"Reaching A Climax": Hedge Funds Turn Most Bearish On Yen Since 2007, As Former FX Czar Sees 20% Undervaluation

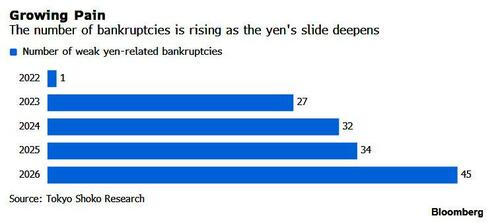

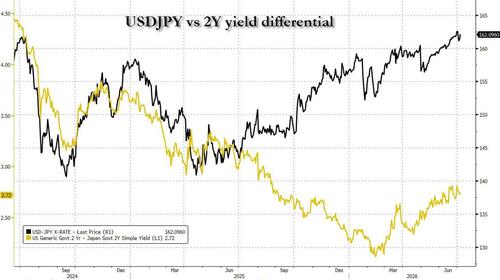

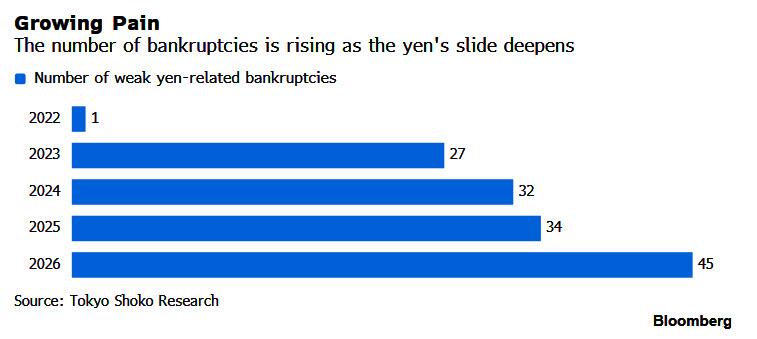

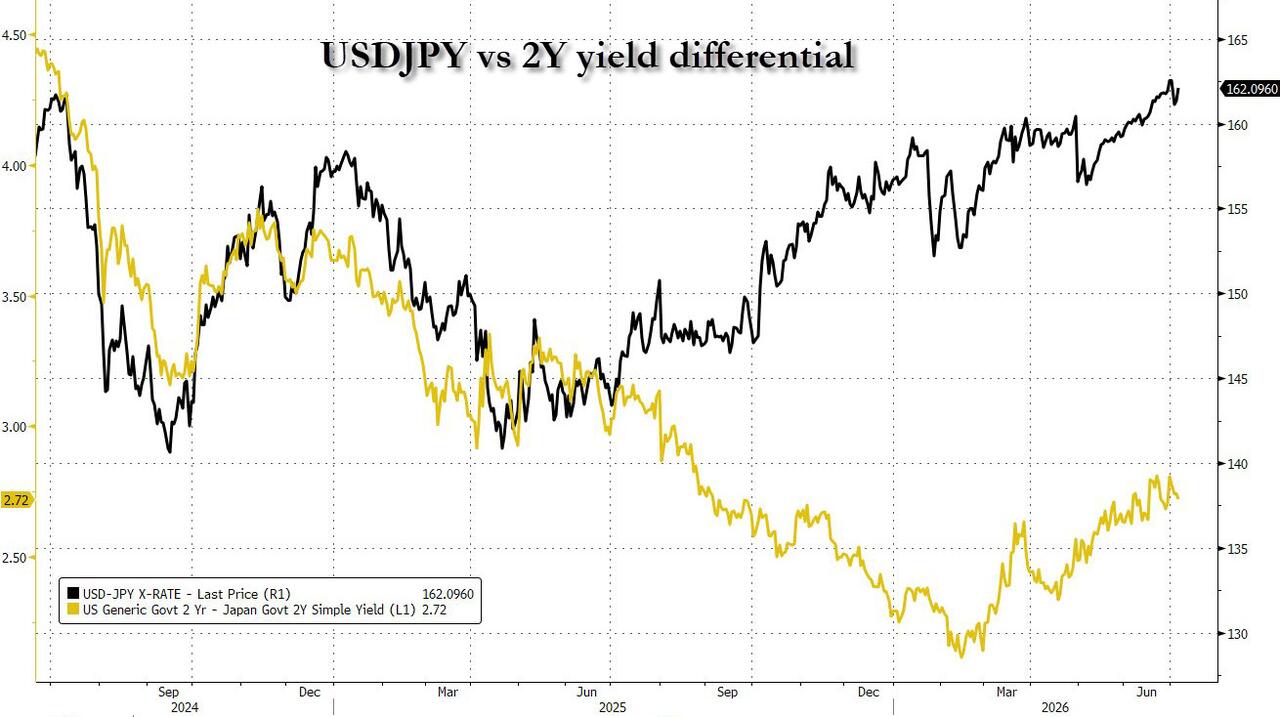

For much of the past year, when the USDJPY disconnected - initially playfully and then terminally - from 2Y yield differentials, FX traders have been asking when and how will this gaping divergence finally converge. Alas, that answer remains elusive still, even as the collapse in the yen has pushed the currency to a generational low, and become an increasingly political topic leading to a surge in Japanese bankruptcies, and a relentless battering of what little is left of Japan's middle class.

Source: Japan Bankruptcies Surge To All-Time High As A Result Of Plunging Yen

Source: Japan Bankruptcies Surge To All-Time High As A Result Of Plunging Yen

And yet, despite the yen's push into what until just two months ago were seen as unthinkable lows by the BOJ no less (which promptly spent $50BN to prop up the currency this April when it touched 161), the fact that the Japanese central bank allowed the yen to resume its descent through the July 4th holiday despite the unprecedented divergence from fundamentals, where it is now about 25 big figures too cheap...

... has encouraged hedge funds to keep piling on yen shorts seemingly encouraged by a theory proposed by Mizuho’s Jordan Rochester that the USDJPY has become negatively correlated to yield differentials, essentially representing the EM-ification of Japan (as Bloomberg reminds us, veteran currency traders will recall that we have seen this sort of thing before, via the “Japan premium” applied to short rates and swap yields around 1997-98 as the country’s banking sector was in the process of imploding).

Another source of pressure on smaller businesses may be foreign-exchange hedging, including the use of so-called reverse knockout options, according to Yuji Saito, executive adviser at SBI FXTrade. Such products are widely sold by regional banks as structured hedging products, particularly to small and regional importers seeking to minimize upfront option premiums.

Once the exchange rate reaches a preset knockout level, the option expires and the hedge ceases to provide protection. Companies needing dollars must then either purchase them in the spot market, enter into a new hedge - often at less favorable levels - or leave themselves exposed to further currency moves.

“The weaker the yen gets, the more importers roll into increasingly risky option structures,” Saito said. “Once the knockout level is breached, they are forced to buy dollars in the spot market, creating a negative spiral that puts even more downward pressure on the yen."

Analysts estimate that remaining reverse knockout levels are clustered between 163 and 170 yen per dollar, territory that many firms didn’t think the currency would reach as intervention from the central bank would likely be forthcoming due to the adverse economic impact of such unprecedented currency collapse.

“The number of knockouts could increase if the yen weakens further,” said Hiroyuki Machida, director of Japan FX and commodities sales at Australia & New Zealand Banking Group. “The situation is becoming significant for companies that are unable to pass on higher costs.”

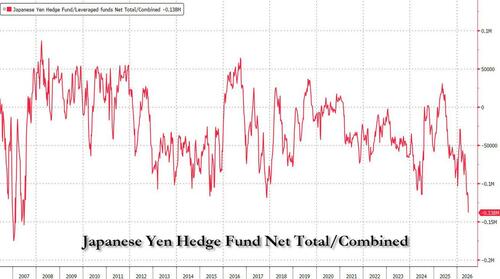

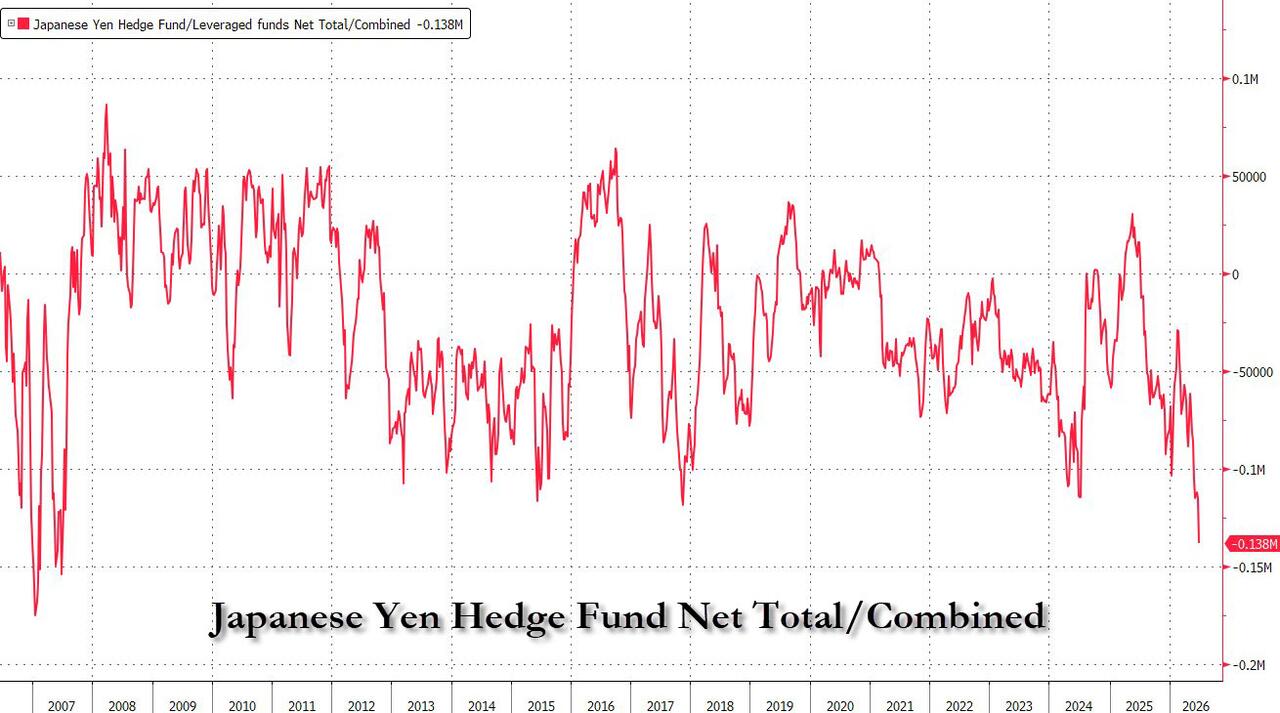

And yet, despite the clear adversely consequences to both Japan's economy and society, the perception that Japan's new PM Takaichi doesn't want higher rates or a stronger yen, is leading to ever greater pile ups inside the short yen trade, which was clearly visible today when the latest CFTC Commitment of Traders data showed that hedge funds are most bearish on the yen since 2007, just before the housing bubble burst.

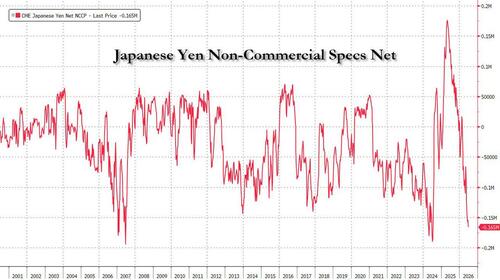

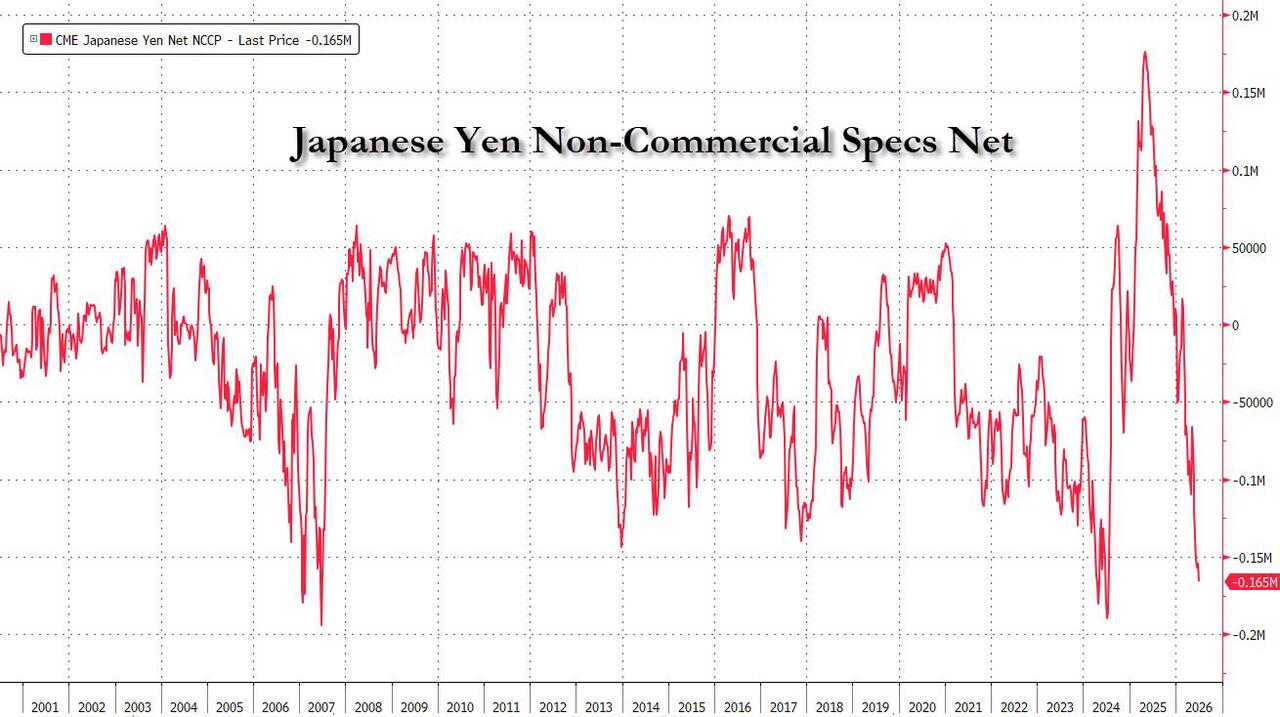

An even more remarkable CFTC chart is the one showing non-commercial spec net positioning in the yen, which over the past two years has completed one of the most dramatic swings in history, from record bearish, to record bullish, and back to record bearish again!

The cherry on top was the overnight reco by the Goldman Sachs FX team which capitulated on its bullish yen bias, but instead now sees the currency dropping to a new 40 year low of 165 next. This is how the bank explained it:

With USD/JPY near its weakest level in 40 years, intervention risk is elevated. But it can only have a short-lived impact if macro fundamentals continue to push in the other direction (as we’ve already seen this year). We think the trend higher in USD/JPY should extend, barring a negative US growth shock or a BoJ pivot towards more aggressive policy tightening—neither of which appears likely over the coming year. Therefore, we are revising up our USD/JPY forecast path to 162, 163, 165 (vs. 160, 158, 155 previously). Without rising recession risk or a pivot towards aggressive BoJ tightening, we think the trend higher in USD/JPY should extend and continue to favor it as a funder for high-carry EM expressions

So with the bulls capitulating and everyone already bearishly positioning, what happens next? Usually precisely the opposite of what everyone expects, since there is nobody left to add to the bearish side.

Which brings us to the rare contrarian view: pushing back against those speculating that the currency might continue its slide - which as we showed above is pretty much everyone - Japan's former top FX official said the yen should be as much as 20% stronger than it is, or around 130 per dollar

“This isn’t about fundamentals anymore — it’s about how people’s expectations have shifted,” Tatsuo Yamasaki, who served as vice finance minister for international affairs a little over a decade ago, said in an interview Monday with Bloomberg. “But we are reaching a climax.”

Former vice financial minister of international affairs Tatsuo Yamasaki

Former vice financial minister of international affairs Tatsuo Yamasaki

“I wouldn’t be surprised if the yen were around 130 to the dollar. That’s honestly how it looks to me,” he told Bloomberg, an outcome that would lead to the liquidation of countless FX trading desks.

Yet, as noted, he remains a lone hawk in a world full of yen bears. The slide along with a relatively tepid response from Japanese authorities has some speculating the rout may have room to run. Jesper Koll, expert director at Monex Group, and Calvin Yeoh at Blue Edge Advisors consider 200 and beyond within the realm of possibility should the Bank of Japan fall further behind in tightening policy.

Yamasaki, now a senior professor at the International University of Health and Welfare, doesn’t see that happening. The BOJ is likely to continue raising rates, while the odds of another Federal Reserve rate hike remain roughly 50%, making a further widening in the Japan-US rate gap far from certain, he said.

“As far as interest rate differentials, yes, the BOJ’s next move is definitely a rate hike, maybe followed by several rate hikes, while the Fed’s next move is still uncertain,” he said. Even if the Fed hikes, it will likely be a one-off move, he said.

“They’ve already issued the warning, and anyone who is still holding short yen positions knows that they risk being punished by an intervention - that is, being forced to unwind those positions,” Yamasaki said. “The finance ministry has already moved beyond the warning stage, and the authorities have demonstrated they’re willing to act.”

Yamasaki also downplayed concerns that Prime Minister Sanae Takaichi’s latest economic and fiscal policies point to a worsening of Japan’s fiscal position. Last month, Takaichi unveiled a growth plan featuring a 14-year, ¥370 trillion investment program combining private- and public-sector outlays, while projecting that Japan’s debt-to-GDP ratio will continue to decline even as the government commits ¥10 trillion in annual spending. The plan appears designed to pair an ambitious investment agenda with assurances of fiscal discipline.

Yamasaki said the market will have a much clearer picture of Takaichi’s fiscal and monetary policy stance later this year as the government compiles its budget for next year. “At that point, I think the market will recognize that there wasn’t a fundamental case for such a weak yen in the first place,” he said.

Until then, however, Yamasaki said authorities should be prepared for a prolonged battle with speculators.

“If you’re facing a long fight, spending tens of trillions of yen every time the market moves isn’t the answer, because the currency will simply move back again,” he said. “The priority should be to prevent the yen from weakening much further. Once people come to believe that the fundamentals actually point to a stronger yen, I think the currency will appreciate on its own.”

Yamasaki added that “stealth intervention” — small-scale operations that avoid drawing immediate market attention — could be an effective way to keep speculators off balance. Having said that, Tokyo isn’t likely to get any help from its counterparts. He said it would be politically difficult for the US to join such efforts while maintaining its standard opposition to currency manipulation by other nations.

“Basically it’s not going to happen,” he said.

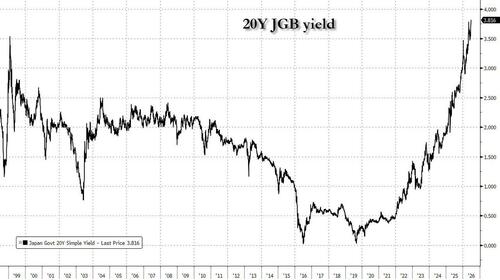

There is another reason why the BOJ will have no choice but to tighten soon: the 20Y JGB yield just hit a new record high overnight, rising 4bps to a new all time high 3.816%. It was 0 in 2019.

Ironically, Yamasaki headed the Finance Ministry’s foreign-exchange market division during a period when Japan was attempting to prevent the yen from doing the opposite, namely strengthening. Authorities spent about ¥35 trillion on intervention between 2003 and 2004 in that campaign.

Even with Washington unlikely to jump into the market, Yamasaki doesn’t expect any pushback if Japan intervenes.

“I don’t recall a time when the US was on board with Japan’s intervention intentions as much as it is now,” he said, reiterating comments made recently by current forex chief Atsushi Mimura. In a Bloomberg interview last week, Mimura highlighted what he described as “closer-than-ever” communication between Tokyo and Washington on currency matters.

More recently, when the yen was foundering in September 2022, Yamasaki warned of intervention risk. Two days later authorities intervened to support the yen.

Tyler Durden

Mon, 07/06/2026 - 19:40

Micron Technology Inc.’s factory in Higashihiroshima, Hiroshima Prefecture, JapanSource: Micron Technology Inc.

Micron Technology Inc.’s factory in Higashihiroshima, Hiroshima Prefecture, JapanSource: Micron Technology Inc. Source:

Source:

Former vice financial minister of international affairs Tatsuo Yamasaki

Former vice financial minister of international affairs Tatsuo Yamasaki

People visit the Smithsonian Museum of American History on the National Mall in Washington, on April 3, 2019. Pablo Martinez Monsivais/AP Photo

People visit the Smithsonian Museum of American History on the National Mall in Washington, on April 3, 2019. Pablo Martinez Monsivais/AP Photo

Ranchers work to evacuate cattle as the Gifford Fire burns nearby in Los Padres National Forest, Calif., on Aug. 4, 2025. AP Photo/Noah Berger

Ranchers work to evacuate cattle as the Gifford Fire burns nearby in Los Padres National Forest, Calif., on Aug. 4, 2025. AP Photo/Noah Berger

CoreSite’s NY3 data center is located in Secaucus and offers more than 138,000 square feet of capacity.CoreSite

CoreSite’s NY3 data center is located in Secaucus and offers more than 138,000 square feet of capacity.CoreSite Deepak Kumar, 31, of Fresno, California, was arrested June 27 after Greenfield police recovered a shipment of tungsten oxide powder valued at about $2.9 million. Police said Kumar faces theft-related charges in Pennsylvania. Source: Greenfield Police Department

Deepak Kumar, 31, of Fresno, California, was arrested June 27 after Greenfield police recovered a shipment of tungsten oxide powder valued at about $2.9 million. Police said Kumar faces theft-related charges in Pennsylvania. Source: Greenfield Police Department

Recent comments