Futures Hit Record High As Oil Tumbles After Bessent Says Hormuz May "Reopen Tomorrow"

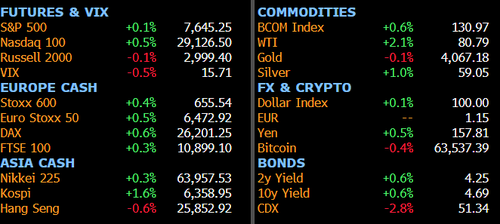

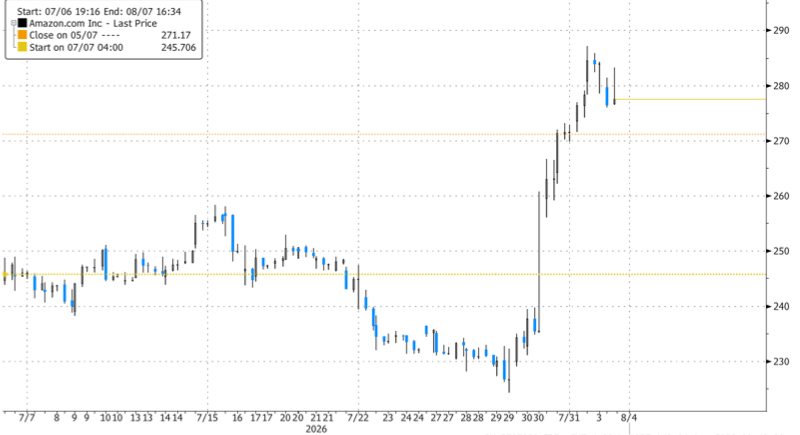

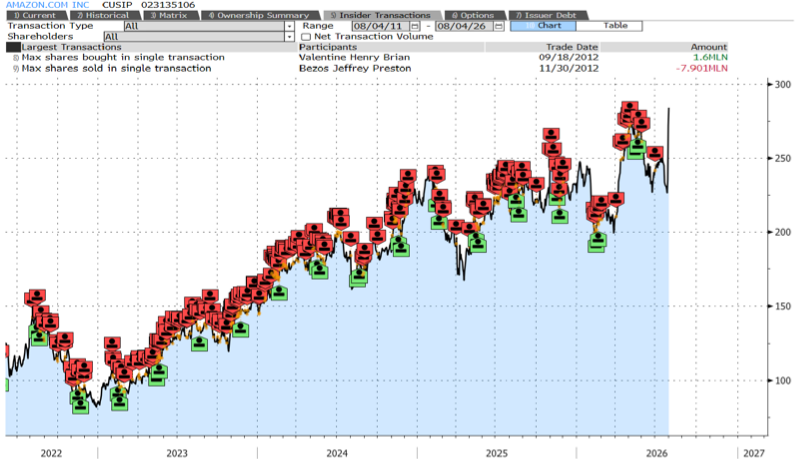

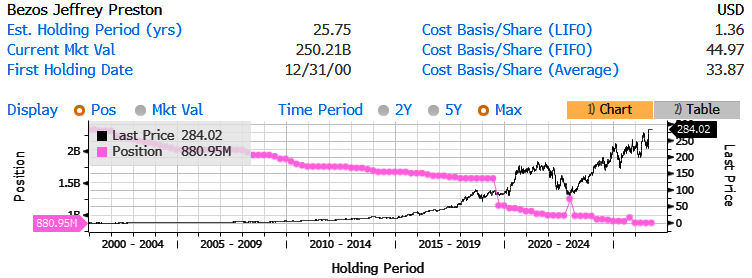

S&P futures are trading at all time high with the latest push higher triggered by comments from Scott Bessent on CNBC who echoed Trump in saying that "we may have Iran deal tomorrow to open Hormuz" (or we may not). The Nasdaq also looks set to extend Monday’s gains: As of 8:00am ET, S&P futures are up 0.4% to an all time high of 7655 and Nasdaq futures rise 1.1%, as Palantir soared 16% pre-market after upping its forecasts, while Caterpillar rose 9% on an earnings beat. Semis are leading the Tech tape with Mag7 (DRAM, EWY, SMH, SOXX all higher by at least 1.6%) while Mag 7 are mixed: Amazon (AMZN) falls 2% after founder Jeff Bezos filed to sell $4.07 billion of stock (Nvidia +1.3%, Tesla +0.6%, Apple -0.2%, Meta -1.7%, Alphabet -1.5%, Microsoft -2%). Cyclicals are leading Defensives with healthcare/staples lower pre-market. Bond yields are slide 2-3 bps on the drop in oil prices, and the USD is stronger as is USDJPY following a catastrophic 10Y JGB auction while intervention is not expected to have a lasting impact and the market is likely signaling the need for BOJ to hike. In commodities, WTI tumbles on Bessent's comments that we may have a deal to reopen Hormuz tomorrow (we won't) with WTI sliding as low as $76. Base metals are higher with Precious metals spiking and Ags bid. It’s a busy day, with earnings this morning from McDonald’s and Caterpillar, and the AI trade front and center this afternoon as AMD and SpaceX report. Today’s macro data focus is on JOLTS and trade balance.

In premarket trading, Mag 7 are mixed: Amazon (AMZN) falls 2% after founder Jeff Bezos filed to sell $4.07 billion of stock (Nvidia +1.3%, Tesla +0.6%, Apple -0.2%, Meta -1.7%, Alphabet -1.5%, Microsoft -2%).

- Ameresco (AMRC) rallies 30% after the energy company boosted its adjusted earnings per share guidance for the full year.

- BioNTech SE (BNTX) falls 3% after the company lowered its revenue outlook as demand for its Covid-19 vaccine shrank more than expected.

- Caterpillar (CAT) posted second-quarter earnings and revenue that beat Wall Street expectations as the company’s power-generation business continued to post strong growth off the back of data center spending. Shares are up 8%.

- DuPont de Nemours (DD) falls 3% after the chemicals company reported second-quarter results and gave a full-year forecast.

- McDonald’s (MCD) climbs about 2% after the fast-food restaurant owner and operator posted second quarter results.

- Nike (NKE) falls 3% after JPMorgan cut its recommendation on the sportswear and sneaker company to underweight, noting financial impacts from the company’s “Win Now” business strategy.

- Onsemi (ON) rises 7% after the chipmaker’s second-quarter revenue and earnings beat the average analyst estimate. Analysts note that AI data-center demand is boosting results.

- Palantir (PLTR) jumps 15% after the company boosted full-year revenue and income forecasts and described commercial demand for its data analytics tools as “otherworldly.”

- Powell Industries (POWL) drops 11% after the maker of circuit breakers and other electrical equipment posted fiscal third-quarter EPS and revenue that missed expectations.

- Rockwell Automation (ROK) falls 5% after the maker of industrial automation products posted third quarter results and provided a year forecast.

- Snap (SNAP) gains 5% after the the social media platform posted higher-than-projected quarterly sales and gave an upbeat forecast for the current period. The results signal optimism ahead of the September commercial debut of its first pair of augmented reality glasses.

- Spotify (SPOT) falls 4% after the music streaming service’s third-quarter monthly active users and operating income forecasts missed the average analyst estimate.

- Voyager Technologies (VOYG) rises 15% after the defense company raised its revenue outlook for the full year.

- Wayfair (W) falls 3% after the online furniture and home goods retailer posted second quarter results.

Corporate news is also busy, with Prologis set to buy UK REIT Segro for about £14 billion ($18.8 billion) and Williams reaching an agreement to buy Momentum Midstream through a deal valued up to $5.5 billion. HSBC’s CEO said the bank will consider boosting its bonus pool for bankers if strong performance continues. In AI news, the White House plans to host leading companies today to discuss a safety framework. Competition is heating up, especially from Chinese AI models, creating what’s been described as a death zone for anyone without frontier-pushing technology or market-breaking pricing. And AI is also shaking up the VC market, with money flowing disproportionately to top-tier investors that backed the technology early.

The rebound in US tech followed a volatile month as investors questioned whether billions of dollars of spending on artificial intelligence will translate into stronger growth and profits (they will... for Chinese AI models). The positive earnings season so far has eased some of those concerns, although the reality is masked under hundreds of billions in new debt. S&P 500 companies are beating expectations at a rate of 86%, the highest in five years, while year-on-year growth in earnings per share is running at 29%. Specifically, of the 322 S&P 500 companies to have reported so far this season, 86% have beaten analysts’ EPS forecasts, while 10% have missed. 68% of companies have positively surprised on sales, while 16% have missed.

“The combination of resilient economic growth, strong corporate earnings and AI-driven investment continues to provide a favorable backdrop for equities,” said Jeff Buchbinder, chief equity strategist at LPL Financial. “While investors are right to scrutinize elevated capital spending by hyperscalers and monitor developments in the Middle East, we believe these risks will be offset by the powerful earnings tailwind.”

However, as Bloomberg cautions, one potential pitfall for markets comes when SpaceX reports its first earnings as a public company later Tuesday. It also sets the stage for one of the largest share unlocks in capital markets history, with as much as $116 billion of stock becoming eligible for sale for the first time next month. SpaceX stock is about 15% lower than its closing price on June 11, when the shares started trading.

“The bigger issue for SpaceX remains the looming share overhang,” said Chris Weston, head of research at Pepperstone Group Ltd. “There is a sense that many investors remain interested in owning the stock but are waiting for the selling pressure associated with these lock-up expiries to begin fading.”

Elon’s rocket company isn’t profitable and has a very speculative model, so the results may end up raising more questions than they answer according to Bloomberg. Volatility could also be increased by technical factors: With a low free float, 95% of SpaceX stock available to borrow is out on loan, according to S3 Research data, amounting to 34% short interest as percentage of the float.

Total assets in US-listed leveraged ETFs have retreated from highs, reducing the market impact from daily rebalancing. Still, rotation trades are creating pain points for hedge fund consensus long versus short trades. And while US equities look fairly resilient on the surface, positioning data point to limited investor conviction, particularly within small caps, according to Citigroup strategists.

In hedge funds, Coatue Management’s fund plunged 8.3% last month, marking the latest technology-focused money manager to be whipsawed after the AI rout. Today’s Big Take looks at how a tax strategy for the rich built the world’s largest hedge fund.

The Stoxx 600 rises 0.4% as mining and technology shares lead gains, while retail and consumer products stocks are the biggest laggards.Here are the biggest movers Tuesday:

- The Stoxx 600 basic resources index is the best-performing sector in the European stocks benchmark after copper advanced to the highest in two months

- BP Plc shares are up as much as 1.7% after the British oil major reported adjusted Ebit for the second quarter that beat the average analyst estimate

- Johnson Matthey rallied as much as 5.2% in London after Jefferies reinstated the chemicals company buy, noting full-year earnings that beat the banks expectations and the Cormetech acquisition

- Travis Perkins shares surge as much as 19%, the most since April 2020, following first-half results that analysts say showed encouraging signs against a tough macro backdrop

- Zalando falls as much as 18%, the most since 2018, after the German online retailer narrowed its FY guidance alongside its second-quarter numbers

- Lufthansa shares drop as much as 11%, the most since March. The carrier reported a miss on second-quarter Ebit driven mostly by higher fuel costs

- Acciona SA shares fell as much as 10% to €208.20, the lowest level since March, after shareholder Tussen de Grachten BV sold about 1.65 million ordinary shares at €217.90 per share

- Fresenius Medical Care shares drop as much as 9.6%, the most in roughly three months, after the German company reported weaker-than-expected US dialysis volume in the second quarter

- Smith & Nephew shares drop as much as 7.9%, the most since November, after the medical-device maker reported weaker-than-expected revenue and cut its revenue growth outlook for the full year

- Adidas drops as much as 3.1%, underperforming the Stoxx 600’s consumer products and services subgroup, after UBS downgraded the stock to neutral from buy, citing “no clear catalysts to support a further re-rating”

- Metro Bank shares fall as much as 12%, the most in more than a year, as weaker fee income overshadowed improved profitability and prompted RBC to trim its earnings estimates and price target

Earlier, Asiam stocks edged lower for a second straight session, as declines in Taiwan’s TSMC and Japanese bank shares overshadowed an afternoon rebound of South Korean chipmakers. The MSCI Asia Pacific Index slipped 0.2% after earlier gains, with Mitsubishi UFJ Financial, SoftBank and Sumitomo Mitsui Financial also among the biggest decliners. Benchmarks in Taiwan, Hong Kong and India retreated. South Korea and Japan staged an afternoon comeback as key chip stocks, including SK Hynix, Samsung Electronics and Kioxia, rebounded. Chip stocks moved up after a Counterpoint Research report said rising DRAM prices are boosting the outlook for memory-chip makers. “We expect pent-up demand driven by Agentic AI and AI server CPU growth to lift prices further for conventional DRAM,” according to the report. China’s ChiNext, meanwhile, rose 5.6%, led by optical transceiver makers tracking US peers, as investors grew more optimistic about the impact of Nvidia’s rollout of its co-packaged optics platform.

In FX, yen gains are being reversed with USD/JPY approaching 158 as intervention efforts are being used as an opportunity to reload on yen shorts rather than turn the tide for the currency.

In commodities, Brent oil tumbles 3% on Bessent's comments during a CNBC interview that a Hormuz deal may come as soon as tomorrow (he is now used to emphasize Trump commentary which the market no longer believes). Lower energy prices are also boosting fixed income markets with gilts leading the declines. US yields are down 2-3bps across the curve. Also of note for bonds was the extremely poor 10-year JGB auction overnight.Precious metals have pared upside with spot gold now down 0.1%. Bitcoin sheds 0.4%.

In rates, treasuries are slightly cheaper across the curve as US day begins with futures off session lows. Price action was broadly steady overnight as oil prices stabilized, with WTI crude up around 0.4% after President Donald Trump threatened Iran with renewed air strikes. IG credit issuance is expected to remain busy this week. Treasury yields cheaper by 1bp to 2bp across the curve, following similar losses for gilts during London session with oil prices edging higher. US 10-year is around 4.695% with bunds outperforming by around 3bp in the sector. IG dollar issuance slate empty so far. Six borrowers priced almost $8 billion on Monday, with at least one borrower standing down. Issuers paid about 2bps in new issue concessions on deals that were 3.3 times covered. This week’s dealer forecasts call for a sharp pickup vs last week, with about $50 billion of new US investment-grade transactions projected

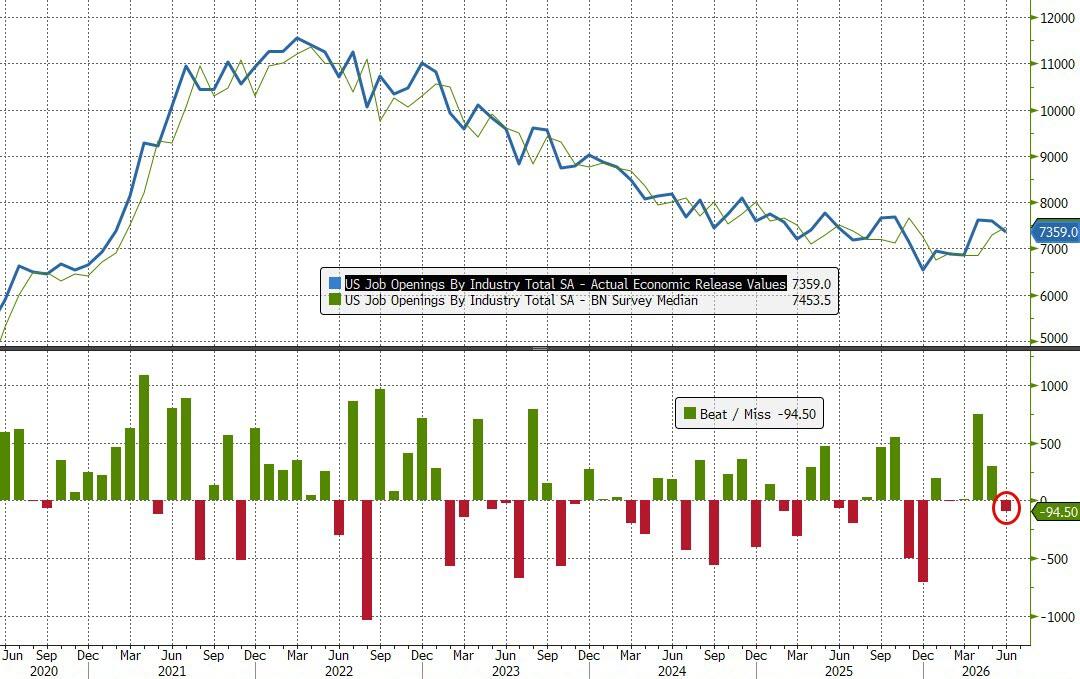

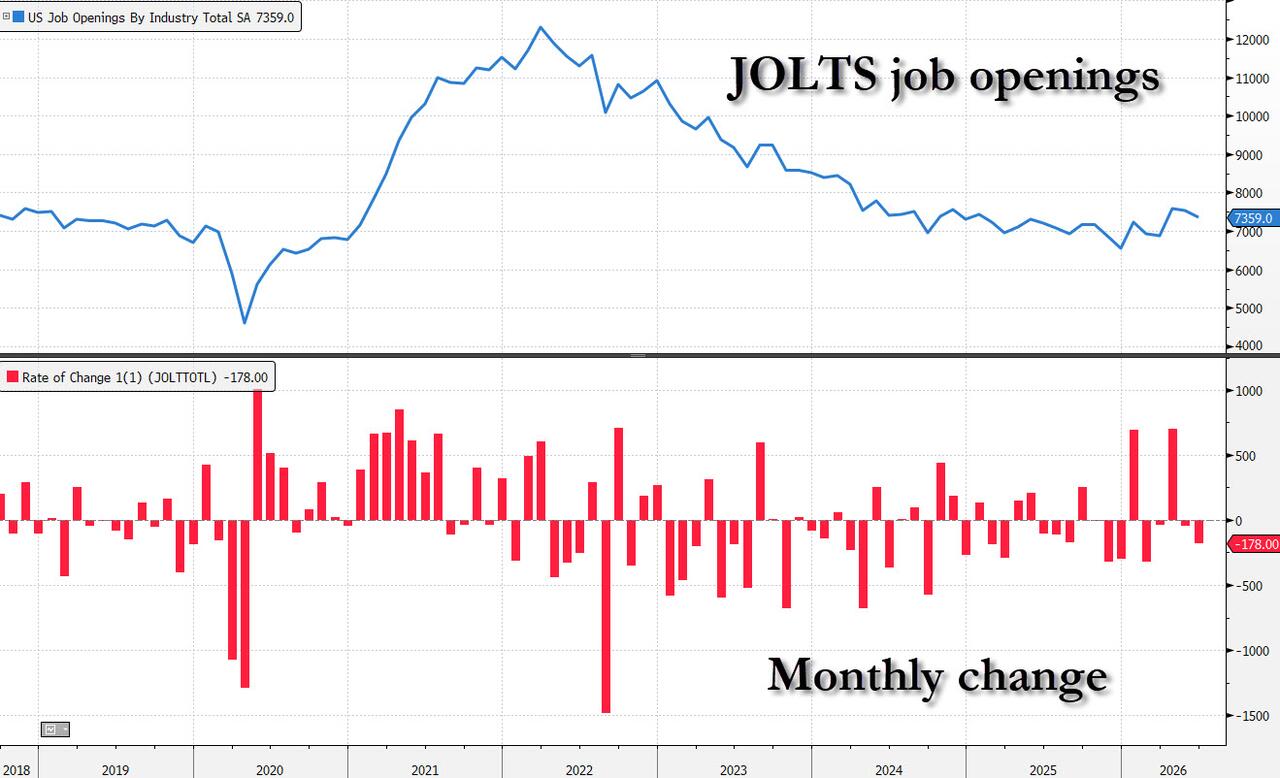

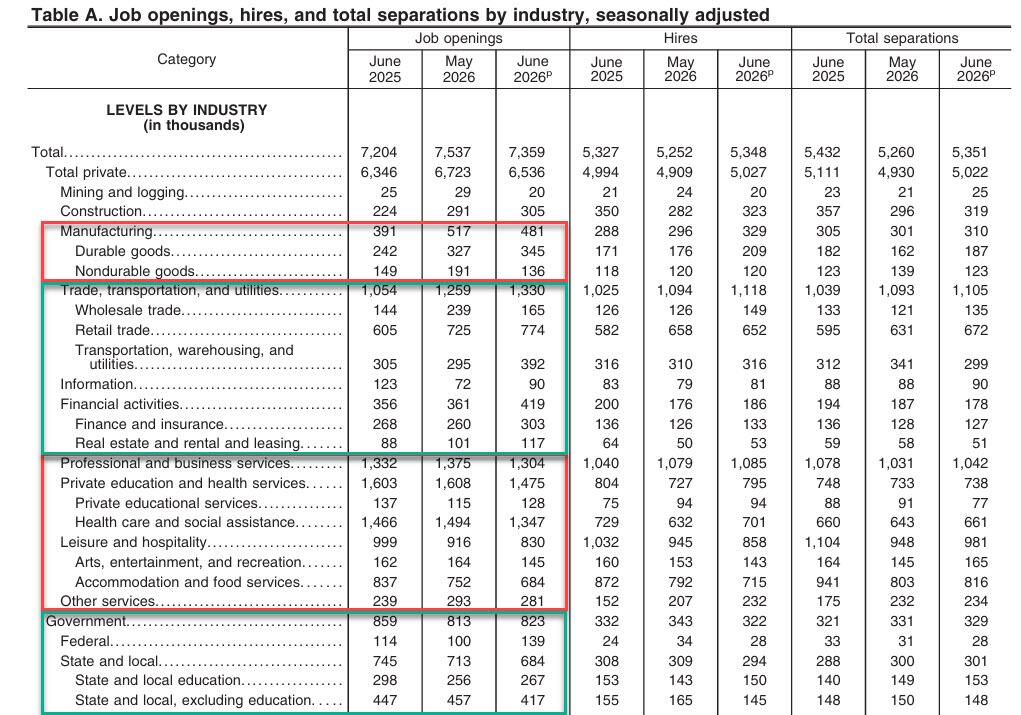

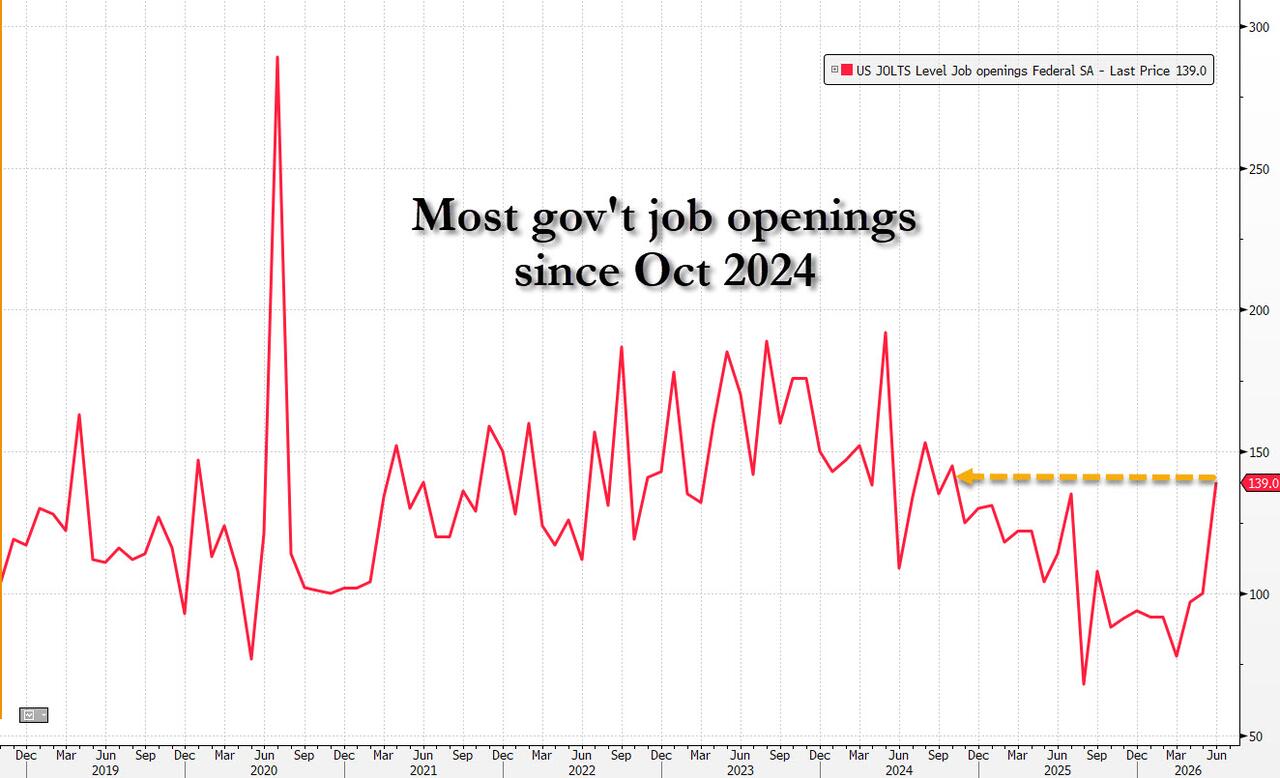

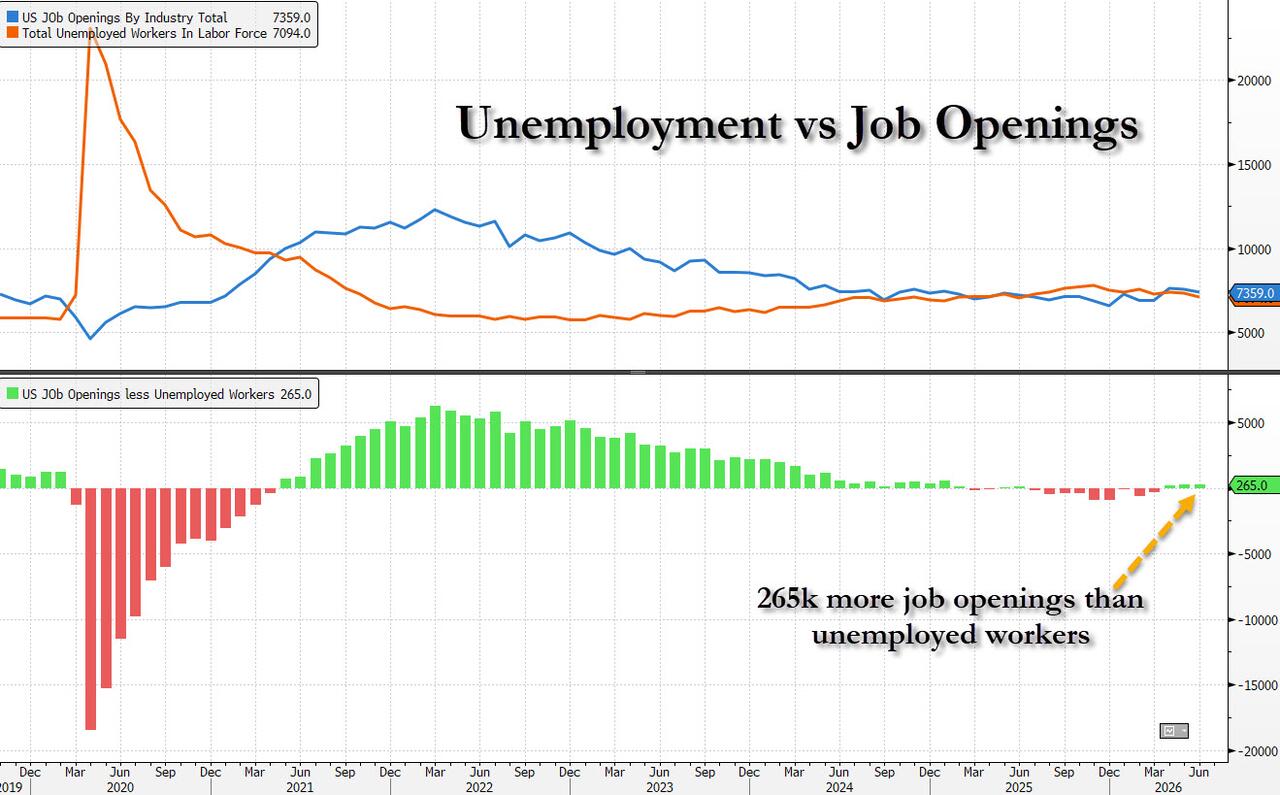

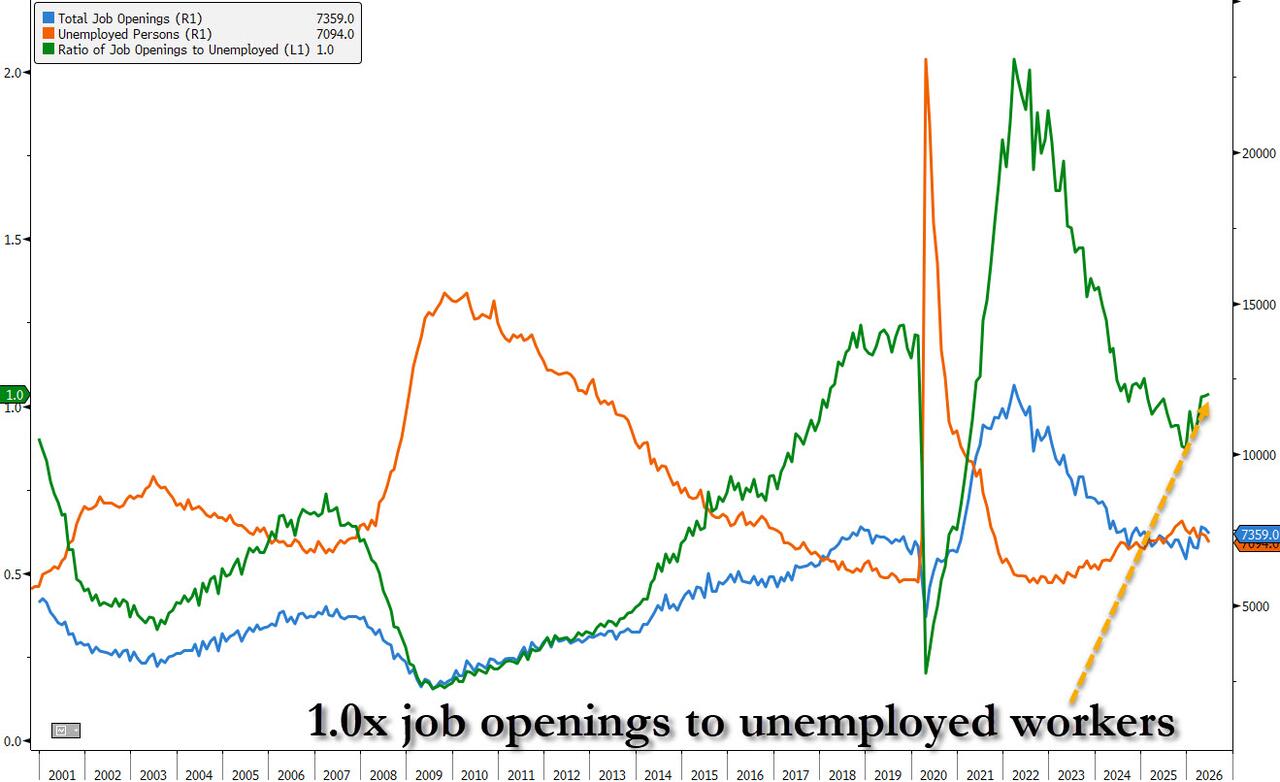

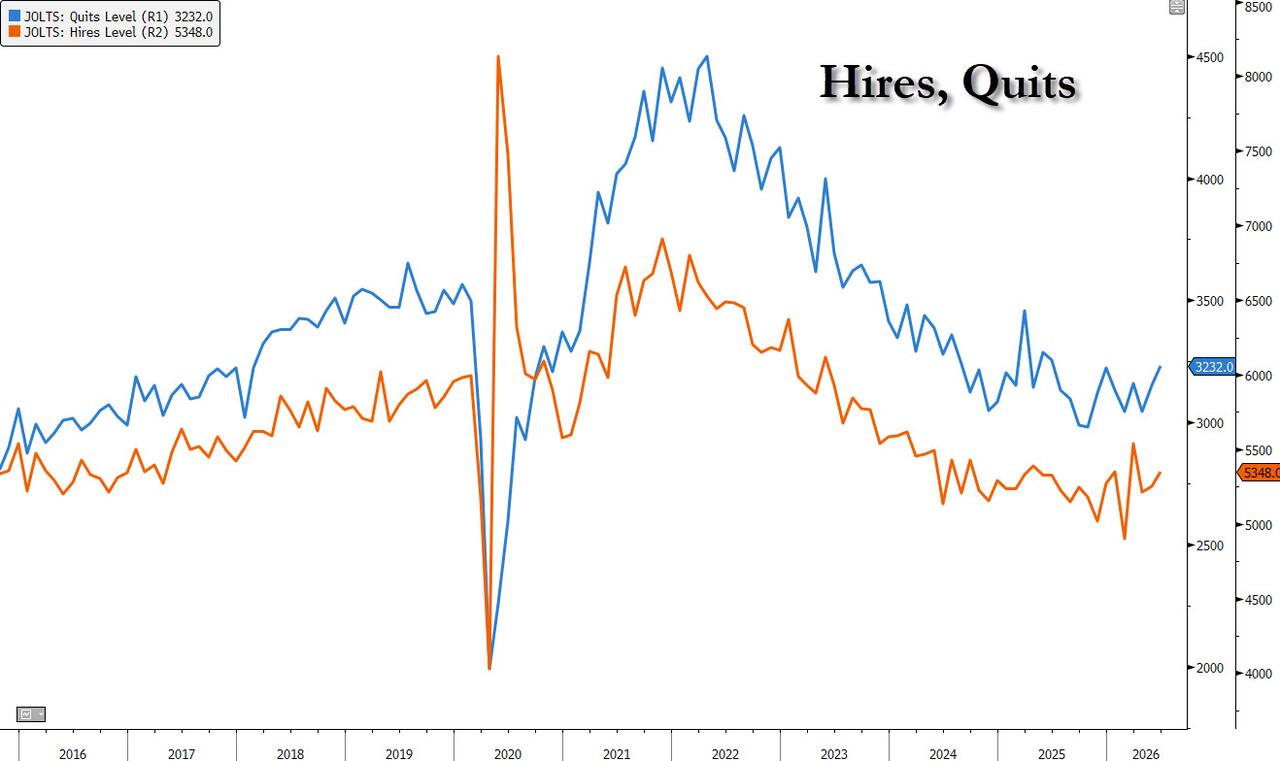

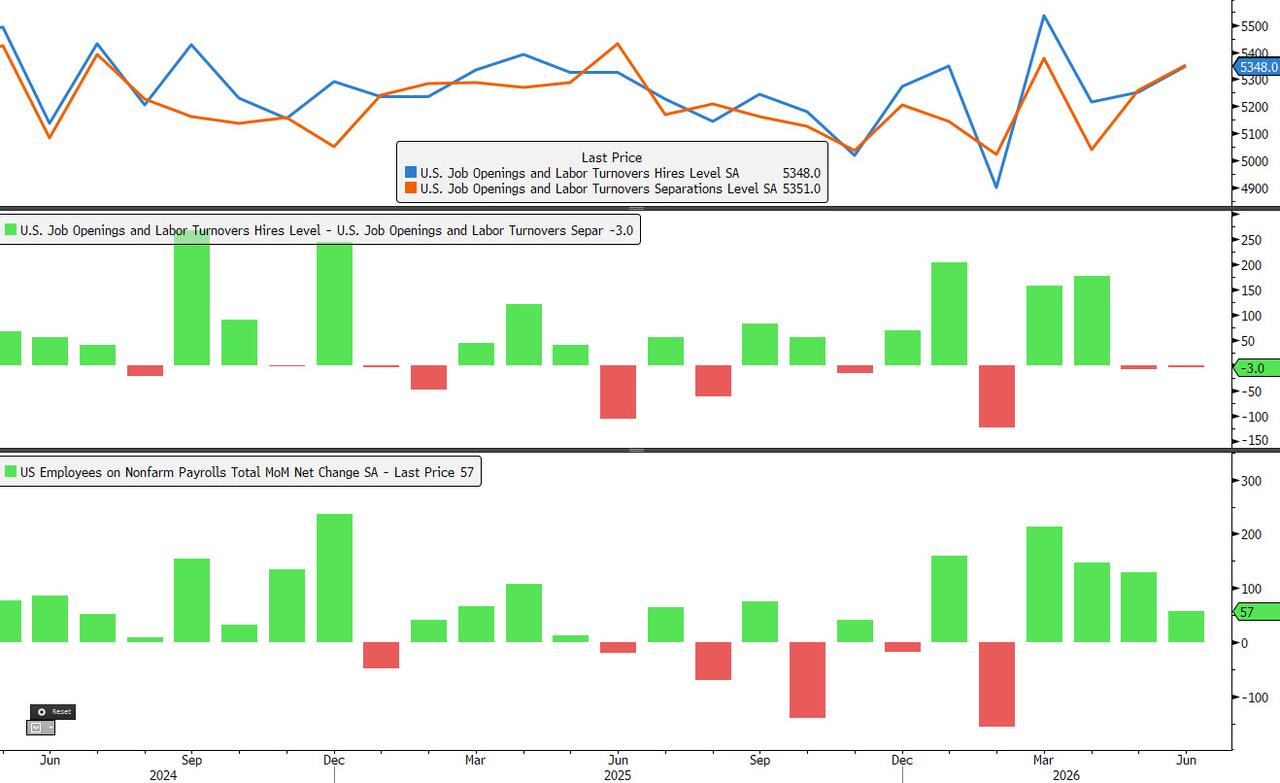

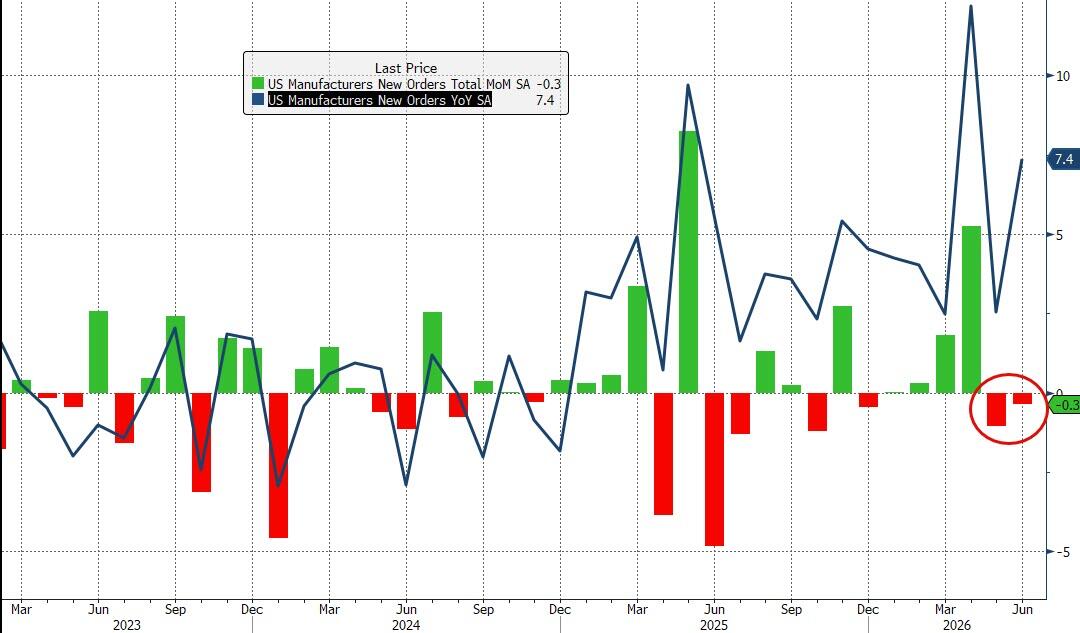

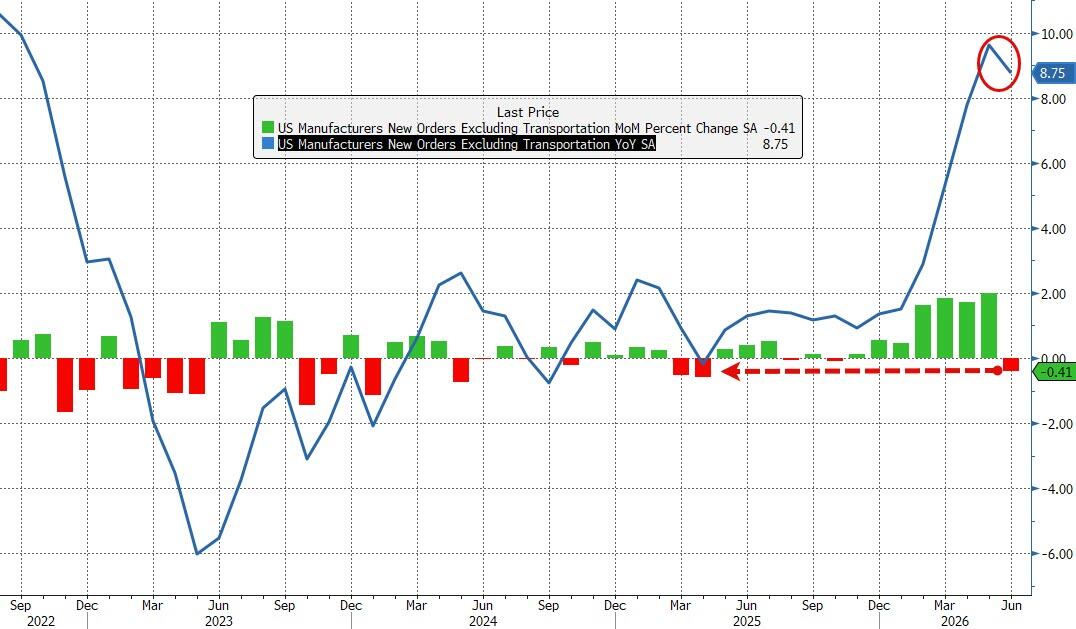

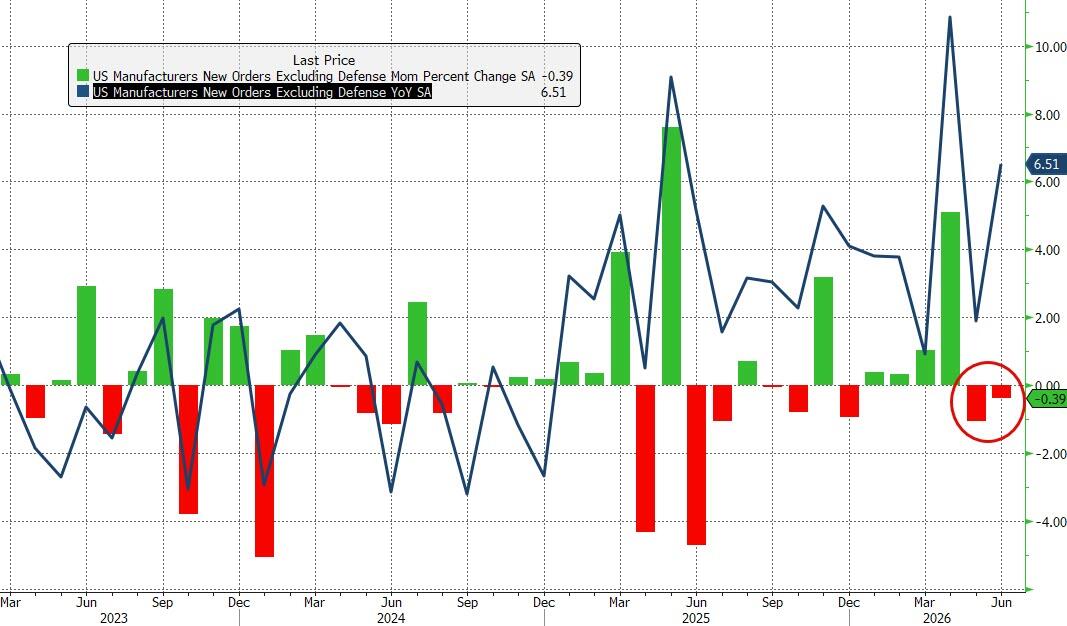

Looking at today's calendar, US economic data calendar includes June trade balance (8:30am), June factory orders with durable goods revision and June JOLTS job openings (10am). Fed speakers scheduled include Schmid at 8:15pm.

Market Snapshot

Top Overnight News

- The Trump administration is drafting a ban on U.S. imports of new models of Chinese data center components, four people familiar with the matter told Reuters, as it seeks to protect the infrastructure that undergirds the AI boom. RTRS

- Chinese officials are growing concerned about the potential for Anthropic’s Mythos and other US AI models to be used as an offensive weapon, people familiar said. BBG

- The yen continued to unwind its intervention gains and Treasuries fell. Oil rose after Donald Trump pushing Iran to reach a deal with Oman on the Strait of Hormuz as soon as today, or face devastating air strikes. BBG

- Japan Finance Minister Satsuki Katayama said the US holds the country’s economic policies in high regard, sidestepping questions on whether Washington helped strengthen the yen. BBG

- Oil prices look too low as disruptions to flows through the Strait of Hormuz are expected to persist, MLIV said. Prediction markets also show little optimism that shipments will resume anytime soon. BBG

- Michigan Democrats vote today in a high-profile Senate primary between moderate Rep. Haley Stevens and progressive Abdul El-Sayed. The winner will face Donald Trump-backed Mike Rogers. Virginia, Kansas, Missouri and Washington also hold primaries. BBG

- Todd Blanche’s nomination as attorney general seems set to advance in the Senate Judiciary Committee today after he agreed to rescind an order creating a $1.8 billion “anti-weaponization” fund, winning over holdout Republican senators. BBG

- China’s AI blitz is rapidly narrowing the gap with Silicon Valley — creating what’s been described as a “death zone” for anyone without frontier-pushing technology or market-breaking pricing. BBG

- China’s below-normal crude imports may persist if Middle East supply disruptions continue. BBG

- US Senate voted 89-4 to advance stopgap funding bill which would fund the US government through to December 11th.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed after the region failed to sustain the momentum from Wall Street, where all major indices rallied, and the Dow notched a record close amid lower oil prices and yields, following Trump's strike cancellation and touted US-Iran talks, while he even suggested they are discussing opening the Strait of Hormuz as soon as today. ASX 200 outperformed with the advances led by strength in tech and the top-weighted financial industry. Nikkei 225 wiped out early gains and dipped into negative territory with a lack of bullish catalysts overnight. KOSPI swung between gains and losses amid the choppy performances in its tech giants. Hang Seng and Shanghai Comp were mixed amid very few fresh catalysts and with China said to be growing anxious that Anthropic’s Mythos could be wielded against its economy, while better-than-expected HSBC earnings failed to inspire its shares in Hong Kong.x

Top Asian News

- Japan's Economy Minister Kiuchi said the pass-through of rising costs on goods prices has been limited so far and June overall CPI shows price rises remain moderate Y/Y. The minister added that the Government shares with BoJ the forecast that consumer inflation will accelerate in the latter half of this year and slow thereafter. Hopes the BoJ conducts monetary policy appropriately to stably and sustainably achieve its 2% inflation target and that the BoJ closely communicates with the government in guiding policy.

European bourses continue to climb, with the FTSE MIB the outperformer. Not much in terms of a broader driver; plenty of corporate earnings were on the docket this morning, while another day of no strikes between the US and Iran brightens hopes of a sustained end to the conflict. Sectors are mixed. Basic Resources top the sector pile, followed by Tech and Industrial Goods & Services. Retail is the sector laggard, with Travel & Leisure and Consumer Products & Services rounding out the underperformers. Weighing on Retail is the earnings from Zalando (-15.5%), in which Q2 revenue missed estimates and narrowed its FY26 adj. EBIT guidance.

Top European News

- Bayer (+3.4%), Q2 revenue and Adj. EBITDA beat estimates and confirms FY26 view;

- Continental (-1.5%), FY26 revenue guidance missed estimates and highlighted that raw material costs are set to substantially increase;

- Lufthansa (-9.5%), cuts FY26 adj. EBIT guidance and notes heightened levels of forecasting uncertainty;

- HSBC (-1.0%), Q2 PBT and Net beat estimates and announces a USD 1bln share buyback programme;

- BP (+1.0%), Q2 revenue beat and announces its intention to sell Archaea.

FX

- DXY sees relatively quiet trade thus far, trading on either side of the 100 mark in a narrow 99.93-100.06 range at the time of writing, deriving little support from the firmer oil prices, albeit WTI sees shallower gains than Brent (see Commodities update). Analysts at ING meanwhile posit “Unless ADP tomorrow and, more importantly, payrolls on Friday point to a clearly weakening jobs market … we do not expect the dollar to fall much further in the near term. Uncertainty over the next stage of US-Iran negotiations may also help limit downside pressure on oil prices.” DXY has topped yesterday’s 100.02 high but remains well within Friday’s 100.46 high and above the 100 DMA (99.73).

- EUR and GBP are also uneventful amid a lack of macro and domestic drivers this morning. EUR/USD found support at 1.1500 on Monday after slipping from a 1.1559 high, shy of its 100 DMA, which today resides at 1.1563 (vs 1.1568 yesterday). GBP/USD is tucked in a 1.3419-1.3439 range, well within yesterday’s 1,3418-1.3506 band but still above a small cluster of DMAs, with the 100 DMA at 1.3399 and 200 DMA at 1.3396, providing some reinforcement around the 1.3400 round figure.

- JPY is once again interesting, with USD/JPY continuing its mild recovery from post-intervention lows, but remains beneath the 158.00 level, with very few fresh catalysts and a lack of tier-1 data overnight and in the European morning. USD/JPY resides in a current 157.14-157.80 range at the time of writing, just shy of yesterday’s 157.93 high and the 200 DMA at 157.95.

- Antipodeans are mixed, with AUD gaining and standing out across G10 peers, with strength seen overnight following stronger-than-expected Household Spending data, whilst gains in gold and copper could also be lending support. AUD/USD and NZD/USD remain within yesterday’s ranges, whilst AUD/NZD has gained and resides closer to the top end of a 1.1918-1..1969 range, above yesterday’s 1.1961 high.

- BoJ data showed an expected shortfall of JPY 3.38tln in money market conditions (exp. shortfall between JPY 2.32-2.6tln). Data suggest that Japan may not have intervened in the FX market on Monday.

Fixed Income

- A mostly contained European morning for fixed income, after pressure seen in APAC trade in JGBs and to extent other peers after a particularly poor 10yr Japanese auction.

- As mentioned, the main point thus far was the dismal Japanese 10yr auction, featuring a lower b/c but pertinently a sizable price tail. Results sparked pressure in JGBs of near 70 ticks, to a 126.36 low. Since, the benchmark has recovered for the most part, but remains lower by just over 10 ticks and as such underperforms.

- For reference, no move to a BoJ research paper on the JGB market, where the headline points echoed commentary from Ueda in last week’s press conference.

- Bunds firmer by a handful of ticks, saw some modest pressure overnight alongside the JGB move (as did USTs), but only fleeting with the fundamentals and dynamics a very different story. The day ahead for Europe is light, and thus the benchmark will likely conform to the lead from USTs around US events, and geopolitical updates more generally. At the midpoint of a relatively narrow 124.68-92 band.

- USTs look to a few data points, alongside commentary from Fed’s Paulson. But, action is more likely to be dictated by any geopolitical developments, after President Trump’s relatively constructive commentary on the conversations with the US; however, CBS reported that only the ongoing mediator-led talks are planned. As with Bunds, flat in a c. five tick range, holding just above the 108-10+ low.

- Gilts conform, opened with gains of a few ticks, and has since slipped to a 87.04 base, lower by around 25 ticks. Pressure is a function of the modest strength seen in energy (despite it coming off highs in the early morning). No reaction was seen following the 2032 tap.

- The UK sells GBP 4.25bln 4.625% 2032 Gilt: b/c 3.34x, average yield 4.613%, tail 0.2bps.

- Japan sells JPY 1.98tln 10yr JGBs, b/c 2.56x (prev. 3.13x), average yield 2.840% (prev. 2.729%), Tail in price 0.46 vs prev. 0.20.

Commodities

- In geopolitics, President Trump said talks with Iran were ongoing and suggested the Strait of Hormuz could reopen by Tuesday, although US officials clarified that no new negotiations were planned beyond existing mediator-led discussions. Tensions remain high, with reports of Iranian drone attacks on a US base in Kuwait and vessels near the Strait, including a cargo ship struck off Oman. Iran warned that continued efforts to break the blockade could put US forces and vessels at serious risk, while Iranian leaders reportedly believe they can withstand US pressure and raise costs through regional proxies and threats to shipping. Meanwhile, Iran’s foreign minister is expected to visit Islamabad.

- WTI Sep'26 and Brent Oct'26 are firmer amid geopolitics but to varying magnitudes, with the former currently +2.2% intraday and the latter +3%. The difference in gains could potentially be a function of President Trump yesterday criticising major oil companies, saying they were making excessive profits and urging them to lower retail fuel prices. The mechanism being: if US refiners are forced to lower fuel prices while crude costs remain elevated, refining margins shrink, prompting them to reduce crude processing to balance books and, in turn, lowering demand for WTI crude. Nonetheless, WTI trades around the top of a USD 79.62-82.28/bbl range vs yesterday’s USD 78.43-81.30/bbl range. Brent resides within a USD 83.80-86.33/bbl range vs Monday’s 81.55-84.66/bbl range. Dutch TTF is back above EUR 59/MWh, having traded under EUR 58/MWh

- Metals are firmer across the board as DXY remains contained despite the gains across crude, with precious and base metals benefiting from the current stability in oil prices under July highs as President Trump continues to tout diplomacy with Iran, and with no further escalations seen thus far this European morning. Spot gold remains under yesterday’s USD 4,019-4,079/oz range within a current USD 4,043-4,073/oz range. Base metals also benefit across the board, with 3M LME copper back above USD 14k/t in the current 13,871.88- 14,049.30/t range at the time of writing.

- Saudi Aramco - Q2 adj. net income +33% Y/Y to USD 33.4bln (exp. 31.1bln). Benchmark Brent crude averaged approximately USD 97/bbl during the quarter as the closure of the Strait of Hormuz, driven by the US-Iran conflict, caused the largest oil supply disruption on record, with Aramco redirecting the bulk of its exports via the East-West Pipeline to the Red Sea. Elevated refined-product prices provided an additional margin tailwind, sustaining returns even as Brent temporarily retreated below USD 75/bbl following an interim ceasefire agreement. It flagged mounting risk to Red Sea export volumes as Houthi militants threaten attacks on tankers using that route.

- Saudi Aramco CEO said global oil inventories could take about 18 months to recover following supply disruptions.

- Oman crude for October delivery priced at USD 83.51/bbl, according to state news.

- Goldman Sachs expects Brent crude to trade within an USD 80–90/bbl range until a new US-Iran agreement is confirmed or attacks escalate significantly.

Trade/Tariffs

- Japan and Mexico agreed to strengthen energy cooperation, with Japan and Mexico aiming to hold first high-level economic dialogue this fiscal year, according to Kyodo

Central Banks

- BoK Minutes stated that one member said timing and pace of any further rate hikes should be determined with primary emphasis on inflation.

Geopolitics: Middle East

- Iranian President said Tehran would defend its borders but does not seek to expand the war, according to state media.

- Iranian Supreme Leader adviser Rezaei said if the blockade continues, US vessels and forces will face serious risks and casualties.

- Arab media reported explosions and fires occurred at US bases in Kuwait, according to Fars News Agency. This was later confirmed by i24, in which the IRGC attacked a US base in Kuwait using 3 drones, according to a source.

- UKMTO received a report of an incident 20 nautical miles northeast of Oman's Al Khasab, in which a cargo vessel broadcasted that they had been hit by an unknown projectile. More recently, a dry bulk vessel was reportedly hit by a projectile near the Strait of Hormuz, according to a maritime security source.

Geopolitics: Ukraine

- Ukraine, on August 4th, struck a major Russian oil refinery 800km from the border, attacking the Syzran oil refinery (170k BPD). A major fire broke out on the premises, RBC Ukraine reported.

Geopolitics: Other

- North Korea slammed US-led naval exercise and vowed to respond with deterrence of a new level, according to Yonhap.

US Event Calendar

- 8:30 am: Jun Trade Balance, est. -73b, prior -77.6b

- 10:00 am: Jun Factory Orders, est. 0.2%, prior -1.3%

- 10:00 am: Jun JOLTS Job Openings, est. 7453.5k, prior 7594k

- 10:00 am: Jun F Durable Goods Orders, est. 0.3%, prior 0.3%

- 10:00 am: Jun F Durables Ex Transportation, est. 0.6%, prior 0.6%

DB's Jim Reid concludes the overnight wrap

After several weeks of military exchanges and fears of a renewed energy shock, markets have started August welcoming the late weekend comments from President Trump that fresh talks with Iran would begin after he cancelled plans for what he described as a major attack. That optimism was reinforced by suggestions from Iranian officials that negotiations between Iran and Oman over “temporary” shipping arrangements through the Strait of Hormuz are progressing, offering a potential path towards improved oil flows. Even Trump’s post as Europe went home that “Iranian Leadership is unbelievably duplicitous”, which came following Iranian comments that they were not currently negotiating with the US, didn’t spoil things. Trump also said that his latest offer of talks was a “last chance” for Iran but that didn’t derail improved market optimism on Hormuz shipping amid the renewed focus on diplomacy.

So for one day at least markets enjoyed something they haven't had much of this summer: falling oil prices, lower inflation expectations, stronger growth data, declining bond yields, and rising equities all at the same time. A nice way to start August even if you feel it could go either way very quickly.

The biggest move was in energy yesterday. Brent crude fell -4.73% to $83.77/bbl (adjusting for the benchmark month change), whilst WTI dropped -5.11% to $80.34/bbl. This morning, they are edging back +1.42% and +1.12% higher respectively. European natural gas futures also declined -1.80% yesterday.

The reaction in inflation markets was also strong. The US 1yr inflation swap fell -5.5bps to 1.86%, its lowest since September 2024, whilst the Eurozone 1yr inflation swap declined -3.3bps to 2.36%. So markets are dismantling a chunk of the near-term inflation premium that had built up through July as the conflict intensified. Real yields moved lower too, with the US 30yr falling -3.6bps to 3.00%.

Government bonds were immediate beneficiaries. The 10yr Treasury yield fell -5.8bps to 4.68%, whilst 10yr bund yields (-5.5bps) declined to 3.15%. Gilts outperformed both, with the UK 10yr yield down -9.6bps to 4.95%, making them one of the strongest-performing major developed market assets on the day and their best day since May 20. 10yr BTP yields (-8.6bps) weren’t far behind, also registering their largest daily decline since late May.

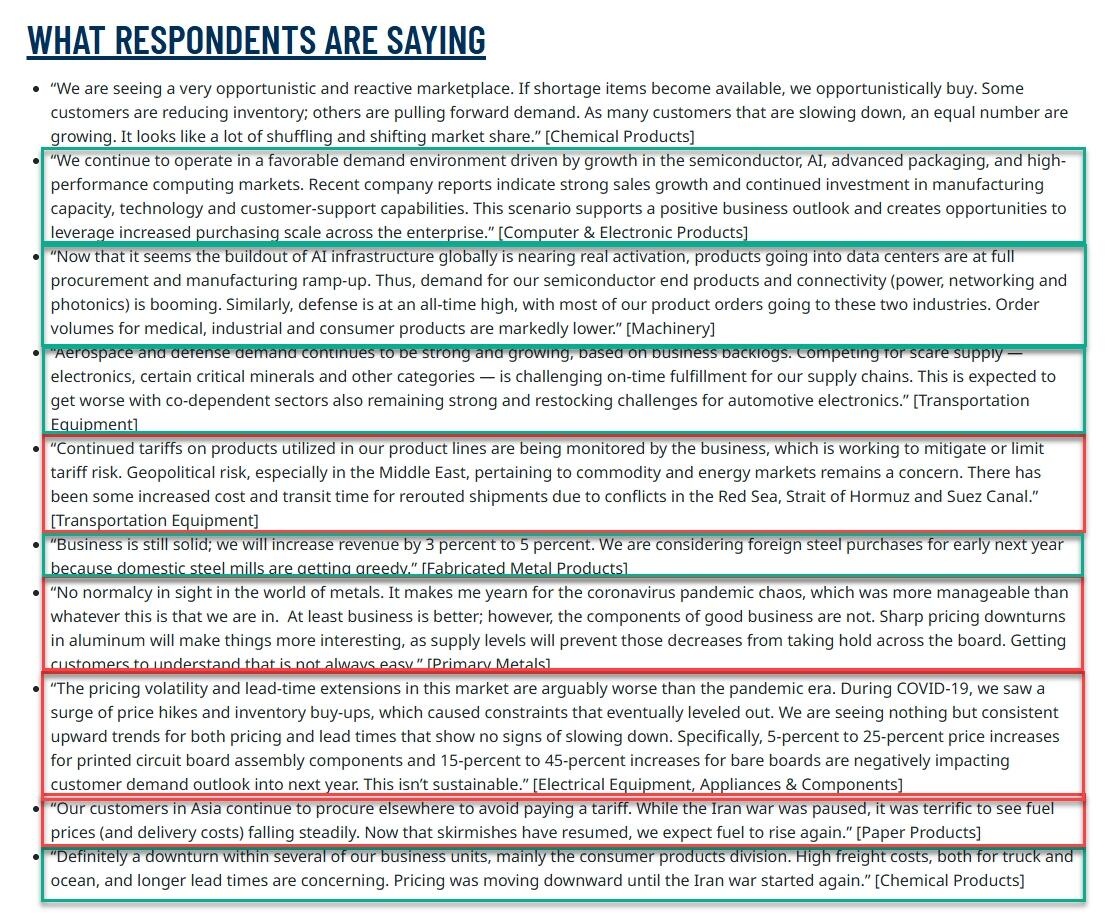

However, unlike several of the recent oil-driven rallies, yesterday's move wasn't occurring against a backdrop of weakening growth. In fact the opposite was true. The US ISM manufacturing survey rose to 55.6 in July, its highest reading since May 2022 and comfortably above the 53.9 expectation. The employment component (52.8 vs 50.0 expected) moved into expansion territory for the first time since September 2023, whilst new orders was strong (56.7 and in-line). Not even prices paid remaining at an elevated 71.1 (roughly in line with expectations, but easing back from 73.0) dampened the mood. The associated commentary suggested the booming activity was linked to semiconductors, AI, defence, and high-performance computing. In other data, the Fed’s latest quarterly Senior Loan Officer Survey painted a picture of buoyant lending to corporates, even if there were some pockets of softness on the household side.

That combination of lower oil and stronger growth proved a very supportive backdrop for equities. The S&P 500 rose +1.48% to close just -0.12% below its record high from June 2. The Nasdaq Composite gained +2.13% and the Dow added +1.32%. The standout performer was the Magnificent Seven, which rallied +3.56%, posting its largest daily gain since March 31, with all bar Apple (-1.78%) up around +3% or more. Moreover, coupled with the tech rebound late last week, the Mag-7 recorded its best 3-day run (+8.98%) since May 2025, when the US and China agreed on their trade truce. Interestingly that enthusiasm didn't extend as much into the semiconductor space, with the Philly Semi Index (+1.05%) underperforming the broader market after losing -20.6% in July. In Europe, the Stoxx 600 rose +0.45%, the DAX gained +1.45% and the CAC 40 advanced +1.22%.

This morning, focus continues to be on the yen story, which stabilised after its early Monday spike that we wrote about yesterday. The yen ended yesterday’s session up +0.19% to 157.10 against the USD, having traded below 155.50 early on Monday. And this morning it is -0.27% lower trading at 157.63 against the dollar, still far from the 163 level before the intervention last Thursday.

Asian equity markets are mostly trading lower overnight with the KOSPI (-0.96%) again the weakest performer, despite recovering some of its early losses, while the Nikkei (-0.33%) and Hang Seng (-0.49%) are also on the softer side. In contrast, mainland Chinese equities are outperforming their regional counterparts, supported by a rebound in technology stocks following yesterday’s selloff. At the time of writing, both the CSI 300 (+0.94%) and the Shanghai Composite (+0.18%) are trading higher. Meanwhile, Australia’s S&P/ASX 200 (+1.29%) is posting strong gains, driven by a rally in lithium miners and strength in commodity-linked shares, which is more than offsetting weakness in other sectors. S&P 500 (+0.22%) and Nasdaq (+0.38%) futures are up along with the Stoxx (+0.34%) equivalent.

Early morning data showed that South Korea's consumer inflation eased to a three-month low, with prices rising 2.8% year-over-year in July, down from 3.2% in June and 3.0% expected. Core was a tenth higher than expected at 2.6% YoY.

Away from the macro picture, one of the more eye-catching corporate stories came from healthcare after reports that AstraZeneca (-8.96% yesterday) has explored a potential acquisition of Bristol-Myers Squibb (+0.24%), which would rank as the largest pharmaceutical deal ever completed. Defence stocks also remained in focus after Northrop Grumman secured agreements worth up to $3bn related to missile interceptor production, a reminder that even if diplomacy is making a comeback, the geopolitical backdrop remains anything but normal.

To the day ahead now, the main US data will be the JOLTS report, followed by June trade balance and factory orders. We’ll also get France’s June budget balance YTD, Italy June retail sales. Earnings include SpaceX, AMD, HSBC, Booking, Pfizer.

Tyler Durden

Tue, 08/04/2026 - 08:30

Dozens of empty Waymos clogged a small street in an Atlanta neighborhood, preventing residents from leaving or returning to their homes

Dozens of empty Waymos clogged a small street in an Atlanta neighborhood, preventing residents from leaving or returning to their homes

Damage in Moscow region, via Telegram

Damage in Moscow region, via Telegram

Bitdeer Tydal campus

Bitdeer Tydal campus

A farmer washes lettuce in a backyard urban farm in Los Angeles, on March 25, 2020. Robyn Beck/AFP via Getty Images

A farmer washes lettuce in a backyard urban farm in Los Angeles, on March 25, 2020. Robyn Beck/AFP via Getty Images

Recent comments