Trump Grift vs. the “Biden Crime Family”

The post Trump Grift vs. the “Biden Crime Family” appeared first on CEPR.

Speak Your Mind 2 Cents at a Time

The post Trump Grift vs. the “Biden Crime Family” appeared first on CEPR.

Guest post by Josh Frankel

In April 2025, my NYS municipality rushed to sign a contract for Automated License Plate Readers (ALPRs), live view cameras, and drone-as-first-responder technology with Flock Safety. The Flock contract was hastily put on the agenda for a vote that same evening, bypassing the customary public notice, as required by law. The subject was misleadingly referred to as “Public Safety Equipment” and gave no further detail as to what was under consideration or why.

Curious about where the cameras would be placed, I filed a Freedom of Information Law (FOIL) request for the exact locations of the new Flock cameras. My request was denied three times, despite an extremely favorable opinion from the NYS Committee on Open Government (COOG).

So I sued. I filed an Article 78 litigation against the Village of Scarsdale (Index # 57090/2026 – February, 2026, Westchester County Supreme Court¹); last submissions to the judge were April 27. There is similar litigation, brought by the same New York Civil Liberties Union (NYCLU) attorneys representing me, pending against Westchester County.2

~~~

A veil of secrecy is an essential component of Flock’s playbook, and what happened in my village is the playbook in municipalities nationwide. Flock makes inroads, secures support — and, I believe, personally coaches local law enforcement and trustees on how to keep it all on the down-low. Before you know it, Flock cameras are popping up everywhere.

Worse, some communities vote them through “consent agendas” — bulk votes on what are supposed to be routine matters. One community, Lucas County Ohio, rammed through on a consent agenda and tried to cancel once local officials realized exactly what they’d done.

The story of what happened in my community was perfectly chronicled by independent journalist Jessica Burbank. She wrote a killer piece for DropSite News and produced an outstanding one-hour documentary. Jessica’s work was a catalyst in bringing mass surveillance front and center nationwide. Her work, along with that of 404Media and the Electronic Frontier Foundation, has been indispensable in the effort to rein in this out-of-control technology.

Ultimately, intense public outcry and the failure to secure grant funding led to the cancellation of the contract in my community.

My involvement in opposing mass surveillance continues through my ongoing litigation with the NYCLU and volunteer work with the Institute for Justice (IJ). I am slated to join an IJ webinar in the coming days to discuss my experience. To that end, I have put together the following “toolkit,” which I hope other like-minded folks will use as a roadmap in their local communities.

Each and every tool in the kit was useful in its own way, and taken together, they are very powerful.

Good luck!

NOTE: FOIA/FOIL laws vary greatly from state to state. What works in NYS might not work elsewhere (and vice versa). Familiarize yourself with your state’s law so you can extract everything to which you are legally entitled.

~~~

LOCAL ALPR ADVOCACY: A CITIZEN’S TOOLKIT

Be Vigilant. Be Engaged. Ask Questions.

Local surveillance programs can move from proposal to approval quickly—and sometimes with relatively little public attention. Residents do not need to be lawyers, technologists, or privacy experts to have an impact. They do need to pay attention, ask questions, obtain the records, and persist.

1. KNOW WHAT YOUR GOVERNMENT IS DOING-Watch local government agendas. Search Board, Council, Police Commission and committee agendas for terms such as ALPR, license plate reader, camera, public safety technology, surveillance, and vendor names such as Flock Safety.

-Attend or watch public meetings. Important details often emerge during discussion that never appear in the agenda or resolution.

-Read the actual documents. Don’t rely solely on how a proposal is characterized publicly. Obtain the proposed contract, staff memoranda, policies, presentations and supporting materials.

-Ask questions early. Who will have access? How long will data be retained? Who can search it? Can other agencies access it? Is data shared across jurisdictions? What audit controls exist? Where will cameras be located? What happens when the contract ends?

2. USE PUBLIC-RECORDS LAWS-NYS FOIL is a powerful investigative tool (with a strong presumption of access). Request contracts, proposals, vendor correspondence, policies, data-retention rules, audit logs, camera locations, internal memoranda and communications with neighboring agencies. AI can be very helpful in crafting comprehensive requests that are impossible to dodge.

-Ask for records—not answers. A well-crafted request identifies existing records rather than asking the government to explain itself.

-Request native electronic records when useful. Spreadsheets and databases can reveal considerably more than PDFs.

-Appeal denials. An agency’s initial “no” is not necessarily the final word.

-Know the exemptions being asserted. Ask the government to identify specifically why records are being withheld rather than accepting generalized claims about “security” or “law enforcement.”

-Use New York’s Committee on Open Government. COOG advisory opinions and guidance can be valuable when challenging an agency’s interpretation of FOIL. The Advisory Opinion I got — F19882 — could be very useful in other NYS municipalities.

3. FOLLOW THE PAPER TRAIL-Build a chronology.

-Save agendas, meeting videos, resolutions and contracts.

-Preserve emails and correspondence.

-Compare what officials say publicly with what the underlying documents show.

-Follow the money: grants, purchase orders, contracts, renewals and amendments can reveal where a program is headed.

-Set up a Google Alert for “Flock Safety” — stay current on what is going on nationwide.

–Look beyond your municipality. Counties, neighboring police departments and other agencies may possess records involving the same system or vendor.

4. USE THE PUBLIC PROCESS-Speak during public comment.

-Write to elected officials both collectively and individually.

-Ask specific questions that require specific answers.

-Draft and circulate a petition (one targeted petition is better than several that are fragmented).

-Encourage officials to adopt written policies before deployment rather than after cameras are operating.

-Ask for meaningful legislative oversight—not simply administrative approval by a police department.

–Bring other interested residents into the discussion. One inquiry is easy to dismiss; sustained public interest is much harder to ignore.

5. LEVERAGE LOCAL MEDIA-Local reporters are often looking for well-documented stories about government, policing, technology and privacy.

-Give journalists documents and facts, not merely conclusions.

-Explain why the issue affects ordinary residents—not just people concerned about surveillance.

-Simplify: A complicated technology story becomes much more understandable when framed around these simple questions: Who is watching? What are they collecting? Who can see it? How long do they keep it?

6. DON’T ACCEPT FALSE CHOICESSupporting effective law enforcement and questioning government surveillance are not mutually exclusive.

False question:

“Are ALPRs good or bad?”

Better questions:

What problem are we trying to solve?

Does this technology materially solve it?

What information will be collected about innocent people in the process?

What safeguards, oversight and transparency should accompany it?

7. DO RESEARCHAccess the FBI’s National Incident-Based Reporting System (NIBRS) to get actual crime and clearance data for your municipality. Doing so can go a long way toward determining if you even have a problem that needs to be solved. I believe “Motor Vehicle Theft” should be the most relevant crime to explore. What is, or has been, the trajectory of clearance rates, i.e. are they rising dramatically, as they should be? This data is readily available and should match up to what you would receive from a FOIL request, without the wait.

8. BE PERSISTENTGovernment processes move slowly. Records requests get delayed. Answers may generate more questions. Policies change. Vendors return with revised proposals.

Persistence matters.

9. THE MOST IMPORTANT LESSONLocal government works differently when people are watching.

You don’t need special access. You need curiosity, public records, patience—and a willingness to keep asking reasonable questions until you get reasonable answers.

FOOTNOTES

1. JOSHUA FRANKEL v. VILLAGE OF SCARSDALE

Special Proceedings – CPLR Article 78

2. I am not a named party in the new case against the County, though that COOG opinion and my FOIL work were foundational. (Index # 57090/2026 – Westchester County Supreme Court)

The post Flock Around and Find Out: A Citizen’s Guide to Local ALPR Oversight appeared first on The Big Picture.

My Two-for-Tuesday morning reads:

• The Housing Recession is Over: The vibes remain bad, the recovery is uneven, but recession is now behind us. Conor Sen thought 2026 was the year housing cracked — Florida, Texas and Arizona were carrying 20% to 30% more listings than the same point pre-pandemic, and the number was still climbing. He is calling it the other way now. (Conor Sen)

• Private Credit Is Under Growing Strain, Despite Industry’s Upbeat Tone: Default rates are hitting recent highs, and internal reviews of loan health point to tougher times ahead, a WSJ analysis shows. Default rates are hitting recent highs, and internal reviews of loan health point to tougher times ahead. (Wall Street Journal) see also Private Equity Is Stuck With 33,575 Unsold Businesses: Even amid a booming deal-making environment, private equity firms are unable to exit a growing number of investments at values their investors require. The exit math is not working. A number that size is not a backlog, it is a structural problem for the entire asset class. (New York Times)

• Making it to New All-Time Highs: The world is awash in negativity, and every week brings a fresh reason to get scared out of stocks. The record highs keep arriving anyway. To reach new highs again and again in the 2020s investors have had to ignore: A global pandemic. The fastest 30%+ drawdown in history. A supply chain crisis. Meme stock mania. A 40-year high inflation rate of 9%. Russia invading Ukraine. 73 crash predictions from Robert Kiyosaki. 19 Michael Burry top calls… (A Wealth of Common Sense)

• The Everyday Guide to Supersizing Your Retirement Account: There are a number of tricks to grow a tax-advantaged 401(k) or IRA into a fortune. The mechanical tricks for turning a tax-advantaged 401(k) or IRA into something considerably larger than the contribution limits suggest. (Wall Street Journal)

• Record Profits, Terrible Service: Something’s Got to Give for US Consumers: An interactive on the widening gap between what American companies are earning and what customers are actually getting. Experts say consolidation and market power have left consumers paying more for less (The Guardian)

• America’s Capital of Homebuying Regret: Austin, spring 2022: Ryan McPherson and his wife bid $20,000 over ask to reach $615,000 on a four-bedroom, and wrote the sellers a heartfelt letter to close the deal. Prices have gone the other way since. Meet the Texas homeowners who are deep in the red thanks to Austin’s long, painful real estate hangover (Business Insider)

• Kill the Ticks: America needs a bigger plan to control its tick problem. “The ticks are winning,” a CDC scientist wrote in a recent paper. To put it even more bluntly, humans are losing and are on the retreat. (The Atlantic)

• It’s the Summer of Purse Guys: Ashley Fetters Maloy on the handbag as punctuation mark, and what happens when men — sidelined by a few centuries of pockets in menswear — start carrying one. For years, men have talked themselves out of one of fashion’s greatest inventions. This summer, cool guys are embracing bags, from the huge to the itty bitty. (Washington Post)

• July was the hottest month in the US since records began in 1895: The month featured long, intense heat domes that led to record hot temperatures from the East Coast to the Plains and Southwestern states. NOAA’s temperature records date back to 1895. Andrew Freedman on long, intense heat domes that set records from the East Coast through the Plains and Southwest. Large wildfires were burning across the Pacific Northwest and Canada by month’s end, mirroring Europe’s hottest summer on record. (CNN)

• Loss is a Bitch: No matter how much I try, I’m sad more than I realize: A burned-out writer takes a few days off the keyboard, and his wife suggests he write something personal instead. What comes back are memories he had stopped questioning. (The Omission)

Video of the day: India’s Youth Are Angry. Here’s Why

Be sure to check out our Masters in Business with Jack Raines, a writer and venture capitalist. We discuss his new book, Young Money.

War Is Helping Chinese EVs Upend the Global Car Market

Source: Wall Street Journal

Sign up for our reads-only mailing list here.

The post 10 Tuesday AM Reads appeared first on The Big Picture.

A retired Syrian general who commanded forces fighting ISIS was abducted by personnel from the Syrian embassy in Lebanon, Al-Akhbar reported on Saturday.

Adel Issa, an Alawite brigadier general from Tartous, entered the Syrian embassy in Beirut at 12:30 pm on Friday to arrange a power of attorney for a relative. His Syrian driver waited outside for him, but he never returned. As his driver waited outside, a car with several young men stopped and demanded that the driver hand over the retired general's phone, claiming they needed to register his passport.

Syrian Embassy in Beirut

Syrian Embassy in Beirut

The driver waited for Issa until 4:30 pm before going to the embassy entrance to inquire about him. A Lebanese guard prevented him from entering, telling him the embassy had closed an hour before.

After persisting, the driver was able to speak with an embassy employee who told him that Issa had left the embassy 20 minutes earlier. This surprised the driver, as Issa never came out of the embassy to have the driver take him home.

The driver then informed the general's family of the incident. They began making calls to locate him, but his phone was switched off after 3:30 pm.

The family contacted several Lebanese organizations for help in determining his fate, fearing he might have been illegally detained at the embassy, given his status as an Alawite officer in the deposed government of Bashar al-Assad. There were also fears that he might be transferred to Syria and subjected to torture.

Since the fall of Assad's government in October 2024, Syria's new authorities, led by the former Al-Qaeda leader Ahmad al-Sharaa, have detained thousands of Alawite officers from the former army.

Syrian authorities claim they are detained for committing war crimes during the 14-year war that began in 2011. However, in practice they are typically detained based on their religious identity as Alawites.

According to a December 2025 report by Reuters, Syria's prisons are overflowing with Alawite men who are held without trial and often tortured.

Al-Akhbar notes that Brigadier General Issa had retired more than six years ago. He continued to live in Tartous and move around Syria without being pursued by the new authorities.

He gave a statement before a Syrian court a few months ago regarding a financial dispute with someone without being arrested or prosecuted, as there was no warrant or legal case against him. However, roughly one month ago, a group of unknown armed men raided Issa's home and inquired about him.

#Syria/#Lebanon: Following the scandal reported by the Lebanese newspaper Al-Akhbar over the Syrian Embassy’s abduction and detention of Syrian citizens, the embassy admitted yesterday that retired officer Adel Issa had been held inside the embassy. Embassy staff then handed him… https://t.co/WEkW2aF9TW pic.twitter.com/IgDK7k0H9N

— Syria Justice Archive (@SyJusticeArc) August 9, 2026

Issa was unable to determine whether the armed men were from the official Syrian security forces or from an armed faction affiliated with the new government but operating outside the chain of command. As a result, Issa decided to leave Syrian territory for Lebanon.

The Syrian Justice Archive (SJA) noted that after news emerged of the detention of the retired general, an attempt was made to cover up his abduction at the embassy and make it appear as if it was part of a legal process.

Saudi newspaper Al-Sharq al-Awsat claimed that Lebanese authorities had arrested Issa and requested his judicial file from their Syrian counterparts to decide whether to hand him over to Syrian authorities. SJA notes that the evidence indicates that Issa was taken by Syrian embassy personnel, not by Lebanese prosecutors or police.

"If Syria wanted his arrest and extradition, the proper procedure would have been for the Syrian Prosecutor General to formally request his arrest and handover through the Lebanese authorities, not for him to be abducted while visiting the embassy after legally leaving Syria," SJA stated.

The Syrian embassy admitted later on Saturday that Issa had been held inside the embassy and that embassy staff then handed him over to Lebanese security authorities after he had spent more than a day detained inside the embassy.

The Britain-based Syrian Observatory for Human Rights (SOHR) reported that Issa commanded the Syrian army's 17th Division. In 2015, he was given command of all Syrian ground forces in the eastern governorate of Deir Ezzor, which borders Iraq, before he retired in late 2016.

Under Issa's command, the 17th Division was responsible for protecting Deir Ezzor from ISIS, of which self-appointed Syrian President Ahmad al-Sharaa's armed group, the Nusra Front, is an offshoot. The Nusra Front was later rebranded as Hayat Tahrir al-Sham (HTS).

Another scandal emerged last week when journalist Lindsey Snell reported that the Nusra Front member, Mohamad Qanatari, who had kidnapped her in northern Syria in 2016, had been named as charge d'affaires to the Syrian Embassy in Washington.

My interview with the Syrian chargé d'affaires to the US back when he was a member of Jabhat al-Nusra. pic.twitter.com/g0NSaH1WUp

— Lindsey Snell (@LindseySnell) July 28, 2026

In 2012, Nusra was designated as a terrorist group by both the UN and the US State Department, despite covert US support for the group. Since HTS and Sharaa came to power, the US government has openly embraced members of the former terror group, including Sharaa himself, who visited the White House to meet US President Donald Trump in November 2025.

SJA reports that another disturbing incident involving the Syrian embassy in Beirut occurred earlier this week when a Syrian social media influencer, Hussein Abdul Qader al-Ahmad, was abducted after making a video for social media in front of the embassy.

In the video, Ahmad criticized the new extremist-dominated Syrian authorities, including President Sharaa – who formerly went by the nom de guerre Abu Mohammad al-Julani and is well known for dispatching suicide bombers and car bombs to kill thousands of civilians in Iraq and Syria.

After his abduction at the Lebanese-Syrian border, Ahmad appeared on Syrian government media in detention with visible marks on his forehead, suggesting that he was subjected to abuse or torture. He is now detained on charges of “insulting state symbols” and “provoking the feelings of Syrians.”

Tyler Durden Tue, 08/11/2026 - 03:30In "that's enough internet for today" news...

North Korea has apparently found the answer to record-breaking summer heat: dog-meat soup, chicken broth and stories about how hard Kim Jong Un sweats, according to Reuters.

Pyongyang hit 98 degrees, on Thursday, which state media said was the highest temperature recorded in the capital. With tropical nights piling up, the regime has rolled out an unusually enthusiastic summer survival guide.

Some advice is straightforward: watermelon, cucumbers, mung beans and plenty of fluids. Then things get considerably more North Korean.

A doctor quoted by the ruling party’s Rodong Sinmun recommended “nutritious foods” including fish porridge, red-bean porridge and dog-meat soup, traditionally believed to help people endure summer heat.

The newspaper even published a separate feature celebrating dog-meat soup, reviving an old saying that soup spilled on your foot during the summer dog days “becomes medicine.” North Korea also held a national dog-meat cooking competition earlier this year, because apparently it's important there that someone determines who is the best at cooking dog.

For less adventurous diners, state media promoted samgyetang, a chicken soup stuffed with ginseng, rice and jujubes. Television broadcasts also offered advice on hydration, swimming and outdoor exercise.

According to Reuters no North Korean weather emergency would be complete without reminding everyone that Kim Jong Un is also very hot, possibly hotter than you.

State media recycled stories of Kim heroically sweating through previous summers, including a 2013 construction-site inspection where his clothes supposedly became soaked. Other reports recalled him trudging through mountains and rain in 2018 and inspecting a seafood factory in temperatures reportedly reaching 39°C.

What Kim is actually doing during this heat wave was conspicuously absent. North Korea has disclosed no heat-related death figures, while neighboring South Korea has reported more than 20.

So the official North Korean summer survival plan appears simple: drink water, eat some soup and, if things get unbearable, remember that the Supreme Leader once perspired at a construction site.

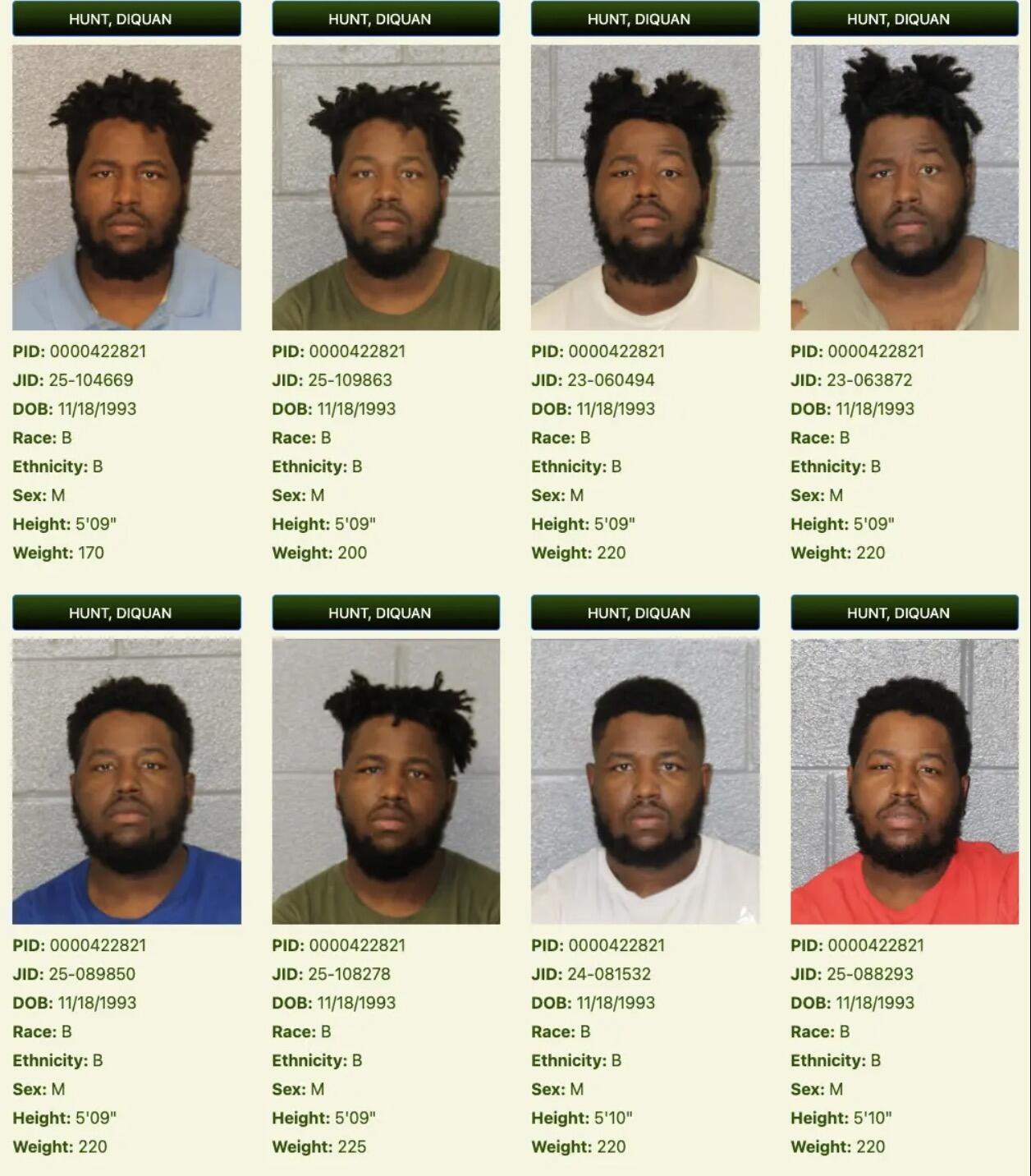

Tyler Durden Mon, 08/10/2026 - 22:10Relatives of a Charlotte man accused of attacking women in public say his behavior had become increasingly unpredictable and violent, prompting them to contact authorities before his arrest, according to the New York Post.

32 year old Di-Quan Schafar Hunt was taken into custody Thursday after disturbing videos circulated on social media showing confrontations with women on Charlotte streets.

According to Hunt’s sister, the problems extended beyond the incidents captured on video. She said relatives had witnessed violent behavior within the family and had previously called police because they were concerned about him.

The Post writes that the family believes Hunt has been diagnosed with PTSD and bipolar disorder and says he has not been taking medication. His sister said they had repeatedly tried to find help for him and are now concerned about the possibility of his returning to the community without treatment.

Hunt also has an extensive arrest record, with at least nine previous arrests reported.

Videos connected to the latest case appear to show Hunt confronting women without warning. In one clip, a woman is knocked to the ground as Hunt shouts at her. Another shows a woman being shoved before Hunt pursues her around a vehicle.

His sister said she turned over video evidence to police and later helped officers locate him.

While expressing concern about her brother’s condition, she also said the women involved deserve justice and acknowledged that the situation has created fear for Hunt’s own family.

Tyler Durden Mon, 08/10/2026 - 19:40Authored by Richard C. Crandall via American Thinker,

My first encounter with trans was in the early 1950s, when Christine Jorgensen became the first widely known person to undergo "sex reassignment" surgery. I remember some of my peers mocking Christine by threatening to swap the feminine lips and masculine mustache between Mr. and Mrs. Potato Head. After some laughter, eye-rolling, and snide smiles, seven-year-olds settled the issue: It was ridiculous - we called it crazy - to believe that Mr. Potato Head could become Mrs. Potato Head any more than a man could become a woman.

The trans issue reemerged with the Reimer twins, Bruce and Brian. In the 1960s, during what was supposed to be a routine circumcision, Bruce's penis was destroyed. Dr. John Money at Johns Hopkins University saw an opportunity to demonstrate that sex roles are a blank slate at birth and are shaped by culture, not genetics. He convinced Bruce's parents that with surgery, hormones, and therapy, Bruce could be successfully transitioned to female. Bruce was castrated, given hormones, renamed Brenda, and not told that he had once been Bruce. From the beginning, "Brenda" didn't like acting like a girl. He tore off his dresses and played with his twin brother's toys more than his own. After applying makeup, Brenda said he looked like a clown. By his early teens, Brenda was confused, depressed, lonely, and suicidal. When Brenda was finally told that he was Bruce, he realized that he was normal and that those trying to turn him into a female were the problem. Brenda became David, underwent penile reconstruction, a double mastectomy, and hormone treatment and married a woman.

For years after "Brenda" became David, Dr. Money claimed that Bruce's transition to Brenda was successful. After the truth came out, I again thought the trans issue was resolved. However, in what can only be described as a new level of hell, swapping parts between Mr. and Mrs. Potato Head has been replaced by dolls that allow children to swap internal and external sexual parts.

I hold the same view I did at age seven. I will reconsider my stance when trans advocates agree to the following conditions.

First, we can change our race. Whites who claim to be black or Native American are called race hoaxers, even though some have demonstrated substantial knowledge of and connection to their new race. A recent example involves a white woman who received injections to darken her skin and surgeries to enlarge her lips. She plans to undergo butt augmentation and surgery to widen her nose. She feels that she is black, even though she is told she will never be black. But if all it takes for a man to be a woman are feelings and mutilating surgery, shouldn't this woman's feelings and surgeries make her black?

Second, we can change our age. If the sex listed on a birth certificate can be altered based on feelings, why not the date of birth? Many people feel younger or older than their chronological age, and some even undergo surgery to look and feel younger. If feelings, rather than biology, determine one's sex, shouldn't they also determine age?

Third, we can be both sexes. Recently, a judge ruled that a man who doesn't identify exclusively as male or female can have a surgically created vagina in the space between his scrotum and anus. And just in time, we have sologamy, "the practice of marrying oneself." Would this be a heterosexual marriage?

Fourth, we can change our species. Individuals who feel they are reptiles tattoo their hands and faces to resemble snake or lizard scales. Those who want to become snakes undergo surgery to remove their ears and noses and have their teeth filed to resemble fangs. Those who identify as lizards have their fingers and thumbs amputated, leaving claw-like hands. They have also had their tongues surgically altered to look forked. If removing a penis and testicles transforms a man into a woman, then does removing ears and fingers transform a human into a reptile?

Fifth, we can become space aliens. To achieve this transformation, one man tattooed his body black and removed his upper lip, nose, and ears. Another man, in addition to full-body tattoos, cut off some fingers, his ears, and part of his nose. A third man has full-body tattoos and fangs. He also chopped off a finger on one hand and had the other hand surgically altered so that his fingers remain in a permanent "V" formation. Again, if feelings and mutilation can change a man into a woman, then don't feelings and bodily mutilation transform someone into a space alien?

Sixth, we can choose our nationality. If men who feel they are women are allowed to use women's bathrooms and locker rooms, then shouldn't people who feel they are of a certain nationality be allowed to live in the country they feel they belong to?

Seventh, it would be easier to adjust feelings to match the existing body than to mutilate the body to match feelings. Why do trans proponents accept only chemical and surgical mutilation to align the body with feelings when it is more rational and humane to use therapy to adjust feelings to align with one's sex?

Eighth, feeling the desire to amputate a healthy arm or leg is abnormal. Body Integrity Dysphoria (BID) is a condition in which the body does not match how someone feels it should look. This goes beyond simply feeling that one's nose is too big or one's breasts are too small. Individuals with BID feel they have too many arms or legs, leading them to want the problematic limb amputated. Others with BID may wish to be paralyzed or to lose their hearing or sight. If chopping off a healthy arm is abnormal, then isn't removing healthy sexual organs also abnormal?

Ninth, we can belong to the ethnic group of our choice. Shouldn't feelings be enough to belong to an ethnic group?

Tenth, we don't need to accept and accommodate individuals' feelings about their identities. If a man who feels he is a woman also feels he is a queen, do we need to accommodate his feelings by addressing him as "Your Majesty" and bowing to him?

Eleventh, the feelings of trans people do not supersede those of people who believe trans people are mentally ill. Trans people demand that others tolerate their feelings, yet they don't tolerate others' feelings. We have seen men who look like men but feel they are women become unhinged when addressed as "sir" rather than "ma'am." There is the same lack of tolerance for those who feel that men pretending to be women should not be allowed to participate in women's sports. They are even incapable of tolerating a T-shirt featuring the logo "XY ≠ XX." If trans people don't respect others' feelings, then can't others disrespect the feelings of trans people?

Feelings do not change reality, and the reality is that there are no Joseph Mengele, Dr. Moreau, Dr. Fauci, or Dr. Frankenstein medical procedures that can turn us into space aliens, reptiles, or the opposite sex.

Image via Pexels.

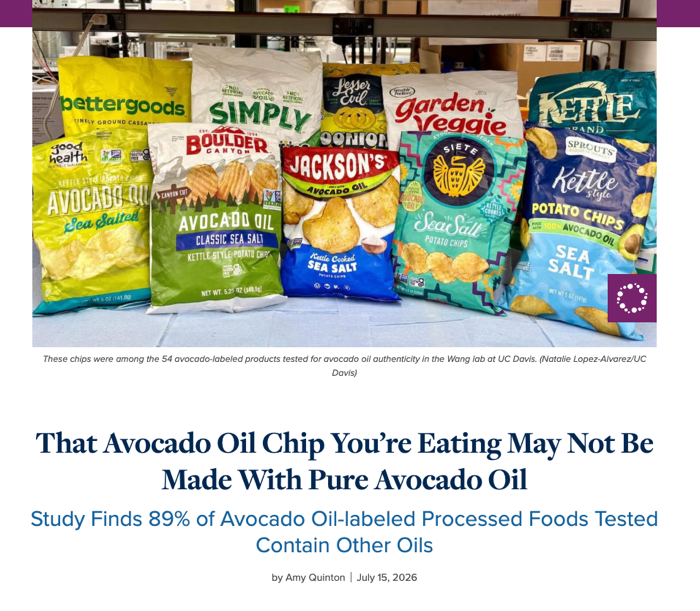

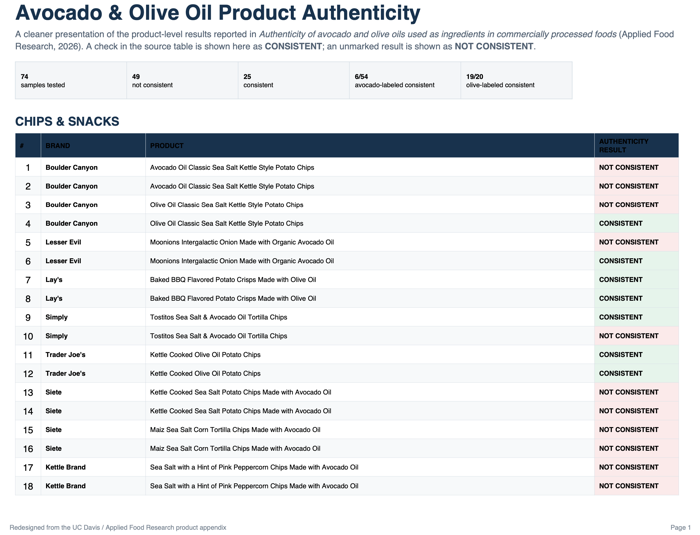

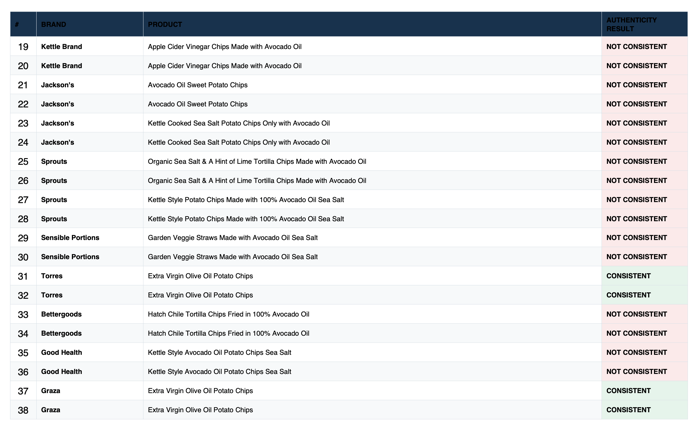

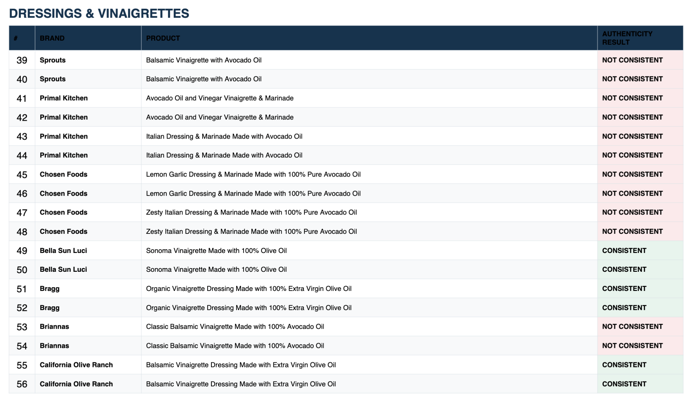

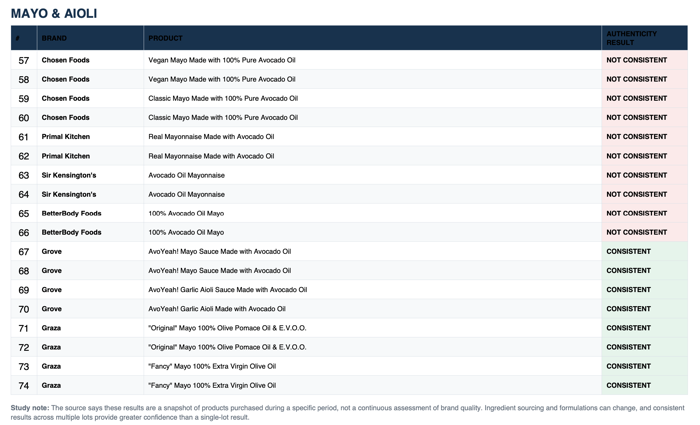

Tyler Durden Mon, 08/10/2026 - 19:15A new University of California, Davis, study found that a shocking number of avocado oil-labeled chips at the supermarket, marketed as a healthier alternative to toxic seed-oil chips, might not be made with pure avocado oil and, in fact, contain other oils.

UC Davis researchers tested 54 avocado oil-labeled products purchased from California supermarkets and online retailers in 2025 and 2026 and found that 48, or 89%, contained cheaper oils despite being labeled as containing premium avocado oil. The failure rate included 93% of chips, and beyond the snack aisle, 71% of mayonnaise products and 100% of salad dressings tested also failed.

"Consumers are increasingly paying a premium for products made with avocado oil or olive oil," lead author Selina Wang, Professor of Cooperative Extension in the UC Davis Department of Food Science and Technology, stated in a press release. "They deserve to get what they pay for and food manufacturers deserve confidence that the ingredients they purchase from suppliers are authentic."

The Trump administration helped propel the MAHA movement into the mainstream, prompting millions of consumers to reevaluate what's actually in their food, including the widespread use of seed oils amid study after study showing potential health effects:

Results by brand:

There is only one real solution here: take control of what you eat. We've long believed that winning the information war starts with properly fueling the brain, which means getting back to real food and cutting out as much ultra-processed junk as you can.

And if you're still going to snack on a bag of chips, why not just keep it super simple? Potatoes cooked the old-fashioned way in actual grass-fed beef tallow. No mystery oils. No ingredient-label guessing games. Just a better chip.

Tyler Durden Mon, 08/10/2026 - 18:50Authored by Frank Fang and Jan Jekielek via The Epoch Times,

The FBI worked with the Department of Homeland Security (DHS) and the Office of the Director of National Intelligence (ODNI) on the recent disclosure by President Donald Trump on foreign influence on U.S. elections, agency director Kash Patel said.

FBI Director Kash Patel speaks during an interview at the FBI headquarters in Washington on Aug. 4, 2026. Madalina Kilroy/The Epoch Times

FBI Director Kash Patel speaks during an interview at the FBI headquarters in Washington on Aug. 4, 2026. Madalina Kilroy/The Epoch Times

During an interview with EpochTV's "American Thought Leaders," aired on Aug. 8, Patel said the three agencies worked as partners, but the FBI played a smaller role, while DHS and ODNI had the technical capabilities and a remit focused more on overseas incidents involving U.S. election infrastructure.

"We shared our information. We made a lot of our information public through President Trump's speech the other week," Patel said.

Patel said the three agencies acted at Trump's direction.

"I think the president was right to go to the nation and the world and put forth this information, but it was only possible because the president directed us to declassify and divulge this information to the American public and the world," Patel said.

In a primetime address on July 16, Trump announced the declassification of documents that showed China had illicitly acquired 220 million U.S. voter files, including names, addresses, phone numbers, and other information.

"This data loss presents an unprecedented election security nightmare," Trump said during the address.

Trump did not explicitly claim that China altered the outcome of the 2020 presidential election.

China began targeting him in an operation in 2018, Trump said, citing a CIA report that described an effort to "reduce [his] votes and make him resign or prevent his reelection."

The CIA report found "China was working to influence the results of the U.S. midterm elections, and later the results of the 2020 presidential election itself," according to Trump.

In 2019, China had a strategy focusing on "undermining domestic confidence in the U.S. president," Trump added.

"They wanted to just make [it] sound like your president wasn't so hot when actually your president has done a great job," he said.

That strategy included influencing U.S. business leaders to turn against him, Trump said.

"The Chinese government sought to identify U.S. journalists who had reported negatively on the U.S. president and pay them large sums of money to write more negative articles about him, as many as they could," he said.

The declassified documents included a CIA wire memo from July 2000, which included information from the FBI, showing that the Chinese Communist Party was targeting "personal e-mail accounts of senior US leadership, including officials in the Executive Office of the President and high-ranking officials in multiple Executive Branch organizations, Congress, and the federal judiciary."

Separately, a National Intelligence Council report found that "Beijing has expanded its cyber collection of data related to the 2020 US elections by carrying out opportunistic intrusions against US private-sector entities in efforts to collect information on US political candidates, campaigns, donors, and voter data."

Trump's claim on China's election interference by targeting American voter registration data was backed by the heads of the ODNI, the National Security Agency, the CIA, and the Department of Homeland Security, according to a White House fact sheet released on July 30.

In September 2025, Patel discussed China's threats extensively during a hearing before the House Committee on the Judiciary.

China "presents the greatest and most sophisticated cyber threat to U.S. public safety and national security," Patel said, according to written testimony.

He singled out one particular Chinese threat group, "Salt Typhoon," which had breached the networks of multiple telecommunications companies in the United States and elsewhere.

Patel also noted in his written testimony that all 55 of his agency's field offices had active Chinese counterintelligence investigations.

"This calendar year alone, as I was mentioning, our counterintelligence operations and cases brought against the Chinese are up by something like 40 percent," Patel told House lawmakers at the hearing.

"The PRC [People's Republic of China] has deliberately created an environment that abuses global interconnectedness and encourages intellectual property theft, using human intelligence officers, corrupt corporate insiders, and reckless and indiscriminate cyber intrusions," Patel stated in his written testimony.

Watch the full 'American Thought Leaders' interview below, covering a great deal more than election integrity:

00:00 Intro

1:31 World Cup Security

4:17 Scam Centers & Operation Blackout

6:55 Pig Butchering Scams

11:25 Slaves in Scam Compounds

13:19 Why's the FBI Working with China's MPS?

19:00 How Does the FBI Get the Money Back?

23:41 Advice to Viewers on Scams

26:00 Chinese Interference in 2020 Election

28:26 Removal of Spies

31:42 CCP Targeting Americans with Security Clearances

35:26 Tackling Transnational Repression

38:40 Terrorist Attacks Thwarted

41:26 What is the Director's Strategic Information Center (DSIC)?

44:33 Major Reforms at the FBI

President Trump is currently experiencing a rare moment of his plans for the Mideast region being rejected on multiple fronts - even among allies, apparently. Israeli Prime Minister Benjamin Netanyahu over weekend rejected a US-backed 15-point peace plan for Gaza, which marks a rare and very glaring public break with Trump.

Netanyahu was surprisingly up front in acknowledging the complete break in policy vision from the White House. "Contrary to all those who preach to us, we do what must be done for Israel’s security and we can and will stand our ground even against our best friends when necessary," he stated.

He said he was confronting a "wave of rumors about Israeli weakness and Israeli withdrawals on all fronts" and made clear that Israel won't succumb to ongoing US pressure to end wars in Gaza, Lebanon and Iran - unless Israel decides it is in its security interest.

Anadolu/Getty Images

Anadolu/Getty Images

Netanyahu was explicit on rejecting Trump's Board of Peace plan which was presented in July:

"Israel rejects the 15-point document," Netanyahu said at the start of a cabinet meeting on Sunday, speaking in Hebrew. "The IDF will not make any withdrawal until Hamas is truly disarmed and will continue to thwart threats against our forces and citizens."

A Hamas statement in the meantime stood by the plan. It said the group "affirms its commitment" to Trump's 15-point plan for the second phase of the ceasefire agreement with Israel, "and establishing a clear timetable for their implementation."

"We call upon the mediators, guarantors, and the Peace Council to assume their responsibilities, ensure the commitment of all parties to what has been agreed upon, and prevent any violations or breaches that could disrupt the implementation process or undermine the ceasefire agreement," the Hamas statement added.

Even CNN has picked up on the fact that Netanyahu - whose government receives literally billions of dollars in US funds and arms each year - has been unusually blunt in his rejection of Trump's big initiative:

On tricky issues, Israeli prime minister Benjamin Netanyahu’s preference is to kick the can down the road. If he must take a position, he likes to include a twist of ambiguity, some wiggle room, just in case things get hairy later. Not this time, though, on the subject of US President Donald Trump’s roadmap for progressing the Gaza ceasefire agreement.

While the Israeli leader risks facing the wrath of Trump, it has been about a full day since reports of the glaring Israeli rebuff have emerged, and yet there's been no immediate Truth Social diatribe or statement calling out Bibi.

And now the Middle East strategy "Ls" are piling up, the same outlet observes:

The US president – more desperate than ever for a win, as his Iran folly looks increasingly like handing him an L – reinvested in Gaza 10 days ago, declaring that his Board of Peace had reached a “historic agreement” with Hamas for its complete disarmament. The board’s top envoy, Nickolay Mladenov, went on to explain carefully on X that decommissioning would need to take place “in lockstep” with Israeli troop withdrawal, suggesting a phased process by which the Israel Defense Forces (IDF) would pull back in stages from positions inside Gaza, as Hamas turned in its arms.

It could be that Netanyahu too sees Trump up against the ropes when it comes to the Middle East, and views this as an opportunity to assert Israel's 'least-bad option'.

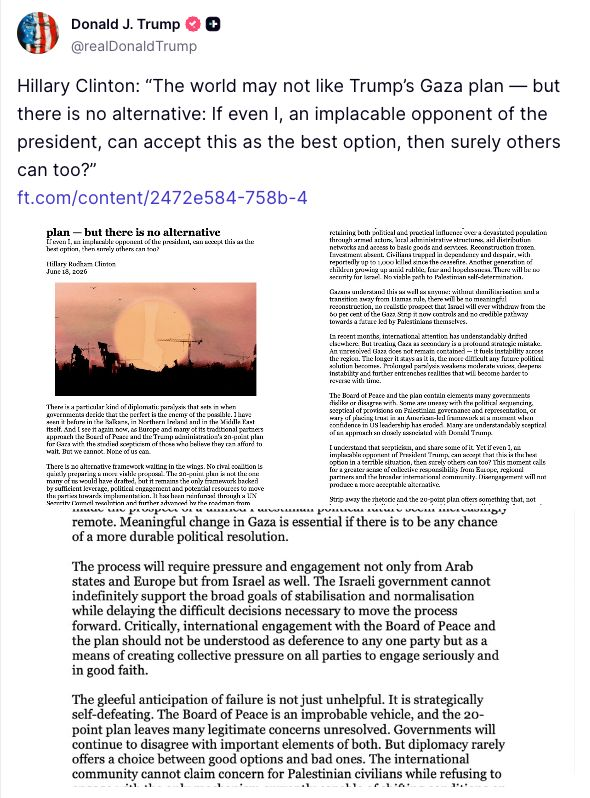

Again, Trump has remained quiet on the Netanyahu issue, but surprisingly presented 'validation' from an unlikely source - former Secretary of State Hillary Clinton, who said she supported his Gaza plan.

She argued in an op-ed that there is no alternative to Trump's Gaza plan, and that she's still able to acknowledge this despite being an "implacable opponent of the president".

Perhaps Trump might be telling himself that Netanyahu's public betrayal is just an "election thing" and so he must speak primarily to domestic voters, given the country's general election is just under 12 weeks away.

Tyler Durden Mon, 08/10/2026 - 16:40Authored by James Howard Kunstler,

"Kill them. Murder them. Let the streets soak in their red capitalist blood.”

- Hasan Piker

You can’t overstate the power of ideas, especially bad ideas, and super-especially bad ideas that are really just manifestations of emotional states such as envy, vengefulness, enmity, sloth, and greed. Did somebody say communism? A lot of people are saying it lately. This garbage barge of management nostrums for the ills of advanced industrial society has steamed back into New York Harbor and is busy now dispatching its agents across the land.

It’s yet another youth movement in an America which cultivates them at regular intervals associated with Fourth Turnings. I happened to be in college during the last one, the hippie rebellion of the late 1960s. It was mostly adolescent sexual energy tinged with resentment over the military draft and the war that went with it, plus a lot of marketing opportunities for music and clothing.

The US economy back then was still a roaring industrial engine. The comforts of that bygone time are legendary. You could easily support a family on an assembly-line job. College was cheap as hell — my State U charged about $500-a-year for tuition and room-and-board. (Imagine that!) You could hide-out from the draft there, too. The new birth-control pill turned campus life into a non-stop orgy with classes for R & R. Is it any wonder that the hippies morphed so easily into hedge funders?

This time around it’s pretty ugly for the youth demographic. College for them turned out to be a life-altering swindle, burdening the young with unpayable loans that can’t even be escaped via bankruptcy. Even the sex angle was ruined by vindictive feminism and the trans fad. Work is scarce and it’s nearly impossible to make a living at it, that is, pay for food and a roof over your head (and, ugh, those loan repayments!). Plus, work is mostly found only in meaningless service to despotic corporations. The most enterprising might land a job in an NGO, but the work there is “activism,” which is pretend work, productive of nothing but the acting-out of grievances.

These grievances, it has been noted by many high-toned observers like VDH, are real enough to provoke a desperate reach for remedies, and communism is a ready-made portfolio for all that. In the 1960s, we still had the reverberations of the civil rights crusade setting a basic moral tone for hippiedom. But fifty years later, that has all mutated into a race-and-gender hustle that adds so much piquancy to the recycled communist agenda. (Note that a hustle is a low-grade racket, and a racket is an effort to get something for nothing.)

So, today’s communist program is not just a war against the injustices of capital, but a jihad against the Western Civ horse that capital rode in on, and most particularly the white horseman up in the saddle.

Kotkin’s explanation of why socialism is attractive to the young and the intellectuals feels very accurate, especially what he says about the young in the first thirty seconds. https://t.co/JvuDLE2pwS

— Clifford Asness (@CliffordAsness) August 9, 2026

Hasan Piker, the present guru and demigod of the movement, put it pretty plainly in a Twitch-stream a few years back when he was rising to stardom on Uncle Cenk Uygur’s Young Turk Network.

“We want more immigrants to come into your countries and then they’re gonna fuck your sisters and then your daughters — we’re here to destroy the White race, bitch.”

Piker is also a leading amplifier of Jew-hatred and other calumnies such as the USA “deserved” the 9/11 attacks. Apropos of our action in Iran, Piker quipped, American soldiers should be shot at like cattle (link).

Piker is rumored to have earned over $6-million on Twitch. He’s quite tall (6’4”) ripped, and a snappy dresser, often sporting old-fashioned sport-jackets with a necktie (dress for success?) and is probably catnip to the cat ladies of Gen Z, who comprise the bulk of the activist corps of the rising Gen Z Democratic Socialists - as the communists have styled themselves to avoid stimulating any action around the Communist Control Act of 1954 (50 U.S.C. §§ 841–844), which categorizes the Communist Party per se as “an instrumentality of a conspiracy to overthrow the Government of the United States.”

The dapper Hasan Piker, dressed for success

Altogether, Hasan Piker and the Democratic Socialists pose quite a vexing problem for the pathetic, old, square, bloviating chuds in the Democratic Party of the Chuck Schumer / Cory Booker ilk. Other bloggers (e.g., Jeff Childers at Coffee & Covid) have observed that Democratic Socialism is the monster that the Dems have been working on sedulously for more than a decade in their Frankenstein lab of Gramscian cultural overthrow. The monster has escaped and is now out on the highways and in the hedges terrorizing the public.

You are surely aware that the entire regular agenda of the Democratic Party has for some time been patently insane. They are still wasting the nation’s patience with debates over the self-evident idiocy of men in women’s sports, resistance to the deportation of illegal immigrants, and their obviously evil opposition to voter ID. Communism is just the icing on that fruitcake. The recent primary election victories of such prodigies as Abdul El-Sayed, Melat Kiros, and Darializa Avila Chevalier, along with the ongoing capers of Mayor Zohran Mamdani pretending to govern New York City, must be giving the old guard the vapors.

And yet, the most pathetic actual commie among them, Sen. Bernie Sanders (I-VT), the Jewish, Israel-hating alte kocker, abides and even thrives in his new role as Godfather to this hatch of larval communist youth. This is Bernie’s revenge on the party that robbed him of two presidential nominations.

He’s doing what all good Jacobins do — what they live for! He has sentenced his old comrades of the DNC to death. He’s stuffing his old enemies into the tumbrel and carting them off to the public square for execution.

They can see it coming and it’s giving them the heebie-jeebies.

And finally, of course, the Mamdanis and El-Sayeds and their spawn will come for Bernie, too, leaving only AOC in the ensanguinated ruins to become America’s Eva Perón.

Wait for that!

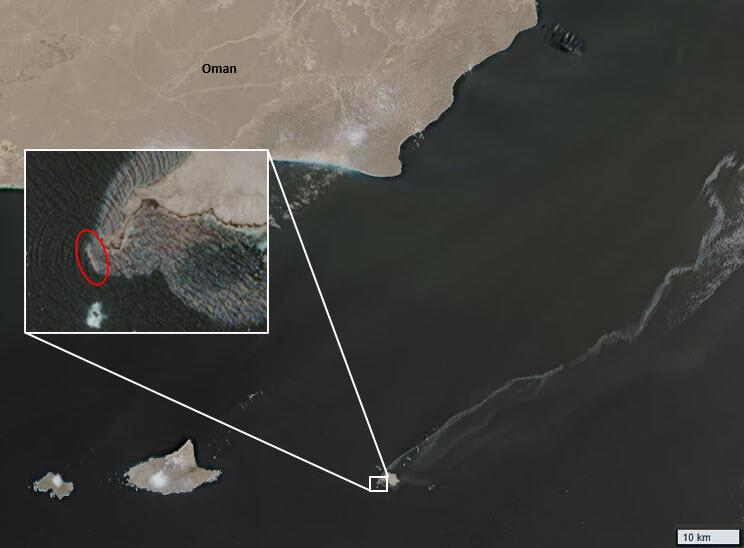

Tyler Durden Mon, 08/10/2026 - 16:20Leaking crude oil from a tanker grounded off a nature reserve in Oman has created a slick covering almost 400 square kilometres, a size six-and-a-half times the land area of Manhattan, the country's government said on Monday. The Caroline Bezengi is loaded with close to one million barrels of Russian oil bound for Asia and first reported difficulties on June 8 off Yemen, with two maritime security sources saying initial assessments indicated a blast had occurred onboard. No party has taken responsibility for attacking the vessel.

Oman, in its first public disclosure on the environmental impact, said on Monday it was seeking to tackle the oil leak near the Hallaniyat Islands.

Oman's Sultan Haitham bin Tarik issued a royal decree last year creating a nature reserve around the islands, an area that is home to wildlife including Arabian Sea humpback whales and Socotra cormorants.

The oil slick covers some 390 square km (150 square miles), Oman's Environment Authority said in a statement carried by the state news agency, adding that there was no concern for facilities in the area including water desalination plants and tourist facilities.

Environmental group Greenpeace last week estimated the slick at around 600 square kilometres citing analysis of satellite imagery.

It extends northeast of the islands and is within an estimated seven kilometres of the coast, the authority said.

A spill of this scale requires dispersant be sprayed across the affected area by aircraft and the use of booms and other equipment to collect the oil before it reaches the shore or sinks to the sea floor, said Tony Gutierrez, professor of environmental microbiology and biotechnology at Edinburgh's Heriot-Watt University.

"If this oil is kept offshore, the impact will be much less than if the oil reaches shallower waters and the actual coastline," he said, citing the impact on diverse marine life such as coral, birds and fish.

"You could find oil still there years later. And that's what happened with Exxon Valdez. Ten years down the line, there still were remnants of oil," he said, referring to a 1989 spill in Alaska.

An analysis by Reuters of satellite imagery and shipping specialists showed the spill from the stranded 274-metre (900-foot) tanker was still spreading at the end of last month, raising concern about possible environmental damage.

The Caroline Bezengi loaded at Russia's Black Sea port of Novorossiysk in April and passed through the Suez Canal at the end of May, ship-tracking data shows.

The grounded tanker had previously been sanctioned by the UK and the European Union over its role in transporting Russian oil. It was last seen sailing under a false Cameroon flag, according to the Equasis maritime database.

Built in 2001, it is part of the so-called shadow fleet of older oil tankers used by Russia which lack Western insurance cover and sail under the flags of various nations to obscure their true ownership. It was listed on public shipping databases as flying the Cameroon flag but was among 39 vessels de-listed from Cameroon’s ship registry in June. The ship is subject to sanctions imposed by the European Union, Ukraine, the UK, Canada and Switzerland.

It was unclear how the ship became stuck, but it was hauling about 1 million barrels of Russia’s Urals crude loaded in mid-May. Ukraine has repeatedly attacked ships carrying Russian oil. However, the vessel is further away from Russian waters than ships Ukraine has hit in the past.

Its registered owner is Rentoor Shipmanagement Ltd and its manager is Villar Shipmanagement Ltd, according to LSEG data. Reuters could not immediately reach those firms, which appear to be based in China.

Authorities are working to identify the sources of the leak, contain the environmental damage, secure the vessel and safely transfer its remaining oil cargo, the news report added. They’re also conducting aerial surveillance, subsea diving inspections and field surveys, using satellite imagery and environmental modeling to track the slick’s movement and forecast its drift.

Tyler Durden Mon, 08/10/2026 - 15:45By Phil Brink of FreightWaves,

Federal officers uncovered more than 1,000 pounds of cocaine concealed beneath floorboards on a commercial truck’s attached flatbed trailer. The truck arrived at California’s Calexico Port of Entry. Authorities estimated the recovered narcotics were worth more than $20 million. The shipment also included 269 bundles of rebar.

The driver, Jose Manuel Lopez Lopez, was the truck’s only occupant, according to federal prosecutors. Lopez, 44, entered the United States from Mexicali, Mexico. Officers arrested him after finding 366 packages within the trailer. The cocaine weighed 1,002.13 pounds, or 454.56 kilograms.

Inspectors find drugs beneath trailer floorCustoms and Border Protection officers X-rayed the attached flatbed during the border inspection. The scan showed anomalies in its wooden floorboards. A drug-sniffing dog then alerted officers to the equipment. Investigators unloaded the rebar before removing the planks.

Officers found packages stuffed beneath those boards, the U.S. Attorney’s Office reported. Homeland Security Investigations agents assisted the inquiry. Drug Enforcement Administration personnel also participated in the case. Prosecutors described the amount as “a tremendous amount of drugs, even by the standards of this district.”

The recovery marked the Southern District of California’s second-largest cocaine seizure during 2026. The larger May investigation began with a months-long task force inquiry into a supposed retail store near Otay Mesa. Agents later found a 1,933-foot cross-border tunnel stretching from Tijuana to the business. Authorities estimated the passage reached 55 feet deep and included reinforced walls, rails, ventilation and electricity.

Federal prosecutors charged four people after officers seized 1,029.60 kilograms of suspected cocaine, or 2,269.87 pounds. Authorities estimated that May recovery had a value of more than $45 million. Investigators found the tunnel’s exit beneath a storage-room floor at the Buy 4 Less store. A hydraulic lift concealed the access point, according to the U.S. Attorney’s Office.

Driver enters not-guilty pleaLopez pleaded not guilty during his federal arraignment July 28. U.S. Magistrate Judge Lupe Rodriguez Jr. scheduled his detention hearing for Aug. 3 at 10 a.m. Court records list the matter as case number 26-mj-08705. Assistant U.S. Attorneys Paul Benjamin and Lawrence Casper are prosecuting the case.

Prosecutors charged Lopez with importing cocaine into the United States. The charge falls under Title 21, U.S. Code, Sections 952 and 960. It carries a mandatory minimum prison term of 10 years. A conviction could bring a maximum sentence of life in prison.

The California Homeland Security Task Force investigated and prosecuted the matter through Operation Take Back America. Customs and Border Protection, Homeland Security Investigations, and the Drug Enforcement Administration handled the investigative work. The federal charge remains an accusation. Lopez is presumed innocent unless proven guilty in court.

Why it mattersCriminal organizations can use legitimate commercial equipment and ordinary cargo to conceal high-value contraband. Freight professionals should understand how a routine-looking shipment can carry risks beyond theft or fraud.

Tyler Durden Mon, 08/10/2026 - 15:25Authored by Christian Toto via American Greatness,

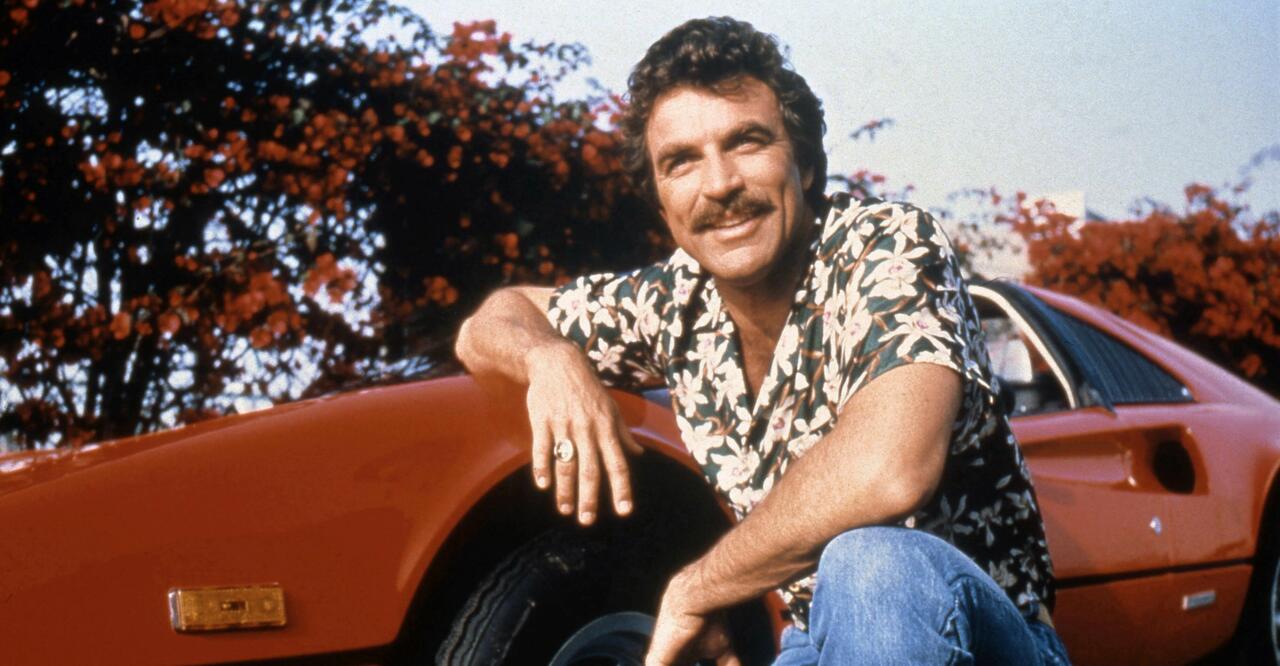

Tom Selleck destroyed the so-called Queen of Nice in 1999 without even trying.

The Magnum, P.I. alum sat down with Rosie O'Donnell a short time after the Columbine High School shooting that left 14 people dead. The host's "nice" shtick crumbled in real time as she savaged Selleck for his NRA support. He was simply there to promote his movie, but she bullied him anyway.

"Now you're questioning my humanity," the actor said following her line of attacks. O'Donnell's image never fully recovered, while Selleck has maintained his star status, in part, by never getting nasty or political.

The Blue Bloods star's nonpolitical persona is even more admirable today, and the 81-year-old is sticking to it. He appeared on CNN recently as part of the Ronald Reagan Presidential Library tour. Selleck is a fan of the late president, hardly a controversial take.

The CNN reporter pressed Selleck on the current state of the country and, more specifically, President Donald Trump. Selleck wisely refused the bait.

"Well, [Trump is] certainly a mixed bag. I stay out of the current political world. Why piss off half the country when you're in the business of entertaining people?" he said.

He's right. Except plenty of artists can't stop doing just that.

The worst example remains Snow White star Rachel Zegler. The 20-something actress insulted that film's source material and, later, told Trump supporters they should "never know peace."

Her film lost a reported $170 million for Disney.

Last month, actor Alan Ritchson of Reacher fame slammed both the Catholic Church and President Trump during an angry podcast interview. His new film, Motor City, bombed at the box office.

Far-Left actor Mark Ruffalo won't stop sharing his socialist views in interview after interview. He's the anti-Selleck, spouting off at any opportunity.

Yet he wisely avoided controversy while promoting his co-starring role in Spider-Man: Brand New Day. The team behind the film must have been high-fiving behind the scenes as the movie broke the all-time record for an opening weekend haul.

No cleanup on aisle 4 - aka doing damage control for Ruffalo's hot takes.

Stars are increasingly political in the modern era, but the results aren't always so clear-cut.

The culture wars surrounding Christopher Nolan's The Odyssey didn't hamper that film's gargantuan box office haul, nor did its co-stars' woke comments.

Many politically active stars remain in demand, as moviegoers refuse to boycott their work. Heck, Ruffalo has five IMDb credits in 2026 alone.

Still, for some, an actor's chronic political talk, often couched in extreme or cruel fashion, is a deterrent for consumers.

Selleck never has to worry about that. He's kept the focus on storytelling for decades, and he has a fine career to show for it. A newer crop of stars has embraced the Selleck standard, rejecting the Left's "politics at all costs" mantra.

We recently saw Kevin James, Michelle Yeoh, and Neil Patrick Harris refuse to engage in political opinions during press exchanges. Their silence was noteworthy for good reason. They're the exception to the new celebrity rule.

Will journalists be pressing Zegler or Ritchson about their newest projects when they're in their eighth decade, as they do with Selleck today?

Christian Toto is the editor of HollywoodInToto.com - "The Right Take on Entertainment." He's an award-winning journalist and movie critic whose film reviews are heard on radio stations across the country. He co-hosts Denver's Mike Rosen at the Movies radio show on KOA NewsRadio as well as the weekly "Hollyweird" segment on The Michael Brown Show.

Tyler Durden Mon, 08/10/2026 - 14:40Authored by Roger Kimball via American Greatness,

Jason Arday should ask for a cover charge. His entertainment value is that splendid. For the last couple of weeks, the "youngest ever black professor" at the University of Cambridge has been a nearly ubiquitous and nonstop source of hilarity. The proximate catalyst for the comedy is the imminent publication of Great and Unfortunate Things, co-written with the "book doctor" Eve Claxton. It is due out on August 11 from Simon & Schuster. Amazon lists it as an "Editor's Pick" of "Best Biographies & Memories." "A story of resilience, dignity, and the extraordinary power of those who hold steady for us when we cannot yet hold steady for ourselves," says one blurber. "Makes you believe in the transformative power of grit and the magic of a mother's love," quoth another. A story easily worth the "$1.4 million" advance that Jason said he was offered for the book (though that figure is disputed). Did you know that poor Jason, now 41, was "diagnosed with autism and developmental delays at age three, and experts told his parents he would never speak, write, or live independently"?

And that was the least of Jason's trials. The Atlantic got hold of an advance copy of the book and drew attention to what some have delicately described as numerous "inconsistencies" in Arday's account of his life story. Comparing the final book with the book proposal, the author of "Icarus in the Faculty Lounge" uncovers some amazing things. In his proposal, Arday recounts being hit by a car, spending months in a sort of conscious coma, then waking up and having to relearn "everything - how to walk, to talk." That remarkable experience is, we are told, entirely omitted from the book, as is his bout with testicular cancer (in the book he grapples with not one but two brain tumors). Arday has apparently never been to Brazil, but that quotidian fact did not prevent him from encountering a mysterious "shaman woman" there who predicted that he would suffer greatly but also achieve great things. "Every event she described has since come to pass," he wrote.

Time itself is plastic in Jason Arday's hands. He somehow managed to appear on the television program Seven Up more than 20 years before he was born. He is also a remarkable athlete, having run 30 marathons in 35 days. Take that, Pheidippides! Clearly, Great and Unfortunate Things should not be categorized as "memoir" or "biography" but fantasy. But the blatant fabrications in the book are only the tip of the Arday midden. There is a vigorous online debate now about whether Simon & Schuster will pull the book before publication. If I were a betting man, I would put a fiver on the cynical side, saying, "No, they'll go through with publishing Arday's drivel. They are that craven." We'll know whether I am right on Tuesday. But speaking of "drivel," take a moment to absorb this 40-minute dollop from the master himself. How proud Cambridge must have been!

Like Shakespeare's Autolycus in A Winter's Tale, Arday also seems to be a "snapper-up of unconsidered trifles," i.e., a plagiarist. Last month, the London Telegraph published a story listing more than 100 passages from Arday's doctoral dissertation that were "identical or nearly identical to a 2009 PhD thesis by Paula Zwozdiak-Myers, a Brunel University student." Does that list prove that Arday is guilty of plagiarism? Outside the universe of Jorge Luis Borges, I would say yes, it does. But when Cambridge was first shown the evidence of plagiarism, it dismissed it as part of a "vile campaign to undermine his credibility." Vile or not, the allegations were irrefutable. Arday has just resigned his professorship. One enterprising blogger reports that Arday's letter of resignation was put through an AI-writing detection program and was determined to be "fully AI-generated" with high confidence. Consistency! I like to see it. Arday hasn't admitted any wrongdoing, though. He is just moving on to his "next phase." Nolo contendere, as Spiro Agnew once put it.

Have I mentioned that Arday is black? He is, and you will not be surprised to discover that among his fabulations are charges that he has suffered from numerous racist attacks. "There has been," he said in an interview, "a very well-orchestrated and coordinated campaign to unseat me from my position. The motive is racially motivated. I think there's a reason why it's me, and I do think that reason is aligned to ableism and racism." When questions about Arday's thesis surfaced, Jack Grove, a reporter for the Times Higher Education, started looking into "anomalies" in Arday's CV and the charges of plagiarism. Arday promptly reported Grove to the Metropolitan Police, claiming harassment. The police opened a four-month inquiry to investigate the charges. They have subsequently apologized.

Almost everything about Jason Arday is fake. He was described as a "professor of sociology." But his degrees are in education, not sociology. He naturally continues to enjoy support from the academic left. "The glee of the right over the Arday case," runs one typical effusion, "is indicative of how unsafe academia is for Black scholars and of an attempt to erode whatever fragile safety still exists." But who said anything about black scholars? The leader of the Green Party, Zack Polanski, signed a letter claiming that the allegations against Arday were "entirely false." Blacks, you see, are often "held to higher standards" than whites. What a card Polanski is!

Two points. First, the tsunami of ridicule building around Jason Arday assures that he will be consigned to the graveyard of exposed fraudsters. Already the memes are burgeoning. Jason Arday beat out Neil Armstrong to be the first man to walk on the moon. The Bayeux Tapestry is making a long stop at the British Museum. You'll see that Jason Arday occupies a prominent place in it and was, in fact, responsible for William's victory at Hastings in 1066. Arday was also there with Nelson on the Victory at Trafalgar in 1805. I've seen the picture. "Historians now believe Britain would never have achieved naval supremacy without him." Ha, ha.

That's the droll side. But we must not let it conceal the dour reality that underpins the comedy. Which brings me to my second point: to wit, the politically inspired intellectual bankruptcy of the University of Cambridge. X recently listed "Cambridge Gender Studies PhD Topics Draw Online Mockery" as trending. Quite right, too. Here are a few:

Et very much cetera.

And then there is Hilary Cremin, a senior professor and dean of faculty in the Faculty of Education at Cambridge. A friend sent me her personal profile:

She co-chairs the THRiVE research group, whose professors and researchers investigate human thriving in and through Education. This includes topics such as wellbeing, peace education, conflict, equity, inclusion and social justice. Together the group has a significant portfolio of research and publication.

Hilary's own work focusses on Education, Peace and Conflict, whether this is: inner peace; interpersonal conflict resolution; social / community peace; global peace; or peace with the planet and non-human species. Her book Positive Peace in Schools with Terence Bevington outlines a framework for peace education in schools and communities. It forms the basis for her most recent peace education research project - the Cambridge Positive Peace Hub - which is creating an interactive digital platform for schools globe whilst supporting a global network of peace educators, researchers, policy-makers. visionaries and young people.

Hilary's most recent book Rewilding Education calls for an urgent global conversation about the aims and purposes of education in times of existential crisis. It proposes radical change, moving from education as monoculture to education as ecosystem. Learning in and through Nature, and in embodied and contextualised ways are highlighted in case studies from around the world Hilary uses the arts, auto ethnography and poetry in her research. She welcomes approaches from collaborators also interested in these methods and ideas.

Cambridge has a lot more than Jason Arday to worry about.

Roger Kimball is editor and publisher of The New Criterion and the president and publisher of Encounter Books. He is the author and editor of many books, including The Fortunes of Permanence: Culture and Anarchy in an Age of Amnesia (St. Augustine's Press), The Rape of the Masters (Encounter), Lives of the Mind: The Use and Abuse of Intelligence from Hegel to Wodehouse (Ivan R. Dee), and Art's Prospect: The Challenge of Tradition in an Age of Celebrity (Ivan R. Dee). Most recently, he edited and contributed to Where Next? Western Civilization at the Crossroads (Encounter) and contributed to Against the Great Reset: Eighteen Theses Contra the New World Order (Bombardier).

Tyler Durden Mon, 08/10/2026 - 14:00Authored by Naveen Athrappully via The Epoch Times,

There were 666 commercial Chapter 11 bankruptcy filings made in the United States in July, a 27 percent drop from a year ago, according to the American Bankruptcy Institute (ABI).

Chapter 11 bankruptcy allows a business to reorganize its debts so it can continue operating and eventually become solvent. In addition to a decline in Chapter 11 filings, overall commercial bankruptcy filings declined in July, falling by 8 percent year over year, ABI said in an Aug. 6 statement.

The decline in July's commercial filings followed improved economic conditions in June. The 12-month inflation rate declined in June from the previous month after surging for three consecutive months.

According to a July 24 report from S&P Global, U.S. business activity growth accelerated to an eight-month high last month, with business confidence in the year-ahead outlook rising to an eight-month high as well.

ABI clarified that although the number of Chapter 11 filings fell this year, more than 300 filings were made in connection with a large healthcare system's bankruptcy.

A hiring ad at a store in Columbia, Md., on Sept. 18, 2025. Madalina Kilroy/The Epoch Times

A hiring ad at a store in Columbia, Md., on Sept. 18, 2025. Madalina Kilroy/The Epoch Times

Meanwhile, despite the overall decline in Chapter 11 filings, subchapter V bankruptcy elections within Chapter 11, which represent filings by small businesses, rose 24 percent in July from a year earlier.

This is despite an improvement in small business optimism in June, according to a July 14 statement from the National Federation of Independent Business (NFIB).

NFIB chief economist Bill Dunkelberg said in the statement that lower fuel costs provided relief for businesses, with companies expecting operating conditions to improve over the coming six months.

"While there have been improvements in the overall environment, high interest rates and modest economic growth are causing owners to approach hiring and capital spending with caution," Dunkelberg said.

Total subchapter V elections in July totaled 234 filings, ABI said in its recent statement.

Amy Quackenboss, ABI executive director, said in the statement that bankruptcy serves as a "critical safeguard" for businesses to reorganize their finances and move forward under conditions of financial distress.

"ABI appreciates the continued efforts of Congress to permanently expand access for both distressed small businesses looking to restructure under subchapter V and for consumers looking to file under chapter 13," Quackenboss said.

Quackenboss was referring to the Bankruptcy Threshold Adjustment Act of 2026 introduced in the Senate by Sen. Chuck Grassley (R-Iowa) in March.

The Act seeks to permanently raise the small-business Chapter 11 bankruptcy debt threshold to $7.5 million. This threshold is the maximum debt limit a business can have when applying for such bankruptcy.

On Aug. 3, the Senate passed the bill. The legislation now heads to the House of Representatives for approval.

In an Aug. 4 statement from Grassley's office, the lawmaker commended the Senate for unanimously passing the Act.

"Our nation's bankruptcy code should work for Americans, not against them," Grassley said in the statement, while calling on members of the House to quickly pass the legislation.

"By eliminating barriers to reorganization and restoring modern debt limits, the bipartisan Bankruptcy Threshold Adjustment Act would provide American families and small businesses the tools they need to regain their financial footing in a quicker, more streamlined process."

The bill also seeks to raise the debt limit for Chapter 13 filings by individuals to $2.75 million.

Meanwhile, the Trump administration has taken action to ensure businesses have access to sufficient financing to operate.

On July 4, a new policy went into effect that allows businesses to secure up to $10 million by combining two Small Business Administration (SBA) loan programs - 7(a) and 504 loans.

The 7(a) loan program provides financial assistance of up to $5 million, while the 504 loan program has a maximum limit of $5.5 million. Previously, a business could only take $5 million cumulatively from both initiatives. The new update effectively doubles this threshold.

On July 30, the SBA announced that it would update its website to make it more helpful to small businesses and manufacturers.

The update offers a streamlined online lending process for businesses that "simplifies how lenders originate and process SBA-backed loans, helping them deliver capital to Main Street businesses faster and with greater consistency and security," the SBA said.

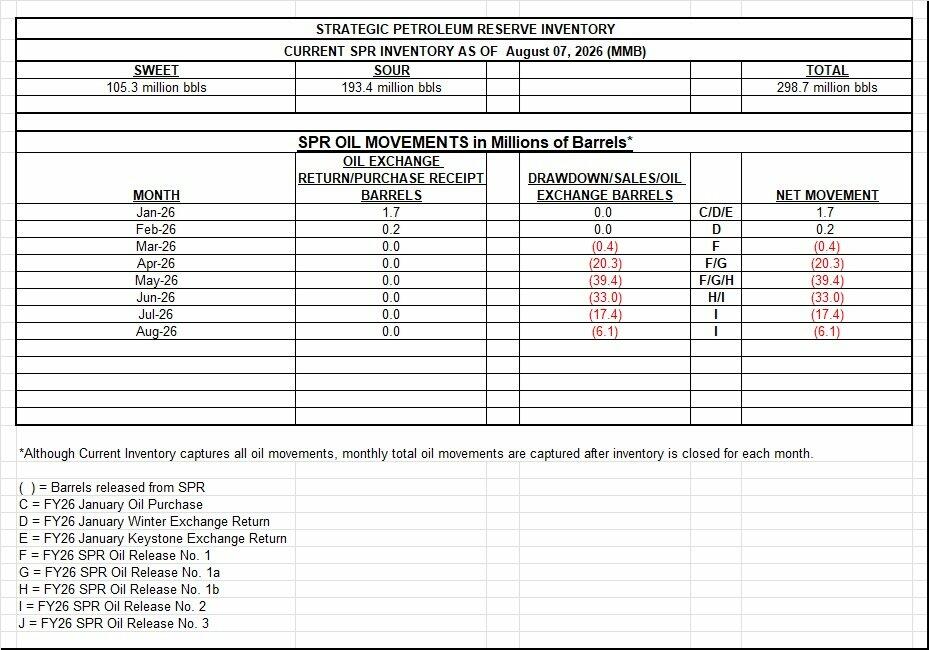

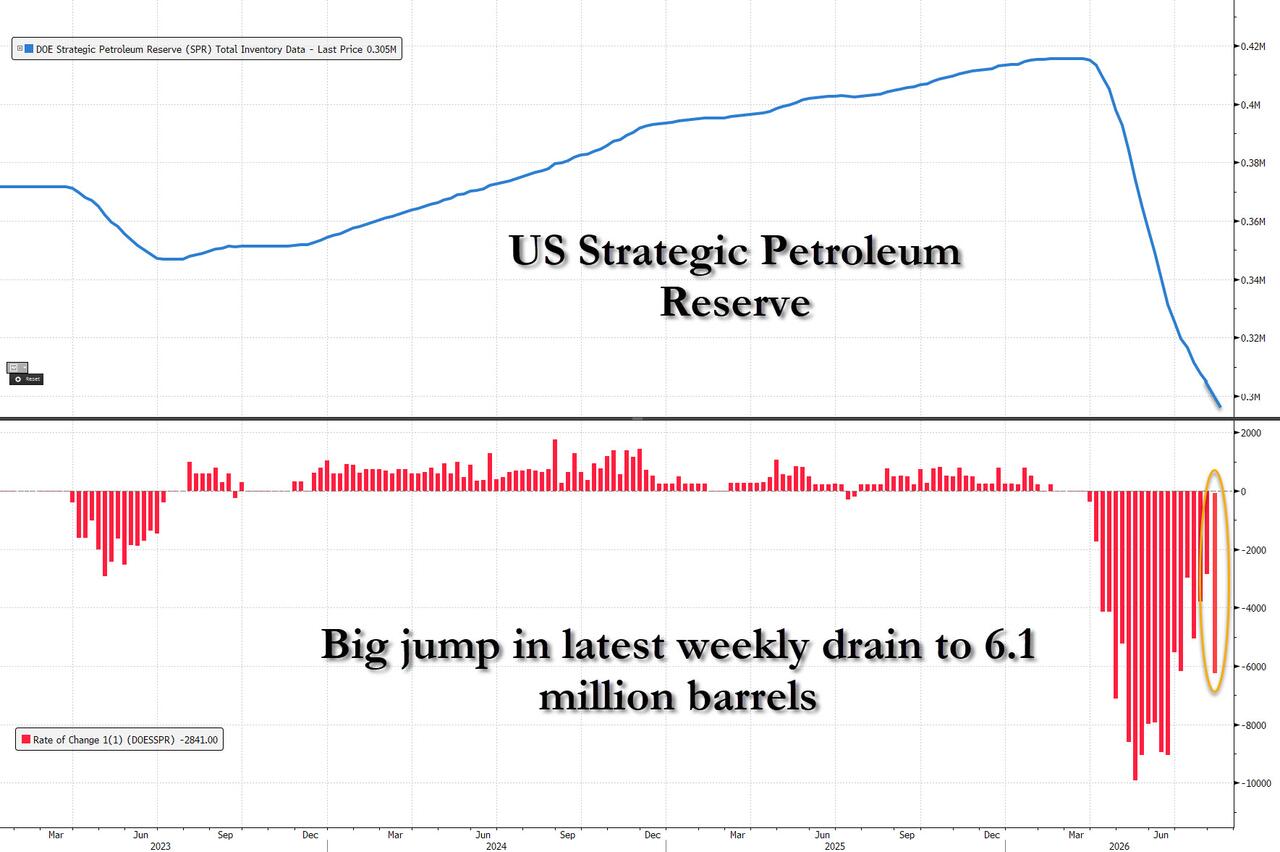

Tyler Durden Mon, 08/10/2026 - 13:25As negotiations between the US and Iran to reopen the Strait of Hormuz go nowhere, oil prices continue to slide lower on some naive hope that a resolution to the conflict will magically emerge. Meanwhile, both commercial and strategic stocks continue to be drained at a historic pace, and one day virtually every tank bottom will be hit, sparking a historic surge in commodity prices as the market realizes that physical always wins the war with paper oil.

That day just got closer today when the US reported that crude oil stocks in the Strategic Petroleum Reserve fell below 300 million barrels for the first time since early 1983, as global inventories are under pressure due to the Iran war.

The SPR fell by 6.1 million barrels to 298.7 million barrels last week, according to data released by the Department of Energy on Monday. The reserve is at its lowest level since January 1983.

The 6.1 million drain was a big jump in the SPR's recent moderating trend which saw the previous week only 2.8 million barrels exit the strategic reserve. Instead, the outsized outflow which was the biggest in almost 2 months suggests that US reserves are once again working overtime to prevent the oil price frrom spiking.

Yet as we have repeatedly explained, it is only a matter of time before the SPR can no longer be used to plug the gap so to speak. That's because the oil industry has generally accepted that the operational minimum for oil in the SPR, a point at which it would be more difficult to pump out the oil, is somewhere between 250 million and 300 million barrels. Meanwhile, sizing studies done on the SPR in the 1970s recommended an inventory minimum of 250 million barrels.

In other words, the US is already if not at the operational minimum, it will certainly hit it in a few weeks, should the weekly drain persist at this rate.

The rapid drain of the SPR explains why, according to unconfirmed reports, Iran has "completely ruled out any future negotiations with the Trump administration," declaring it will wait out Donald Trump's term until January 20, 2029, per Iranian outlets and Ghalibaf advisor's post.

"Trump will not reach an agreement with us. We will accompany him until his term ends," said Majid Shakeri, advisor to Parliament Speaker Ghalibaf.

He posted: "The path to victory is neither fighting nor a deal — it is managing the process of neither war nor peace, up to the point of victory. Publicly confirming negotiations with the U.S. is sheer folly. The winning approach is denial, ambiguity, and strategic patience."

The US release is part of a coordinated action by countries in the International Energy Agency to support the global oil market with 400 million barrels, although the US has been by far the most aggressive lender of its strategic reserves.

The drain began after Trump ordered the release of 172 million barrels in March to help address the oil supply disruption triggered by Iran’s attacks on tankers in the Strait of Hormuz.

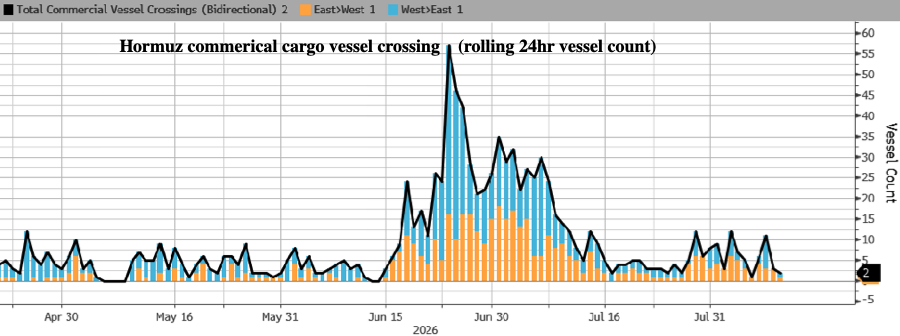

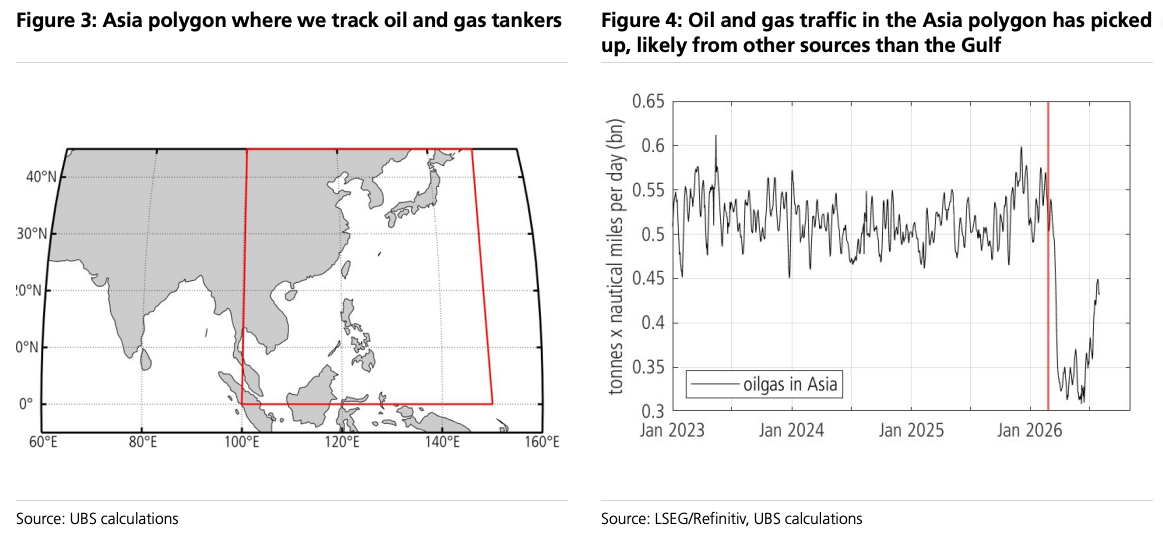

Tyler Durden Mon, 08/10/2026 - 12:55The latest Bloomberg data show that shipping transits through the Strait of Hormuz remained largely disrupted Monday morning, even as Iran and Oman reportedly moved closer to a deal.

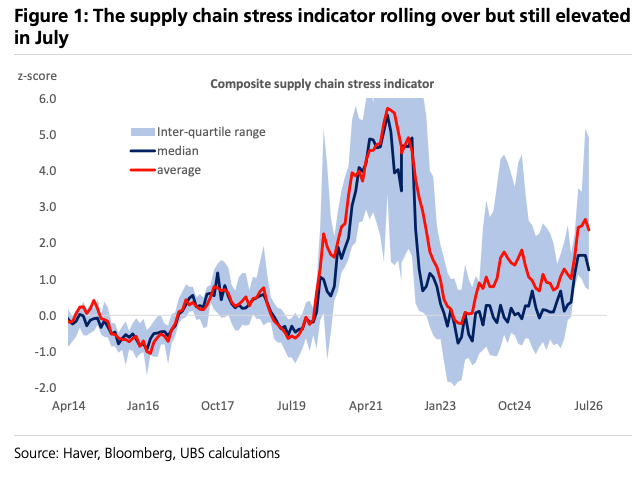

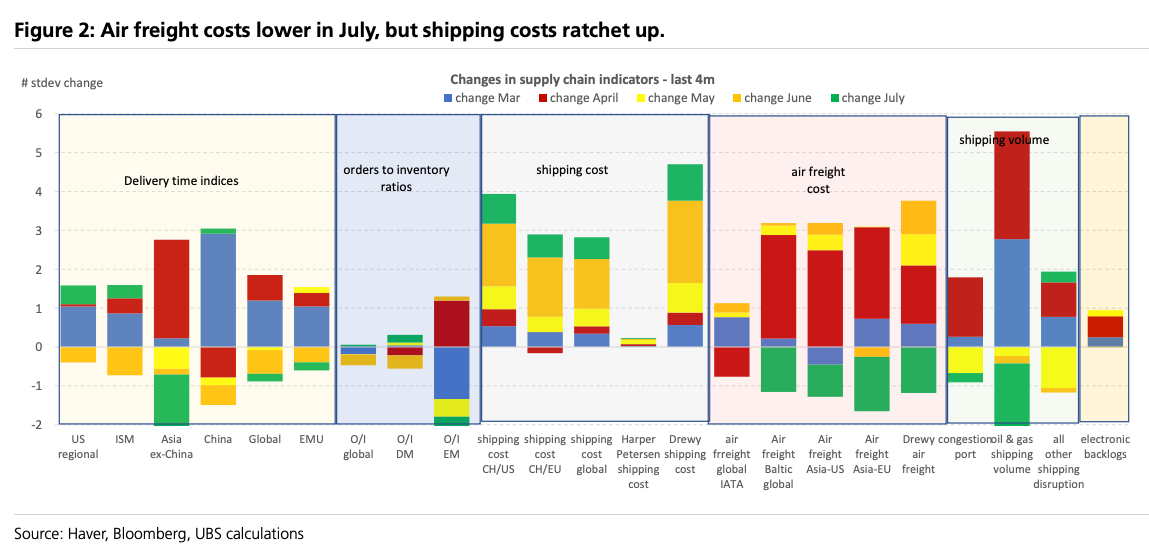

Brent crude futures traded near $85 a barrel as markets priced in the possibility that a deal to reopen the maritime chokepoint could be imminent. Yet global supply-chain stress remains near its highest level since the pandemic, and any normalization could take months, even if shipping traffic resumes.

UBS senior international economist Pierre Lafourcade highlighted the bank's proprietary Global Supply Chain Stress Index, which showed that although pressures eased modestly in July from their highest level since the pandemic, disruptions stemming from the Hormuz chokepoint continue to strain global shipping networks.

The median reading of the bank's 23-component Global Supply Chain Stress Index fell .4 standard deviation from June but remained .9 standard deviation above its pre-Iran conflict level. The average reading declined .3 standard deviation from June while remaining 1.35 standard deviations above February, or pre-US-Iran war, levels.

Lafourcade adds more color here:

Marginal relief for supply chains relative to the June peak

With the July data now complete, our Global Supply Chain Stress Index is showing a modest easing in pressure from the June reading, which marked the highest level of stress since the pandemic. Figure 1 below shows the latest reading.