentioned yesterday, saying that Iran wanted “to make a deal so badly”. So when US and European markets reopened yesterday, they were buoyed by the fact that Trump was still talking about some kind of agreement. So that supported oil prices lower, with Brent crude down -2.20% on the day to $76.30/bbl. And in turn, that eased fears around inflation, with the 1yr Euro inflation swap (-9.0bps) falling to 2.05%, after rising 27bps on Wednesday.

This backdrop meant that investors dialled back their expectations for imminent rate hikes again, particularly in Europe. For instance, the amount of ECB rate hikes priced by December came down -8.5bps on the day to 31bps. And over at the Fed, the probability of a hike at the upcoming July meeting fell back from 31% to 24%. So that provided a decent tailwind for sovereign bonds in turn, with yields on 10yr bunds (-0.8bps), OATs (-7.2bps) and BTPs (-7.0bps) all coming down.

Whilst lower oil prices helped sentiment, markets got another boost yesterday from the latest tech headlines, which saw the Philly semiconductor index (+3.06%) post its best daily performance in 3 weeks. That included a very strong gain for Micron (+4.52%), who raised their planned spending on new US plants to $250bn by 2035, which was $50bn on top of previously announced commitments. The rally also saw the SK Hynix ADR officially became the largest foreign company offering as the South Korean chipmaker raised $26.5bn – greater than expected and just ahead of the $25bn previously raised by Alibaba.

So that chip rally helped to lift US equities more broadly, with the S&P 500 (+0.81%) recovering after back-to-back declines on Tuesday and Wednesday. The rally was fueled by investors rotating from defensives industries back into growth and cyclical names. Autos (+2.91%), Tech Hardware (+1.99%), Semis, +(1.90%), and Banks (+1.61%) were the best performing S&P 500 industry groups, while Consumer Staples (-2.04%), Food & Bev (-1.77%), and Household Products (-1.58%) lagged. And in Europe, the STOXX 600 (+0.78%) advanced for the first time this week with a similar rotation from defensives into cyclicals.

Speaking of tech, there was an interesting acknowledgement of AI-driven inflation from New York Fed President Williams. He spoke about the potential for demand driven by AI to raise inflation, and said if it “creates a sustained impulse to demand relative to supply in inflation, I do think that’s the kind of situation where you don’t look through this”. Meanwhile on inflation more generally, he said that if core PCE were at “two-tenths a month in the second half of this year, that would be consistent with my view of a disinflationary process that’s continuing”. But he also said if it were higher, “ that would be a sign of inflation a bit more persistent.”

The other Fed news from yesterday was the release of the leadership teams of the five task forces that Chair Warsh announced to examine the Fed’s current approach and processes. The areas that the Fed are examining are the communications strategy, the use of the balance sheet, the quality and reliance on existing data sources, productivity and jobs, and inflation framework. The teams are mix of former policy makers, academics, and corporate leaders.

Staying on central banks, yesterday also brought the minutes of last month’s ECB meeting, where they hiked rates for the first time since 2023. It spoke of inflation pressures, and said how “Further indirect effects were in the pipeline, pointing to more broadening of inflationary pressures across the economy”. Moreover, there was an acknowledgment that “memories of the 2022 high-inflation episode could make households and firms react more quickly than in the past, increasing the risk that price-setting and wage-bargaining behaviour would adjust.” Interestingly, there was also a discussion about what happened in 2011, when the ECB hiked rates before reversing course shortly after as the sovereign debt crisis became more severe. But the view was there were key differences with that period, including the lack of financial stress.

Finally, the latest US data yesterday offered fresh reassurance on the labour market, with the weekly initial jobless claims coming in at 215k in the week ending July 4 (vs. 217k expected). So that took the 4-week moving average down to 218.75k, and so far at least, claims remain well beneath their summer peaks in 2023, 2024 and 2025. However, existing home sales unexpectedly fell in June, falling back to an annualised rate of 4.09m (vs. 4.20m expected).

Looking at the day ahead now, and data releases include Italy’s industrial production for May, and Canada’s employment for June. Otherwise, central bank speakers include the ECB’s Vujcic and Stournaras.

Tyler Durden

Fri, 07/10/2026 - 08:07

via Shutterstock/National Interest

via Shutterstock/National Interest President Donald Trump attends an event to mark the launch of "Trump Accounts" in the Oval Office at the White House in Washington, D.C., July 6, 2026. Photo by Evan Vucci/ Reuters

President Donald Trump attends an event to mark the launch of "Trump Accounts" in the Oval Office at the White House in Washington, D.C., July 6, 2026. Photo by Evan Vucci/ Reuters

Polymarket takes another step in its return to the U.S. (Kanchanara/Unsplash)

Polymarket takes another step in its return to the U.S. (Kanchanara/Unsplash)

AFP/Getty Images: French President Emmanuel Macron shakes hands with Syrian President Ahmed al-Sharaa during a visit to the Umayyad Mosque in Damascus on July 6.

AFP/Getty Images: French President Emmanuel Macron shakes hands with Syrian President Ahmed al-Sharaa during a visit to the Umayyad Mosque in Damascus on July 6.  Shutterstock

Shutterstock

Getty Images

Getty Images Illustration via

Illustration via

Recent comments