translations on the coordinate plane worksheet pdf

Coordinate plane translation worksheets, often in PDF format, are vital tools for mastering geometric shifts. These resources, like those from CKMath, reinforce concepts effectively.

Practice with these worksheets builds skills in graphing and algebraically representing movements, preparing students for more complex transformations and geometric challenges.

What are Coordinate Plane Translations?Coordinate plane translations represent a fundamental geometric transformation where a shape or point is moved, without rotating or flipping, to a new location. Worksheet PDFs focusing on translations demonstrate this shift by consistently adding or subtracting values from the x and y coordinates of each point.

Essentially, every point in a figure moves the same distance in the same direction. These worksheets, such as those offered by CKMath, often require students to identify this consistent change – the translation rule – and apply it to graph new images. This builds a strong foundation for understanding more complex transformations.

Why Use Worksheets for Practice?Translation worksheets, readily available as PDF downloads, provide targeted practice crucial for solidifying understanding. They move beyond conceptual knowledge, demanding students actively apply the translation rule. Resources like CKMath’s bundles offer in-class exercises, homework assignments, and reinforcement after instruction.

Worksheets allow for individualized practice and immediate feedback, often including answer keys for self-assessment. They also build procedural fluency – the ability to accurately and efficiently execute translation steps. Furthermore, PDF format ensures accessibility and easy printing for convenient learning.

Understanding TranslationsCoordinate plane translations involve sliding a shape without changing its size or orientation, often practiced using PDF worksheets for skill development.

Definition of TranslationA translation, in the context of the coordinate plane, represents a rigid transformation where every point of a shape is moved the same distance in the same direction. This movement doesn’t alter the shape’s size or orientation; it simply relocates it. Worksheet exercises, frequently available as PDF downloads, often present pre-image shapes and ask students to apply a given translation rule.

These PDF resources help students visualize and understand how coordinates change during a translation. The core idea is a consistent shift – for example, moving every point three units to the right and two units up. Mastering this concept is foundational for understanding more complex transformations.

Translation vs. Other Transformations (Reflection, Rotation, Dilation)While all are coordinate plane transformations, translation differs significantly from reflection, rotation, and dilation. PDF worksheets often include exercises designed to differentiate these. Reflections create mirror images, rotations turn shapes around a point, and dilations change the size of a figure.

Translation, uniquely, preserves both size and orientation – it’s a pure shift. Students using these PDF resources learn to identify transformations by observing changes in coordinates. For instance, a flipped coordinate indicates a reflection, while a scaled coordinate suggests dilation. Recognizing these distinctions is key to mastering coordinate geometry.

The Rule of Translation: (x, y) → (x + a, y + b)The core of understanding translations lies in the rule: (x, y) → (x + a, y + b). PDF worksheets heavily emphasize applying this rule. ‘a’ represents the horizontal shift, and ‘b’ the vertical shift. Positive values move the shape right and up, respectively, while negative values shift left and down.

Students practice using this rule to determine new coordinates after a translation. Many worksheets present pre-translated shapes and ask students to deduce ‘a’ and ‘b’. Mastering this algebraic representation is crucial for solving more complex problems involving multiple transformations.

PDF worksheets vary from basic practice to complex scenarios, including multiple transformations and engaging activities like emoji-based translations for diverse learning styles.

Basic Translation WorksheetsBasic translation worksheets, frequently available as PDF downloads, focus on the fundamental concept of shifting figures on the coordinate plane. These worksheets typically present pre-image shapes and ask students to apply a given translation rule – often in the form (x, y) → (x + a, y + b) – to determine the new coordinates of the image.

Students practice plotting the original points, applying the rule, and then connecting the translated points to reveal the transformed shape. These introductory exercises build a solid foundation for understanding how translations affect geometric figures, preparing them for more complex transformations. Many worksheets include answer keys for self-assessment and teacher verification.

Worksheets with Multiple TransformationsPDF worksheets incorporating multiple transformations challenge students beyond simple translations. These resources often combine translations with other geometric operations like reflections, rotations, and dilations in a single problem. Students must carefully apply each transformation in the correct order to achieve the final image.

These worksheets, such as those found in practice bundles, require a deeper understanding of coordinate plane geometry and the impact of each transformation. They build critical thinking skills as students analyze the sequence of changes and accurately plot the resulting figure. Answer keys are essential for verifying the complex steps involved;

Emoji-Based Translation ActivitiesEmoji-based translation activities, available as PDF worksheets, offer a fun and engaging way to practice coordinate plane transformations. These worksheets present incomplete emoji designs, requiring students to apply translations – and often other transformations like reflections, rotations, and dilations – to complete the image.

These activity sheets, increasing in difficulty, provide a visual and motivating context for learning. Students practice graphing coordinates and understanding how transformations affect shapes, all while creating recognizable emojis. This approach makes learning geometry more accessible and enjoyable, reinforcing skills in a playful manner.

PDF translation worksheets require students to graph, identify rules, and write algebraic rules for transformations. CKMath bundles provide comprehensive practice for these skills.

Identifying the Translation RuleTranslation worksheets, frequently available as PDF downloads, heavily emphasize identifying the rule governing the shift. Students analyze pre-image and image coordinates to determine the ‘a’ and ‘b’ values in the (x, y) → (x + a, y + b) rule.

Worksheets often present paired points, requiring learners to calculate the change in x and y values. This process builds a foundational understanding of how translations affect coordinate positions.

Some PDF resources, like those from CKMath, include worksheets where students must deduce the rule from a graphed translation, strengthening visual-spatial reasoning alongside algebraic skills. Accuracy is key when determining these rules.

Graphing TranslationsCoordinate plane translation worksheets, often in PDF format, provide ample practice in graphing translations. Students are typically given a pre-image shape, a translation rule (e.g., (x, y) → (x + 2, y — 1)), and a coordinate grid.

The task involves applying the rule to each vertex of the pre-image and plotting the corresponding translated points to form the image. Utilizing graph paper, as suggested, is crucial for precision.

Many PDF worksheets, including those for 8th grade, present multiple translation exercises, progressively increasing in complexity. Mastering this skill is fundamental for understanding geometric transformations.

Writing Algebraic Rules for TranslationsCoordinate plane translation worksheets, frequently available as PDF downloads, challenge students to reverse-engineer translation rules. Given a pre-image and its translated image on a grid, learners must determine the change in x and y coordinates.

This involves comparing corresponding vertices and identifying the constant values added to or subtracted from the x and y coordinates. The resulting rule is expressed in the form (x, y) → (x + a, y + b).

Worksheets from resources like CKMath specifically require students to articulate these algebraic rules alongside graphing the translations.

PDF worksheets explore translations with negative values and function notation, alongside composing translations with rotations, reflections, and dilations for complex problems.

Translations with Negative ValuesCoordinate plane translation worksheets, frequently available as PDF downloads, often challenge students with translations involving negative numbers. These exercises require a solid understanding of how subtracting from the x and y coordinates affects the image’s position.

Worksheets present scenarios where the translation rule includes ‘-a’ or ‘-b’, demanding students accurately plot points shifted left or down. Mastering this concept is crucial, as it builds a foundation for understanding more complex transformations.

These PDF resources often include answer keys, allowing for self-assessment and reinforcing the correct application of the translation rule with negative values. Students practice applying the rule (x, y) → (x — a, y ౼ b) effectively.

Translations and Function NotationCoordinate plane translation worksheets, often provided as PDF files, can extend to incorporating function notation to represent transformations. This advanced approach links translations to the concept of functions, where the original point (x, y) becomes an input, and the translated point is the output.

Worksheets might present a function like T(x, y) = (x + a, y + b) and ask students to apply it to given coordinates. This bridges the gap between geometric transformations and algebraic representation.

Understanding this connection is vital for higher-level geometry and pre-calculus. These PDF resources help students see translations not just as shifts, but as functions operating on coordinate pairs.

Composing Translations with Other TransformationsCoordinate plane translation worksheets, frequently available as PDF downloads, often challenge students with combined transformations. These exercises move beyond single translations, requiring students to apply a translation followed by another transformation – like a rotation, reflection, or dilation.

Worksheets might present a shape, a translation rule, and then a subsequent transformation. Students must carefully apply each step in the correct order to determine the final image.

This builds critical thinking and reinforces the understanding that the order of transformations matters. Mastering this composition is key for advanced geometry concepts, and PDF worksheets provide focused practice.

Many coordinate plane translation worksheet PDF options include helpful answer keys for self-checking. Others are designed for focused in-class practice or homework assignments.

Worksheets Including Answer KeysCoordinate plane translation worksheet PDFs frequently incorporate answer keys, a crucial feature for both students and educators. These keys allow students to independently verify their solutions, fostering self-reliance and a deeper understanding of the concepts.

For teachers, answer keys significantly reduce grading time and provide a quick reference for identifying common student errors. Resources like the CKMath worksheet bundles specifically mention included answer keys, ensuring accuracy and efficient learning.

Having readily available solutions promotes a more effective learning environment, enabling focused instruction on areas where students require additional support. This feature is invaluable for both classroom and homework assignments.

Worksheets for In-Class PracticeCoordinate plane translation worksheet PDFs are exceptionally useful for structured in-class practice. Resources like the CKMath bundles are specifically designed to reinforce concepts immediately after instruction. These worksheets provide a focused environment for students to apply their knowledge under teacher guidance.

They allow for real-time assessment of understanding, enabling educators to address misconceptions promptly. Activities involving graphing coordinates and writing algebraic rules, as found in these PDFs, promote active learning.

In-class worksheets foster collaboration and peer learning, solidifying comprehension through discussion and problem-solving.

Worksheets Designed for HomeworkCoordinate plane translation worksheet PDFs serve as excellent homework assignments, reinforcing concepts learned in class. CKMath bundles, for example, are suitable for independent practice, allowing students to solidify their understanding at their own pace. These worksheets often include a range of problems, from basic translations to more complex scenarios.

Homework worksheets encourage students to practice identifying translation rules and applying them to graph coordinates. The inclusion of answer keys allows for self-assessment and promotes accountability.

Consistent homework practice builds confidence and prepares students for future assessments.

Coordinate plane translation worksheet PDFs are commonly used in 8th grade, but also extend into Geometry, offering challenges for varied skill levels.

8th Grade Translation WorksheetsCoordinate plane translation worksheets, readily available as PDF downloads, are specifically designed to solidify 8th-grade geometry concepts. These resources focus on foundational skills, like identifying translations and applying the (x, y) → (x + a, y + b) rule.

Worksheets often present pre-graphed shapes, requiring students to determine the translation rule or graph the image after a given translation. Some PDFs, like those from 8th Grade PDF Worksheets, include sections for performing multiple transformations sequentially.

These exercises build a strong base for understanding more complex transformations encountered in higher-level math courses, ensuring students grasp the core principles of geometric movement.

Worksheets for Higher Grades (Geometry)Geometry translation worksheets, often in PDF format, extend beyond basic shifts, challenging students with more intricate applications. These resources delve into composing translations with other transformations – reflections, rotations, and dilations – requiring a deeper understanding of coordinate geometry.

Worksheets may involve proving geometric theorems related to translations or applying them to complex shapes and functions. Some PDFs, like those found in practice activity bundles, incorporate emoji-based activities to make practice engaging.

These advanced exercises prepare students for rigorous geometric proofs and problem-solving, building upon the foundational skills learned in earlier grades.

PDF translation worksheets are readily available online through resources like CKMath and various educational websites offering free printable materials for practice.

Online Resources for Translation WorksheetsNumerous online platforms provide coordinate plane translation worksheets in PDF format. CKMath offers comprehensive worksheet bundles designed to reinforce concepts after instruction, suitable for in-class practice or homework assignments. These often include answer keys for easy assessment.

Beyond CKMath, a general internet search reveals various free printable options. Websites dedicated to math resources frequently host collections of transformation worksheets, including those focused specifically on translations. Look for resources offering varying difficulty levels to cater to diverse student needs. Some sites even feature interactive tools alongside the downloadable PDFs.

CKMath Worksheet BundlesCKMath provides dedicated Transformations on the Coordinate Plane Practice Worksheet Bundles, available as PDF downloads. These bundles are specifically designed to reinforce understanding after initial teaching, offering versatile use for in-class activities or homework.

Worksheets within these bundles require students to locate and graph coordinates, and to articulate algebraic rules and descriptions for transformations they observe. A significant benefit is the inclusion of comprehensive answer keys, streamlining the grading process for educators and providing self-assessment opportunities for students.

Free Printable Translation WorksheetsNumerous online resources offer free printable translation worksheets in PDF format. These resources cater to various skill levels, from basic coordinate shifts to more complex scenarios involving multiple transformations.

Many worksheets focus on identifying translation rules from graphed images, while others challenge students to graph translations given an algebraic rule. Some even incorporate engaging activities, like emoji-based challenges, to make practice more enjoyable. These readily available resources provide accessible practice for students learning coordinate plane translations.

PDF translation worksheets are most effective when starting with simple shifts, encouraging work checks, and utilizing graph paper for precise coordinate plotting.

Start with Simple TranslationsBeginner-level translation worksheets, often available as PDF downloads, should focus on straightforward shifts – moving shapes left, right, up, or down. These initial exercises help students grasp the core concept of adding or subtracting values from coordinates.

Avoid worksheets immediately introducing multiple transformations or negative values. Instead, concentrate on positive integer translations. This builds a solid foundation before tackling more complex problems.

Resources like those from CKMath offer excellent introductory practice. Gradually increase difficulty as students demonstrate mastery, ensuring they understand the fundamental rule: (x, y) → (x + a, y + b).

Encourage Students to Check Their WorkWhen using translation worksheets – often found as PDF printables – emphasize the importance of verification. Students should re-apply the translation rule to their new coordinates to confirm accuracy.

Visually checking the graph is also crucial. Does the translated image maintain the original shape’s size and orientation?

Worksheets with included answer keys, like those from CKMath, provide a valuable self-assessment tool. Encourage students to compare their solutions and identify any errors in applying the translation rule or plotting points. This fosters independent learning and reinforces understanding.

Use Graph Paper for AccuracyWhen working with translation worksheets, especially those in PDF format requiring graphing, utilizing graph paper is paramount. The gridlines provide a visual framework, minimizing errors in accurately plotting translated coordinates.

Precise plotting is essential for demonstrating understanding of the translation rule. Graph paper helps students maintain consistent spacing and avoid misinterpreting the coordinate plane.

Many worksheets, including those designed for in-class practice or homework, benefit from this approach. It’s particularly helpful when dealing with multiple transformations or complex translation rules.

PDF translation worksheets often see errors like misapplying the rule, misinterpreting the coordinate plane, or forgetting directional components (a, b) in (x, y) → (x + a, y + b).

Incorrectly Applying the Translation RuleIncorrectly applying the translation rule is a frequent issue when students work with coordinate plane translation worksheets, often in PDF format. A common mistake involves adding ‘a’ and ‘b’ to the wrong coordinates – students might add ‘a’ to the y-coordinate and ‘b’ to the x-coordinate instead of following (x, y) → (x + a, y + b).

Another error is forgetting to apply the rule to both coordinates of each point. Students may only adjust the x-value, leaving the y-value unchanged. Careful attention to the order of operations and a systematic approach to each point are crucial for avoiding these pitfalls. Double-checking work is highly recommended!

Misinterpreting the Coordinate PlaneMisinterpreting the coordinate plane is a common stumbling block when using translation worksheets, particularly those in PDF format. Students sometimes struggle with correctly identifying the signs of coordinates – confusing quadrants or misreading positive and negative values. This leads to incorrect translations, as the direction and distance of the shift are based on these values.

Carefully labeling axes and consistently checking the signs of coordinates before applying the translation rule are essential. Utilizing graph paper, as suggested, can help visualize the plane and minimize errors. A solid understanding of quadrant rules is also vital for success.

Forgetting to Include Direction in the RuleA frequent error when working with translation worksheets, often found as PDF downloads, is omitting the correct direction within the translation rule (x, y) → (x + a, y + b). Students may remember to add or subtract a value, but neglect the ‘+’ or ‘-’ sign, fundamentally altering the translation.

This oversight stems from rushing or a lack of careful attention to detail. Emphasize that the ‘a’ and ‘b’ values represent directed movement – positive for right/up, negative for left/down. Reinforce checking the rule’s signs before applying it to coordinates.

Online tutorials and interactive tools supplement translation worksheet PDF practice. Explore geometry textbook chapters for deeper understanding of transformations.

Online Tutorials on Coordinate Plane TranslationsNumerous online platforms offer excellent tutorials to complement coordinate plane translation worksheet PDF practice. Khan Academy provides comprehensive videos explaining translations, alongside practice exercises. YouTube channels dedicated to mathematics, such as PatrickJMT, offer step-by-step guidance on applying translation rules and graphing translated images.

These tutorials often visually demonstrate the process, making it easier to grasp the concept. They can be particularly helpful for students who benefit from seeing problems solved in real-time. Supplementing worksheet practice with these resources ensures a thorough understanding of translations and their applications.

Interactive Translation ToolsBeyond coordinate plane translation worksheet PDFs, interactive tools enhance learning. GeoGebra offers a dynamic geometry environment where students can manipulate shapes and visualize translations in real-time. Desmos, known for its graphing calculator, allows users to input translation rules and observe the resulting image instantly.

These tools provide immediate feedback, fostering a deeper understanding of how translations affect coordinates. They encourage exploration and experimentation, solidifying the concept beyond static worksheets. Utilizing these interactive platforms alongside traditional practice builds a robust skillset.

Geometry Textbook Chapters on TransformationsTraditional geometry textbooks dedicate significant sections to transformations, including translations. These chapters provide a foundational understanding of the underlying principles, often complementing coordinate plane translation worksheet PDF practice. They typically define translations formally, explaining the rule (x, y) → (x + a, y + b) and its implications.

Textbooks offer worked examples, proofs, and a broader context for understanding translations within the larger framework of geometric transformations. They are invaluable resources for students seeking a comprehensive grasp of the subject matter.

The post translations on the coordinate plane worksheet pdf appeared first on Every Task, Every Guide: The Instruction Portal

.

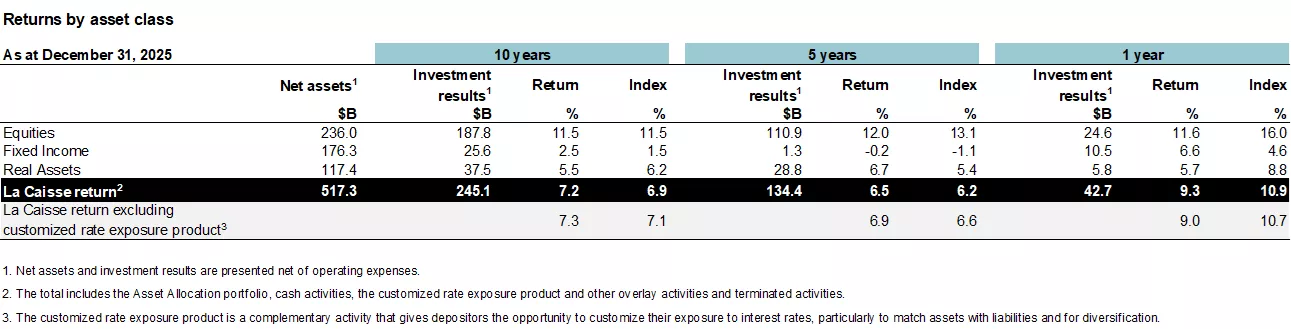

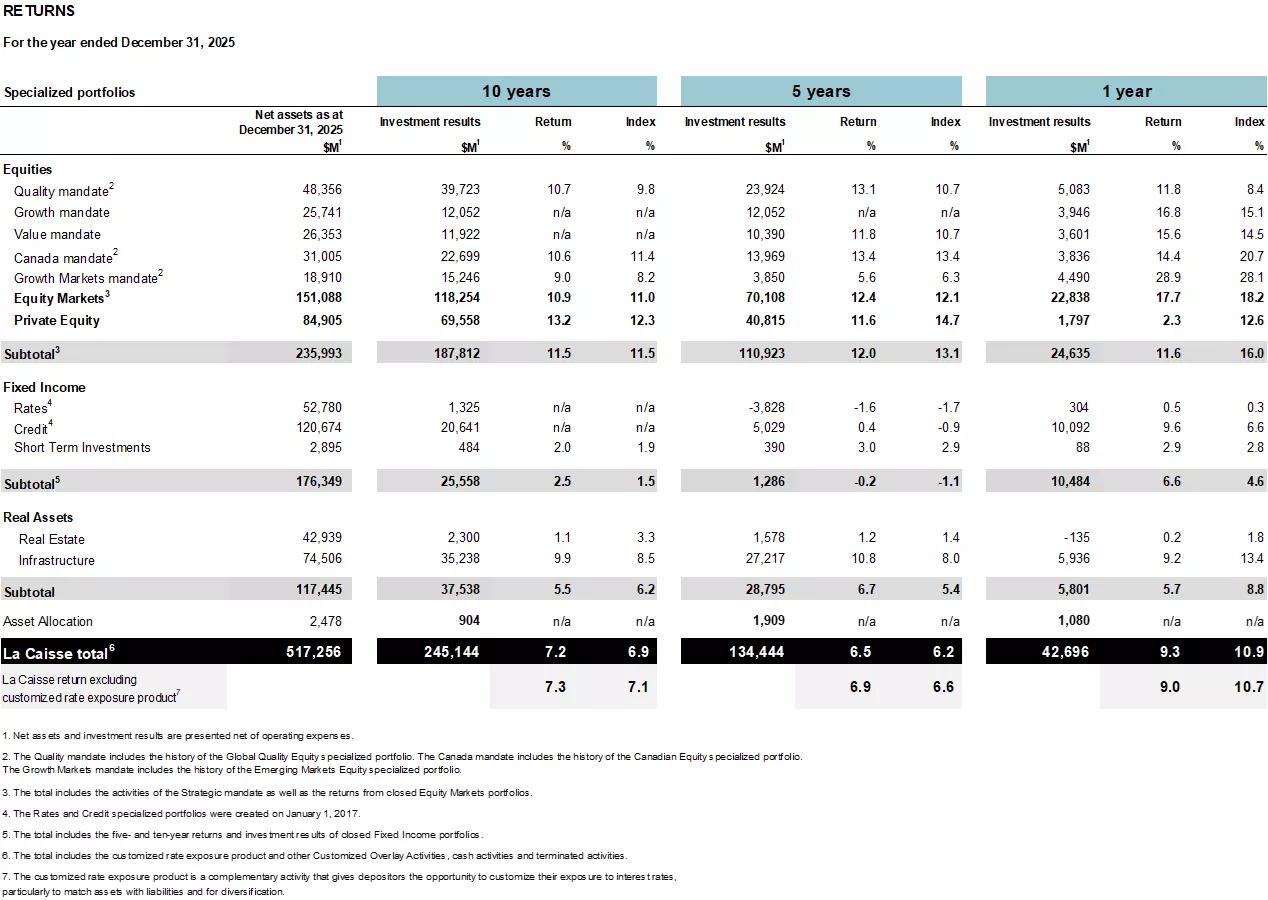

Equities

Equities About La Caisse

About La Caisse

Assets by Geography

Assets by Geography Investment Performance Highlights

Investment Performance Highlights

Recent comments