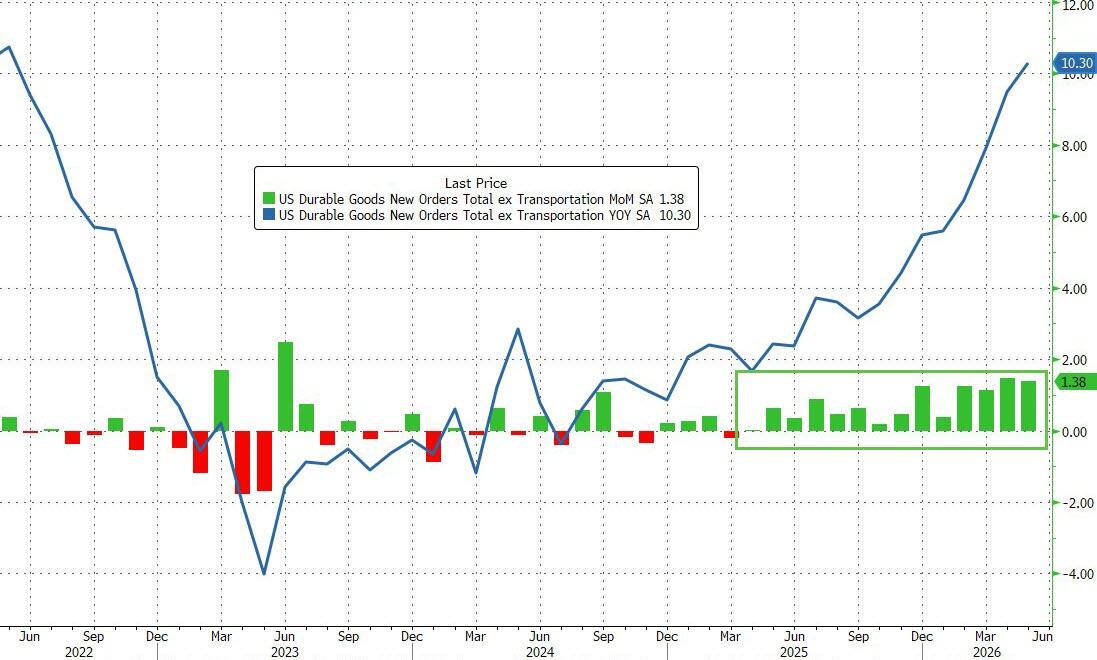

World's Largest Data Center Project On Verge Of Collapse After Blackstone Unexpectedly Pulls Out

Up until now, when it comes to real estate, Blackstone was best known in recent years for dumping many of its trophy office properties - which in the aftermath of work from home never recovered their projected cash flow potential - at a huge discount. Now, it may be pulling a page from its old, pre-Lehman playbook by calling the top in yet another commercial real estate segment: data centers.

Two days ago we reported that Blackstone was selling its stakes in a trio of data centers across Northern Virginia for $3.5 billion, cashing out of part of a bet it made less than three years ago. According to Bloomberg, Digital Realty Trust would pay $1.2 billion of cash and offer $2.3 billion of its shares (which the PE giant has largely cashed in by now) to Blackstone funds; in exchange, the data center company will acquire Blackstone’s 80% interest in two 96-megawatt data centers in Manassas, Virginia, and a 50% interest in a 96-megawatt center in nearby Sterling.

We said that "the question is why did Blackstone decide to pull the cord now, just as fresh doubts are creeping whether the Mag 7s will continue funding the AI expansion with virtually unlimited capex."

Two days later we have an answer.

The digital ink is barely dry on its Virginia data center sales, and we learn that Blackstone’s QTS (QTS Realty Trust) is again quietly fading its AI exposure by walking away from plans to build its portion (which at this point is the only portion left after its partner already pulled out days ago) of a 2,100-acre data center campus in Virginia - also known as Prince William Digital Gateway which would house as many as 37 data-center buildings - handing a win to residents who fought for years to topple the project.

QTS's proposed facility at 9400 Godwin Drive in Manassas

QTS's proposed facility at 9400 Godwin Drive in Manassas

The data center developer had planned to transform more than 800 acres in Northern Virginia’s Prince William County, a project that would have spanned 22 million square feet, making it the largest data center campus in the world. Located on the edge of an historic Civil War battlefield and on what used to be land protected from development, the project ignited strong pushback from homeowners and has been stalled by lawsuits.

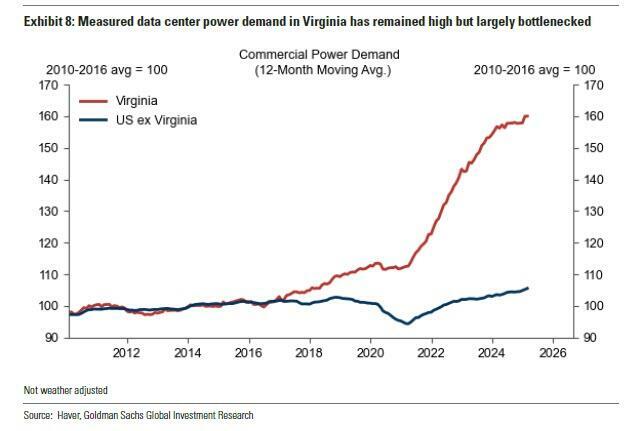

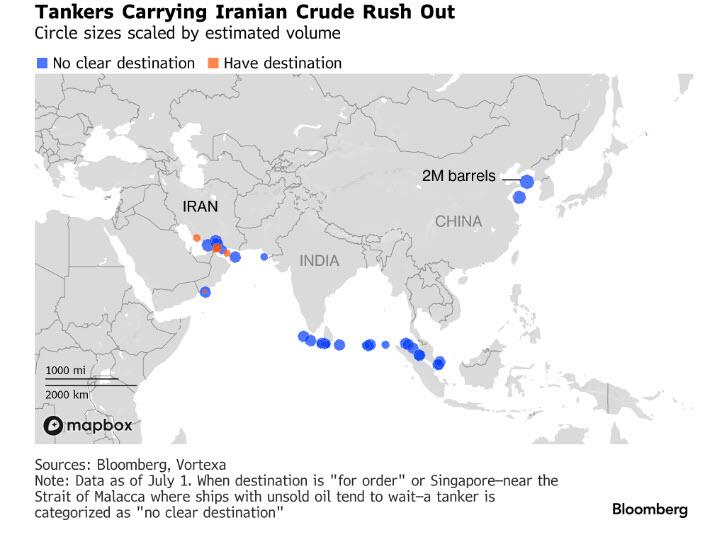

As part of Wall Street’s broader push into data centers, investment has poured into Northern Virginia, which is considered the country’s largest data center market, and is better known as "Data Center Alley"

But in a strategic U-turn, in recent days QTS executives decided that it isn’t worth pressing forward in court, the Bloomberg sources said. The firm’s attorneys plan to inform the court of their decision as soon as this week, the people said, asking not to be named discussing non-public information.

QTS’s rapid growth has made it a poster child of how private equity has fueled the data center industry’s breakneck expansion. Those ambitions are colliding with public anxiety over strains to electricity grids and home prices from AI data centers.

The retreat may be the final blow to Virginia’s “Digital Gateway” project, a mega site roughly twice the size of New York’s Central Park with city-sized power needs. The initiative was supposed to bring in some $100 billion in spending and create one of the world’s largest technology corridors. Not any more.

The project had sparked contentious, drawn-out public hearings. A clerical blunder related to a key zoning meeting created setbacks for developers. Already, Brookfield-backed Compass Datacenters, which was supposed to build on more than 800 acres at the site, had pulled out in May.

The U-turns by both firms, Bloomberg writes, amount to one of the most dramatic retreats by developers from a data center project.

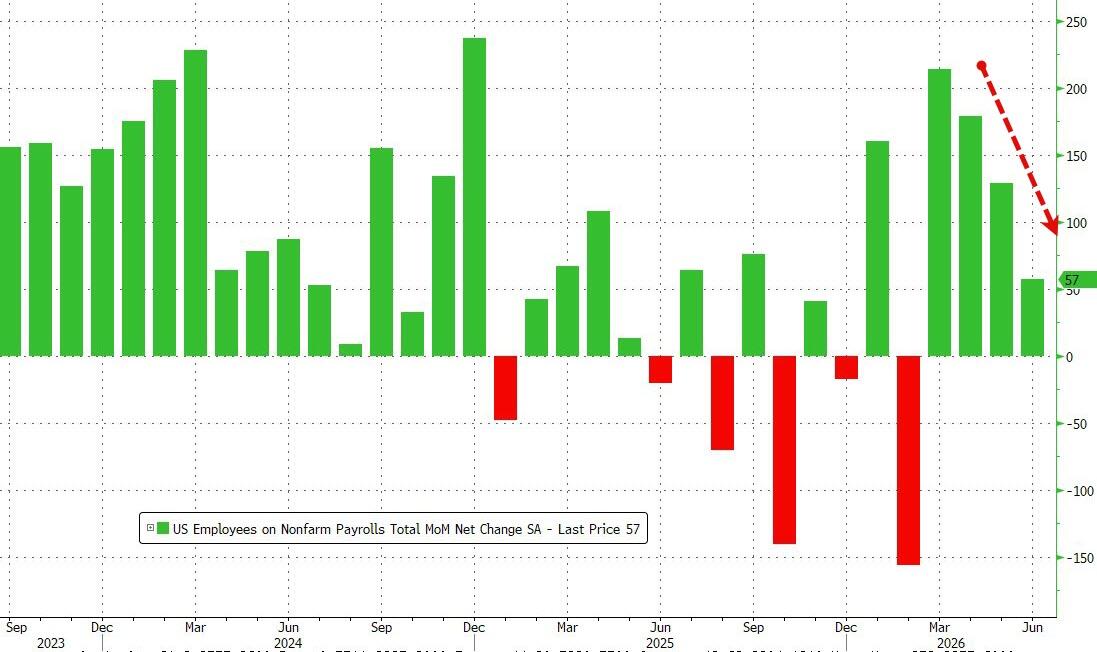

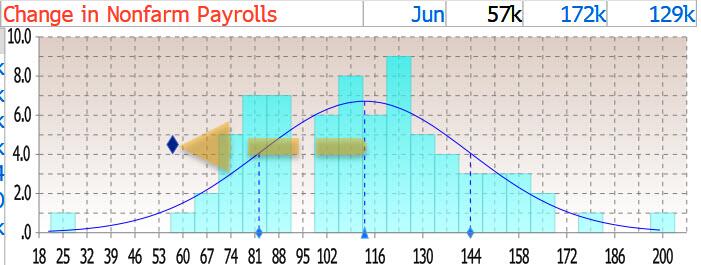

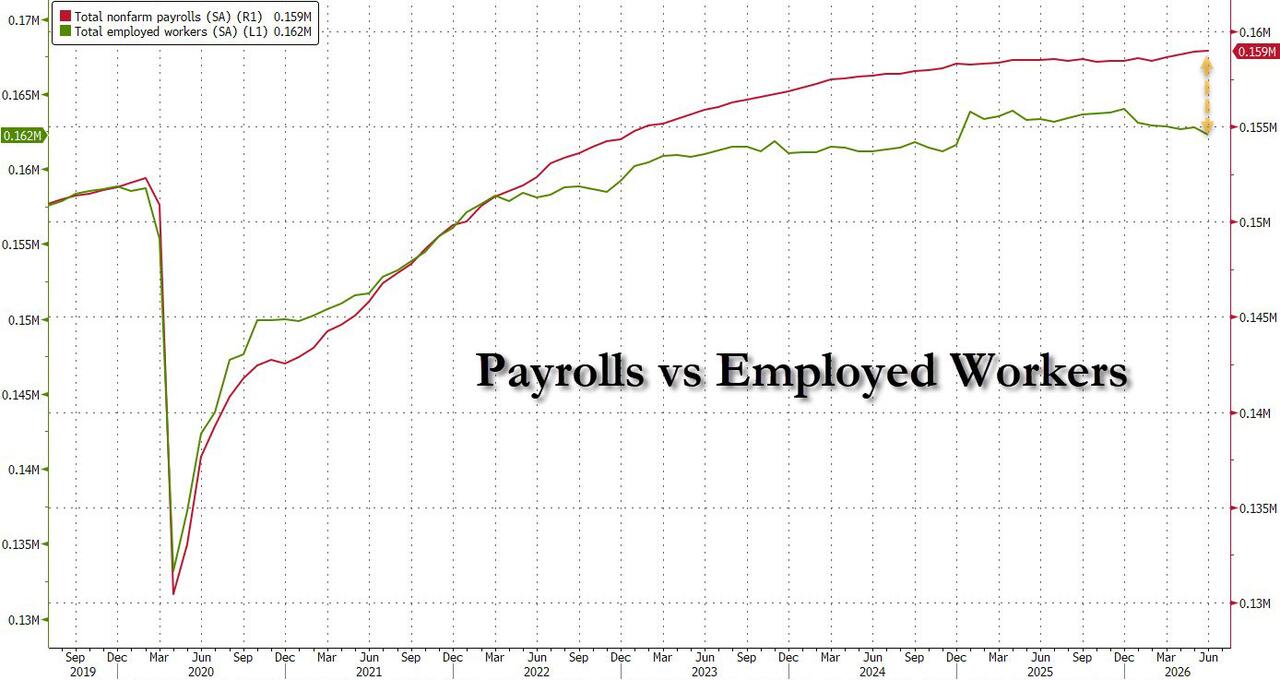

It’s a reminder of how tech firms’ race for the computing infrastructure to support AI advances is increasingly facing the same bottlenecks, from power shortages to supply crunches, we have been warning about for the past two years and which Citadel Securities warned about just yesterday.

Organized opposition is mounting, forcing firms and developers to be more deliberate about where they choose to build. This is precisely what we warned one year ago would happen as more grassroots organizations pushed back against the relentless data center rollout. At least we haven't gotten to the arson stage (yet).

between exploding electricity bills and lack of jobs for grads, a new luddite revolution is coming - they will be burning down data centers within a year

— zerohedge (@zerohedge) August 25, 2025

To account for the costs of such build outs, Virginia recently passed a budget with an energy consumption tax on data centers, and more states are threatening moratoriums on new development. Data centers - and how their costs and benefits are shared - are now emerging a major swing issue in the lead up to the US midterm elections. These hurdles raise questions for investors over whether the AI build out can keep going at this pace.

For community organizers and residents that spent the last five years opposing the Digital Gateway, QTS’s pullout will now validate a playbook that involved pressure campaigns on local politicians and legal attacks. It will also unleash even more powerful blowback nationwide against these unwanted developments.

As Bloomberg recalls, hundreds of proponents and critics showed up at a 27-hour zoning hearing in 2023 to lobby authorities on the project. After county officials narrowly voted to approve the conversion of agricultural and semi-rural land for data centers, community organizers and residents pursued lawsuits.

The outcome of the meeting - and whether the county properly advertised the event - was at the center of legal challenges. The lawsuits hinged on one detail: The first two newspaper notices publicizing the hearing weren’t separated by at least six days, as state and local codes required at that time. While it is unclear if Blackstone agents had tried to "grease" the zoning board's palms to quietly fast-track the data center, in the end the outcome was catastrophic to the builders.

In March, Virginia courts upheld an earlier ruling that the zoning approvals were invalid because the public notices for the meeting fell short of rules.

Opponents of the Digital Gateway data center project rallies at Manassas Battlefield Park.

Opponents of the Digital Gateway data center project rallies at Manassas Battlefield Park.

“While we still believe this project offered significant benefits for the region and our neighbors, recent legal actions and compounding regulatory hurdles have effectively closed a viable path forward,” Compass Datacenters President AJ Byers said in a statement following the ruling.

After Compass bailed on the project, that left QTS as the lone developer. It was the only party that petitioned for an appeal of the case in Virginia’s Supreme Court.

Originally, the firm’s executives were concerned about the prospect of setting a legal precedent on the back of an administrative oversight. After Compass’s retreat, QTS lost a partner who would share the costs of upgrading various utilities needed for the massive developments, said one of the people familiar with the matter. QTS decided it was not worth proceeding with the project.

Blackstone, which acquired QTS in 2021, is a major financier of data centers, with a portfolio of more than $150 billion of such assets around the world.

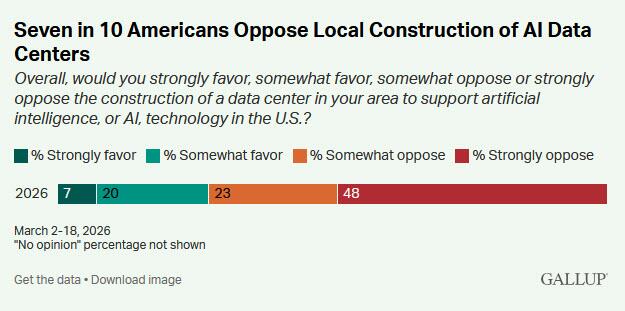

The increasingly bitter political and grassroots pushback against new data center construction explains why Blackstone has been getting cold feet just as the AI bubble is peaking, first selling existing data centers and now walking away from upcoming projects. A recent Gallup poll found that 7 in 10 Americans oppose constructing data centers for artificial intelligence in their local area, including nearly half, 48%, who are strongly opposed. Barely a quarter favor these projects, with 7% strongly in favor.

Half of opponents mention data centers’ excessive use of resources, including 18% each mentioning their use of water and energy. Sixteen percent mention a related environmental concern of pollution, including noise pollution and air and water pollution.

About one in five opponents are concerned with the impact on local quality of life, including increased population, increased traffic and preferring that the land be used for other purposes. A similar share mention potentially negative economic consequences, including higher utility bills, cost-of-living increases, and the cost of building the data centers (which could involve the use of taxpayer funds).

Most of the remaining opposition stems from general or specific concerns about artificial intelligence.

Blackstone, which manages more than $1.3 trillion, bills itself as the largest global provider of data centers, and also owns some of the utilities that power them. It acquired QTS in 2021 and bought Australian computing provider AirTrunk in 2024. In May, the firm held an initial public offering for Blackstone Digital Infrastructure Trust Inc., its data center acquisition vehicle, which aims to buy already built and leased properties benefiting from the artificial intelligence boom.

And now that the protest movement knows how to push back against uninvited Wall Street occupants, thanks to the BlackStone capitulation, expect an exponential increase in legal (and other) attempts to hinder the rollout of data centers across the US, assuring that the AI supercycle, which is already years behind schedule with just half of the data centers meant to be built in progress and on time, will expect to see an avalanche of delays and cancellations assuring that the return on debt-funded capex will be even less as eventual launch dates gradually move ever further into the unknown future.

Tyler Durden Thu, 07/02/2026 - 17:20 The cooling towers for units 4 (L) and 3 (R) are seen at Plant Vogtle, operated by Georgia Power Co., in east Georgia's Burke County near Waynesboro, Ga., on May 29, 2024. Arvin Temkar/Atlanta Journal-Constitution via AP, File

The cooling towers for units 4 (L) and 3 (R) are seen at Plant Vogtle, operated by Georgia Power Co., in east Georgia's Burke County near Waynesboro, Ga., on May 29, 2024. Arvin Temkar/Atlanta Journal-Constitution via AP, File Energy Secretary Chris Wright testifies before the Senate Armed Services Committee hearing on the budget request for the Energy Department on Capitol Hill in Washington on May 13, 2026. Manuel Balce Ceneta, File/AP Photo

Energy Secretary Chris Wright testifies before the Senate Armed Services Committee hearing on the budget request for the Energy Department on Capitol Hill in Washington on May 13, 2026. Manuel Balce Ceneta, File/AP Photo

Former Director of the U.S. Central Intelligence Agency (CIA) John Brennan testifies before the House Permanent Select Committee on Intelligence on Capitol Hill in Washington on May 23, 2017. Alex Wong/Getty Images

Former Director of the U.S. Central Intelligence Agency (CIA) John Brennan testifies before the House Permanent Select Committee on Intelligence on Capitol Hill in Washington on May 23, 2017. Alex Wong/Getty Images

A Glock handgun and two magazines in a file photograph. Rich Pedroncelli/AP Photo

A Glock handgun and two magazines in a file photograph. Rich Pedroncelli/AP Photo California Gov. Gavin Newsom announces new gun legislation in Sacramento on Feb. 1, 2023. Courtesy of Office of Governor Gavin Newsom

California Gov. Gavin Newsom announces new gun legislation in Sacramento on Feb. 1, 2023. Courtesy of Office of Governor Gavin Newsom

Zyn nicotine cases and pouches on a table in New York City on Jan. 29, 2024. Michael M. Santiago/Getty Images

Zyn nicotine cases and pouches on a table in New York City on Jan. 29, 2024. Michael M. Santiago/Getty Images

The Food and Drug Administration in White Oak, Md., on June 5, 2023. Madalina Vasiliu/The Epoch Times

The Food and Drug Administration in White Oak, Md., on June 5, 2023. Madalina Vasiliu/The Epoch Times Tou Lue Vang told the pardons board that he had regrets about abusing a 10-year-old girl multiple times (DHS photo)

Tou Lue Vang told the pardons board that he had regrets about abusing a 10-year-old girl multiple times (DHS photo) Minnesota Gov Tim Walz was part of a unanimous decision that will prevent a child-molester's deportation

Minnesota Gov Tim Walz was part of a unanimous decision that will prevent a child-molester's deportation

via AFP

via AFP

Recent comments