Or....

Shadow Bankers Gone Wild

Preamble

Recently the New York Times published yet another article expressing surprise at the previous existence of securitized financial instruments prior to the last several decades. Securitized financial instruments, or actually securitization, has been around for at least several centuries, and whenever it becomes widely used a Great Depression, or economic meltdown, ensues.

This is the foundation for that bandied about term, “shadow banking.” Without securitization, there would be no such capability. With securitization, the process for creating debt-financed billionaires and multi-millionaires reaches critical mass.

Unfortunately, so to does the dramatic increase in unemployment and poverty.

Those so-called “experts” or “pundits” who continue misleading the populace with extravagant claims as to the recent origins of the securitization process have done a major disservice to society. This brief blog will attempt to rectify this situation.

Historical Background

Securitization: borrowing backed by securities or the transforming of debt into securities.

Samuel W. Straus is credited with originating the first mortgage security with a senior claim, circa 1909.

Over the next two decades (1910-1929) the securitization of mortgages became quite popular, although second liens rendered these financial instruments fragile, with the Great Depression removing them from the table.

Securitization of mortgages began anew in the 1970s, with the US government-sponsored National Mortgage Association and their “Ginnie Mae passthrough.” These mortgage-back securities (MBS) have grown enormously since then, as evidenced by recent years’ publicity correlating to the economic meltdown. [1]

A frequently misunderstood, or ignored, circumstance, is that the greater the debt, the more numerous or greater in number the MBSes; hence all those zero-money down mortgage loans. (Please remember – debt is everything!)

Naturally, this process is supposed to be structured to transfer risk to the bondholders, and sometimes it does actually work out that way. And who are those principal bondholders?

Frequently they are pension funds and endowment funds.

(Say, how’s that Harvard Endowment Fund working out for you, Mr. Larry Summers?)

The holders of mortgage-backed securities would be financially hurt if the majority of homeowners, in a given pool, prepaid their mortgages, of course, but should be disastrously hurt when any defaults occur, unless specific “event triggers” are written into those bond arrangements. One can surmise, by the losses to the Harvard Endowment Fund, that such triggers weren’t present in great number.

I guess Iris Mack knew what she was talking about when she tried to warn then-Harvard Dean Larry Summers about their precarious finances. (Sure am confident that President Obama appointed Mr. Summers to his administration.)

When securitization – of anything – exists opaquely, that is, with no transparency, and can be used in ultra-leveraging, both in speculation of commodities and stocks and other areas, we find the causes for the surplus of debt-financed billionaires and millionaires, while the subsequent ultra-deleveraging destroys what remains of the economy for the (majority) rest of us.

Another take on the history of securitization can be obtained from Prof. George Jackson’s (University of Minnesota Law School) excellent Research Guide on Securitization :

Securitization originated in the 1920s when mortgage insurance companies sold guaranteed mortgage participation certificates for pools of mortgage loans. Investors actively traded these certificates until the real estate market crashed during the Great Depression. In the late 1970s and early 1980s securitization rose like a phoenix from the ashes. The twin energy crises of the 1970s wreaked havoc on the economy and banks experienced severe disintermediation. Freddie Mac – a federal purchaser of mortgages from members of the Federal Reserve System – responded to this by taking legislative initiatives to improve liquidity in the secondary market for mortgage loans so as to increase the availability of investment capital for housing finance.”[2]

Many years ago, I attended a talk given by the late and great progressive economist, John Kenneth Galbraith, on the causal factors leading to the Great Crash and the subsequent Great Depression.

In this talk he described not only mortgage securities (and some interesting financial manipulation and speculation by Goldman Sachs) but also what could best be described as securitization of stock pools leading to the stock market crash.

Although Prof. Galbraith never used the term “securitization” which didn’t exist at that time, only coming into the lexicon in the decade of the 1990s, he succinctly described this process involved with the extreme leveraging of stock pools.

So, will I now segue into the natural discussion of CDOs, or CMOs, or CLOs, or ABSes, or MBSes, or CDSes, or ABS of CDS, or synthetic CDOs, or CPDOs, or securitized notes of all variety, or ABCP conduits?

Nope. Let's look at the securitization of toll roads.

The Privatization of Everything: The Securitization of Everything

While the process of securitization can sometimes be excused on the financial support level, the people and groups behind the privatization of everything always appear to also yearn for the securitization of everything; a most unnecessary and expensive proposition for the rest of society.

Whenever one hears or reads about a “public-private partnership” about to come into existence, it is best to run for the hills, or at least keep one’s hand tight upon their wallet, check their connecting chain to their jeans, or double-check their billfolds.

Each and every time one hears this phrase, securitization almost always seems to be the outcome along with that privatization thing.

Please click to enlarge

From Professor Steven M. Davidoff, University of Connecticut School of Law, one hears the support for the rampant use of securitization as shown in the quote below.

The rise of securitization and derivatives has allowed capital and risk to be allocated differently and more efficiently. In the process, finance has become more accessible and cheaper. Companies can obtain more funds to spur further growth and, consequently, there has been a productivity growth in our American economy. This includes the $1.2 billion invested in green technology in the second quarter of 2009 alone, according to Greentech Media.[3]

Prof. Davidoff’s implied assumption is that if Greentech Media states such investment is worthy, it must be so. Thanks to an excellent research method known as link analysis, originally conceived by the brilliant psychologist, Stanley Milgram (noted for his design of the chilling obedience-to-authority experiments and the creation of the “flash mob” concept, and popularized by radio DJs as “seven degrees of separation to Kevin Bacon” fame), one might research the financing and ownership behind Greentech Media.

(Hint: search the ownership behind one of their financial backers, Egora Holdings.)

If one were to find the financial backers to also be associated with both the financing of and also with, oil and energy speculation on the InterContinental Exchange (ICE), and ICE Futures, and ICE US Trust, and the oil companies, etc., one might arrive at the logical conclusion that Prof. Davidoff’s assumption was highly faulty, to say the least.

The Road to Perdition

Prof. John L. Goldberg, of the University of Sydney, published an outstanding study on financing aspects (securitization and financial engineering) of tolls roads and similar infrastructure projects titled: The Fatal Flaw In The Financing of Private Road Infrastructure in Australia, where he makes the following points:

Eight years of historic financial data has revealed the extent to which the financial outcome of the M2 Motorway was deteriorating despite having received about 35% of its revenue from interest derived from infrastructure borrowings. In 1999, the owners and operators resorted to a scheme known as “financial engineering” based on revaluation of the asset, well above its true economic worth, in order to provide security for increased borrowings out of which investor returns were paid.

Another prospective method of paying off debt involves securitization. In this case toll roads are grouped together in pairs so that cash flow or asset value of one serves as security for the debt of the other and a new financial instrument is created which is sold through capital markets. Recently, this use of securitization is admitted by the toll road promoters to be a high risk method of financing.[4]

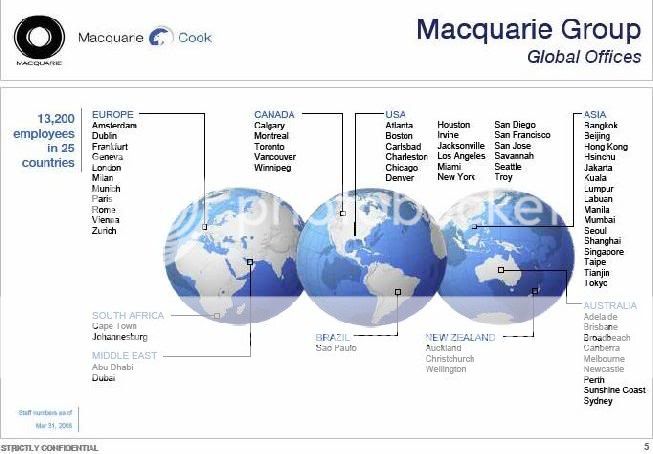

Please note that the first paragraph quote sounds remarkably similar to a private equity firm’s pump-and-dump scheme. Also, the second paragraph refers to processes found in many securitized instruments (CDOs, CMOs, CLOs, etc.) commonly referred to as pools, or pooling, and tranches. This securitization and financing package was undertaken by the Macquarie Bank (part of the Macquarie Group), with feasibility studies by the Macquarie Infrastructure Group.

Thought by many to be the number one promoter of public-private partnerships (PPP) on the planet, Macquarie is frequently involved in such activities (by way of the Macquarie Infrastructure Group, or other subsidiaries) throughout the globe, frequently working in conjunction with other major investment houses, such as Goldman Sachs International and Morgan Stanley.

The following three charts, from a government (EPA) site, present a generalized picture of the size of Macquarie.

Please click to enlarge

Please click to enlarge

Click Image to Enlarge

[5]

In his report the professor makes an interesting point on the content of Macquarie’s prospectus in particular, and other prospectuses in general, in the conveyance of rosy financial data, namely that the given examples of future returns to investors based up the internal rate of return (IRR), which the first few payments look positive, as opposed the actual return on investment (ROI), which, over the extended long haul appears none too profitable to the investor.

This is remarkably similar to what transpired in the state of Indiana (USA) when they leaped for the privatization of their toll roads under a Republican governorship. Throughout Prof. Goldberg’s report one finds numerous examples of “creative accounting” which, under closer scrutiny, doesn’t yield those promised profits and paybacks.

Of course, since these privatizations and securitizations involve former governmental infrastructure of necessity, it is an easy prediction that eventually the true costs will once again fall back upon the citizenry and taxpayers. And, as usual, the returns on such toll road operations, as we’ve seen in Indiana and elsewhere, also directly correlate to the state of the local economy.

And, of course, it is mandatory one quotes from the pivotal remark in his Executive Summary of his report:

Both the use of financial engineering and securitization tend to emphasize the intrinsic nonviability of toll road projects, a matter clearly not understood by those who have embraced the privatization of roads for ideological reasons. It would be of interest to know if such people approve of the financial manipulation necessary to keep these schemes afloat.[6]

A short backgrounder on Macquarie is in order, therefore I have inserted this quoted paragraph from an older Forbes Asia Magazine article.

Macquarie is best known for popularizing the privatization and securitization of all kinds of public infrastructure--first toll roads and later airports, water utilities, ferries, ports and even retirement homes. In general Macquarie bids for the right to build or manage infrastructure-related monopolies and collect the tolls or the landing fees. The capital usually comes from investment funds it manages on behalf of institutions or small investors. It makes part of its living from fees on those funds. This has goosed Macquarie profits while providing an argument to the bearish James Chanos of Kynikos Associates, a New York hedge fund, to short the stock. He says the model works only when debt is cheap and asset prices are rising.[7]

RiskMetrics Group, the corporate governance group and financial analysis think tank based in New York, published a thoughtful and critical report on the Macquarie Group back in 2008.

Some of their criticisms:

…high debt levels, high fees, paying distributions out of capital rather than cashflow, overpaying for assets, related-party transactions, booking profits from revaluations, poor disclosure, myriad conflicts of interest, auditor conflicts…[8]

The Indiana Toll Road (ITR), advertised as the “Main Street of the Midwest,” became a privatized and securitized, public-private partnership, at the beginning of 2006. The new operator for the next 75 years is Statewide Mobility Partners LLC (SMP), a limited liability company between Cintra Concesiones de Infraestructuras de Transporte SA (Cintra) and Macquarie Infrastructure Group (MIG), as a result of their highest bid of $3.8 billion USD.[9]

Click Image to Enlarge

The following quote originates from an Indiana University report published by Dr. Craig Johnson et al., from their School of Public and Environmental Affairs.

The ITR privatization will result in substantial, long-term toll rate increases which will reduce the consumer surplus long enjoyed by ITR motorists. The non-compete clause limits the public sectors flexibility in responding to the future needs of motorists, but the transaction helps the state of Indiana solve the current road infrastructure financing crisis as well as improve and expand the state highway system without relying on tax increases.[10]

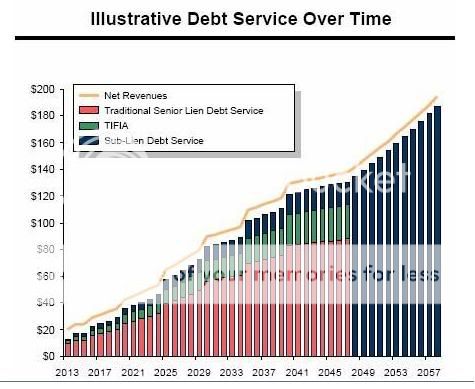

The wonderful circumstances of these privatized and securitized toll road projects, is the colossal amount of debt taken on, the direct correlation to the state of the economy and price of oil, and the abysmally bad financial numbers.

A chart of some of this debt, as displayed in a Goldman Sachs’ presentation:

Click Image to Enlarge

And a financial snapshot of a typical year (one hopes), 2007:

Interest costs total on that colossal debt: $239 million

Actual cash interest costs (money paid out): $141 million

Gross tolls and other revenues: $151 million

Cash operating costs: $40 million (but as can be seen from the previous numbers, only $10 mil remains)

Losses: $32 million (Macquarie and Cintra estimates)

And part of the deal is the upkeep and expansion of the toll road through the Midwest.[11]

As Prof. Goldberg (University of Sydney) pointed out in the previously mentioned report he authored, the payment of equity dividends with no cash flow available seems to be a frequent, and very troubling, occurrence in the securitizing of toll roads and infrastructure projects.

Whatever became of real accounting and real finance?

From a Public Interest Network analysis report we learn that Macquarie sent their investors a presentation proposing a 15-year payback to equity.[12] Given that their (the Macquarie and Cintra) deal is 75 years long, and given the 2007 numbers, not to mention the continuing state of the economy, which appears to have hit the much privatized and securitized infrastructure of Indiana considerably harder than elsewhere, such a proposal appears to exist in the realm of speculative fiction,

Truth to tell, does any financial institution really expect to profit, or realize profits directly from any of these public-private partnerships? Hardly, they gain from peddling the debt and all such fees, valuations and payoffs from such deals.

A Government Accountability Office (GAO) study found that such outsourcing diminishes existing or in-house expertise, which suggests the states ability to oversee future projects highly questionable.[13]

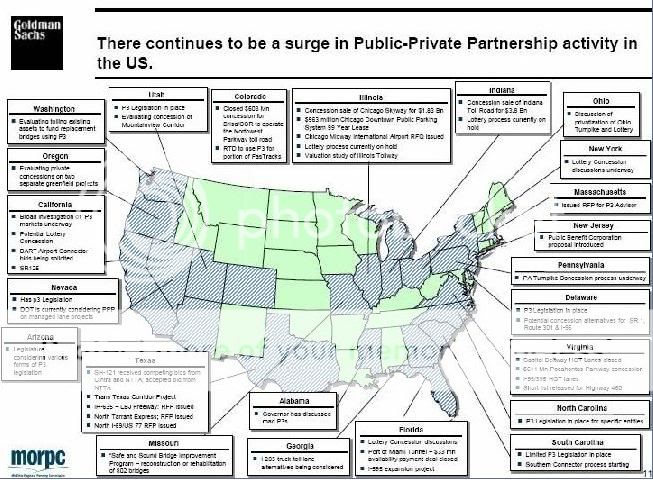

Oh, and by the way, Goldman Sachs does love those public-private partnerships.

Please click to enlarge

Click Image to Enlarge

Dick Cheney’s Godson

Back in the decade of the 1990s, Dick Cheney’s godson, one DJ Gribbin IV, offspring of DJ Gribbin III, Dick Cheney’s best buddy whose career shadowed Mr. Cheney’s (on his staff when Cheney was in congress, later his executive VP when Cheney was with Halliburton, etc.), served as the national field director for the Christian Coalition.

A confirmed cynic might suggest this to be the perfect position for garnering support for a future president. Later, after George Bush began his occupancy of the White House, DJ Gribbin IV moved from the Christian Coalition to the DOT, then back to a position as division director at Macquarie Holdings, Inc. (there’s that Macquarie name again!), then back to Bush’s DOT (Department of Transportation).

With the advent of the Obama Administration, Gribbin moved back to doing the lord’s work: advocating for the privatization of all toll roads in America at Macquarie Capital (there’s that Macquarie name again!).[14]

Like godfather, like godson.

Summation

I am now going to make an assertion, probably obvious to some who are conversant in these subjects, and perhaps new to others who aren’t quite as well informed on the matter.

The overall process of securitization, whether it be coupled with credit derivatives or utilities or toll roads or some other construct, is fundamentally a leveraged buyout, exactly the same as a private equity leveraged buyout (normally following a “pump-and-dump” profile). The major qualifier is that the securitization process is the superset, while the PE leveraged buyout is a subset.

Or phrased differently, securitization is the metapattern, while the other categories and subcategories represent the smaller patterns.

In other words, they are all intrinsically connected, and cannot really be separated, which was why the tax structure was so efficiently restructured over the preceding forty-some years.

It is important to remember the primary product of Wall Street: the peddling of debt.

Often one hears of the necessity of Wall Street bankers for providing seed money for industry; but year after year we have observed them dismantling factories and shipping them overseas. We have observed them dismantling production facilities and shipping them overseas. We have observed them dismantling research and development laboratories and shipping them overseas

And year after year we have observed them ship all those jobs and careers overseas along with those facilities.

Dismantle, dismantle, dismantle is what we have observed. They securitize, and promote the privatization and securitization of everything. Then they transfer their private debt, from whence their millions and billions flow into their coffers, to the public, and then it becomes the public debt (or rather the public’s debt!).

The two principal factors in the ever burgeoning federal debt is that transference of their debt (the Treasury issuing all those Treasuries which the Federal Reserve gives to the largest banks in exchange for their highly questionable – i.e., toxic assets – credit derivatives), and the expenditures for wars (i.e., death profiteering and war profiteering).

And what is the point? To enrich a few and to impoverish the many. As usual.

With the Obama Administration’s reappointment of Bernanke (it was done by congress, but with the strong support of the president), unemployment will continue to rise as Bernanke’s programs contravene Say’s law.

The liberty of a democracy is not safe if the people tolerate the growth of a private power to a point where it becomes stronger than their democratic state itself. That, in its essence, is Fascism—ownership of government by an individual, by a group or by any controlling private power. —Franklin Delano Roosevelt to the Congress, April 29th, 1938

Notes

- Chorafas, Dimitris N. (2005). The Management of Bond Investments and Trading of Debt, pp. 135-139. Massachusetts: Elsevier Butterworth-Heinemann. ISBN 0-7506-6726-5

- Jackson, George, Professor. Research Guide on Securitization, Fall 2001, Advanced Legal Research, p. 3

http://www.docstoc.com/docs/906179/securitization-process - Davidoff, Steven M., Professor, University of Connecticut Law School, Inevitability of finance

http://dealbook.blogs.nytimes.com/2009/10/07/the-inevitability-of-financ... - Goldberg, John L., Professor. Australasian Transport Research Forum (ATRF06) Brisbane. Executive Summary: The fatal flaw in the financing of private road

infrastructure in Australia. School of Architecture, Design Science and Planning, University of Sydney, 2006

http://wwwfaculty.arch.usyd.edu.au/web/staff/homepages/pdf/johngoldberg_... - http://www.epa.gov/region6/6sf/pdffiles/lrb2g_costenbader.pdf

- Goldberg, John L., Professor. Australasian Transport Research Forum (ATRF06) Brisbane. Executive Summary: The fatal flaw in the financing of private road

infrastructure in Australia. School of Architecture, Design Science and Planning, University of Sydney, 2006

http://wwwfaculty.arch.usyd.edu.au/web/staff/homepages/pdf/johngoldberg_... - Meredith, Robyn and Heuslein, William. Forbes Asia Magazine, "Millionaire Maker." May 19, 2008. http://www.forbes.com/global/2008/0519/014.html

- West, Michael. Sydney Morning Herald Online, "Macquarie Model Blowtorched." April 4, 2008.

http://www.smh.com.au/business/macquarie-model-blowtorched-20080404-23oy... - From the Indiana Toll Road official web site:

https://www.getizoom.com/aboutITR.do - Toll Road Privatization Transactions: The Chicago Skyway and Indiana Toll Road. By Dr. Craig L. Johnson, Martin J. Luby and Shokhrukh I. Kurbanov, School of Public and Environmental Affairs, Indiana University. Sept. 2007

http://www.cviog.uga.edu/services/research/abfm/johnson.pdf - Gelanis, Nicole. NY Fiscal Watch site: Toll-road intrigue: The Indiana deal could set a different precedent…. Jan. 28, 2009

http://www.nyfiscalwatch.com/?p=862 - http://cdn.publicinterestnetwork.org/assets/H5Ql0NcoPVeVJwymwlURRw/Priva...

- Private Roads, Public Costs: The Facts About Toll Road Privatization and How to Protect the Public. U.S. PIRG Education Fund. Phineas Baxandall, Ph.D., US PIRG Education Fund, Kari Wohlschlegel and Tony Dutzik, Frontier Group. Spring 2009.

http://cdn.publicinterestnetwork.org/assets/H5Ql0NcoPVeVJwymwlURRw/Priva... - http://www.tollroadsnews.com/node/3980

http://www.tollroadsnews.com/node/4165

Reference

Goldman Sachs Presentation: Texas Transportation Forum

You Bet Your Assets: Leveraging Existing Infrastructure

Current Opportunities in the US PPP Marketplace

By Gregory B. Carey, Managing Director, June 9, 2006

Meta:

- infrastructure

- goldman sachs

- shadow banking

- securitization

- PPP

- Public-Private Partnership

- University of Sydney

- Christian Coalition

- Cintra

- Craig Johnson

- DJ Gribbin III

- GAO

- Halliburton

- Indiana

- Indiana Toll Road

- John K. Galbraith

- John L. Goldberg

- Macquarie Infrastructure Group

- Public Interest Network

- Risk Metrics

- Samuel L. Straus

- Say's Law

- Steven M. Davidoff

Comments

Great Post

I don't know about psychology, links and 6 degrees of separation, but I do know about vested interested parties funding "research", sometimes through a 3rd party to justify whatever short term profit or goals they want to do...regardless of it's affects on the national interest or even long term health of the same company.

We are seeing more and more biased research, white papers where one is only going to find the flaw if:

1. You read the white paper

2. you have advanced mathematics

3. you have advanced economic theory

4. you review raw statistics

I mean from drug trials to policy to the obvious outrage, writing a white paper to justify getting funds from the government for your particular investments or privatization schemes you want to do.

I edited the formatting a tad, your post tells me I need to get better formatting, esp. graphics tools NOW! My apologies, it's clear a lot of the site tools are not adequate.

BTW: There is a slew of "immigration" "papers" right now that try to claim unlimited migration "helps the economy". This is really sick. What they are doing, which is truly dishonest, not only from the theory, but also the raw statistics, is putting the labor substitution coefficient to zero, in a nutshell. This is just the equations, ignoring the other elements in wages, overall costs. In English, these biased papers are trying to claim that U.S. workers are not displaced and that is just very obviously false from the data on what's happening on the ground.

So, we also have people, with their philosophies trying to make something so, which is objectively incorrect.

Anywho, for someone who takes the scientific method seriously, who believes that the entire world was built upon objective science, methods and analysis...

this trend is really disturbing to me. It's cutting down objectivity itself and so you are turning supposed objective experts into glorified lobbyists with bad math.

Most people in the United States cannot add two numbers together. They know something is wrong with this picture but who can drill down into the actual theory to see clearly....someone just biased a mathematics equation by setting a known quantity, represented by a host of variables....to zero in order to get their conclusion to work out they want they want it to.

Thanks

Thanks for the formatting. I did a sloppy job because shrinking those Macquarie charts down made them difficult to read, but it does look better!

Agree with everything you said, of course. My main point, besides the lack of history on securitization (by those supposed experts) which is crucial to understanding what's going on, was to get across the idea of the linking of securitization to all those debt-financed billionaires now smelling up the landscape -- and to further the concept that securitization, the way it is presently handled at least, is nothing more than a humongous leveraged buyout of leveraged buyouts against the American people and workers.

Thanks again.

automatic graph scaling

I am out for a solution that the site does and doesn't require special HTML to do it. For now there is a "Zoom" outlined in the admin forum and you can put very large graphs on size them down and put the "click on image to enlarge".

But this is obviously way too difficult, so what am I saying, well, don't worry about it. I simply need to get the upgrades done and solve this problem.

Part of the problem is the dire straits of states and cities

City of Chicago sold the Chicago Skyway - part of the Indiana Toll way deal. It sold a portion of its elevated train system (the EL). It is contemplating selling Midway Airport and its water system.

RebelCapitalist.com - Financial Information for the Rest of Us.

RebelCapitalist.com - Financial Information for the Rest of Us.

True, but they are only making matters....

...worse, when the privatize and securitze their infrastructure, as the way those deals are structured, and they are always structured differently where the very rich are concerned, they don't simply go into bankruptcy like the average person, then forfeit the property, or operation, or revenues; instead they have made off with the profits of peddling all that debt, and the debt always seems to get transferred.

So, the pension funds of unions, especially the super-sized ones (known as superannuation funds), are used to undermine employment, and the local and state tax bases.

Definitely almost exactly the way a typical private equity leveraged buyout works.

It all appears to fit the same pattern. And look what bad shape with Indiana trying to privatize and securitize everything in that state; their public transportation service has been continued in some cities due to lack of funds, their water usage becomes more expensive, etc., etc.

Also, a general FYI I recently chanced upon -- in case anybody else was unaware of the specifics -- the anti-usury laws at the federal level were effectively nullified by a 1978 Supreme Court case (1978 Supreme Court decision in Marquette Bank v. First Omaha Service Corp.) which stated that the home state's usury laws superceded the federal law, thus allowing the credit card operations of various banks and financial services, to relocate to the two states with the laxest of laws: Delaware and South Dakota.

Hi I am from Slovakia - a

Hi

I am from Slovakia - a small central european country, PPP projects are here on the rise since there is only little left for privatization (prefered way in the past of wealth transfer aka theft). In short time our government will sign a bulk of PPP project for motorways, we will pay for 30 years an amout that equals about maximum (per year) of what we had so far invested in highway construction. I know, nonsence. I am trying to tell my friends and people I know but only few people get it since this quite new and unknown.

I wonder how many degrees are between the companies you mentioned and the ones that are going to rob us here.

Thanks for your comment, AB

You make an excellent point, one I didn't really explain too well, and your point amplifies the fact that this situation is global in scope, whether it is happening in Slovakia, Australia, Peru, United Kingdom, or North America.

Your point about debt servicing, the payment for and to extremely long-term debt, along with all those processing fees, both of which are leveraged against.

They then generate securitized financial instruments (credit derivatives) against that debt (and debt servicing), adding more and more layers of securitization, then generate an almost infinite amount of credit default swaps, ostensibly to hedge against all those derivatives and deals; hence that ultra-leveraging.

And then the government (least ways in the USA), by way of the Treasury, generates tons of Treasuries (various bonds) to be exchanged by our Federal Reserve Banks for those credit derivatives and CDSes which have earned billions and billions of dollars for all those investment houses, big banks and financial services firms. Thus transferring private debt, yielding their fortunes, to public debt and the pillage and destruction of the public commons.

Prof. Goldberg (University of Sydney) makes a number of outstanding points in that cited report, one of which is:

(CCT refers to the Australian infrastructure project, the Cross City Tunnel)

That has bothered me for years, trying to ascertain where the revenue streams come from in so many of these cases, but as he ably demonstrates, they (banks, investment houses, etc.) are simply paying dividends to give the impression of revenue streams to acquire more investors, and more leveraging; using creative accounting techniques and double entries to hide non-amortization of debt, etc.

Public-private partnerships translate to private gain, public debt, and we observe that on all levels and now in across far too many countries.

A very sad and troubling thing indeed. My hopes with those Greek protesters today.

Stock Shock

President Obama, Bernanke, and Jim Cramer are in a MOVIE about hedge funds called "Stock Shock." Even though the movie mostly focuses on Sirius XM stock being naked-short-sold to near bankruptcy (5 cents/share), I liked it because it exposes the dark side of Wall Street and reveals some of their secrets. DVD is everywhere but cheaper at www.stockshockmovie.com