A Senate hearing on the credit rating agencies, Wall Street and the Financial Crisis: The Role of Credit Rating Agencies, exposed Moody's and Standard & Poors for being complicit in fictional credit ratings. Market share, or who pays the ratings agencies, was more important than objectivity. AAA credit ratings were slapped on a host of Credit Default Obligations, enabling Banksters to peddle their worthless crud to unsuspecting investors, all the while betting against them (see here also).

If employees didn't rate this junk with AAA, dared to point out the ratings was fiction, they were fired. Of course Moody's and S&P just denied they fired people for questioning fictional ratings. Right.

The most damning testimony is by former Moody's employee Eric Kolchinsky:

The incident which I believe caused me to lose my role at the rating agency occurred in September of 2007. During the course of the year, the group which rated and monitored subprime bonds did not react to the deterioration in their performance statistics. That changed by the late summer of 2007. In early September, I was told that the ratings on the 2006 vintage of subprime bonds were about to be downgraded severely. While the understaffed group needed time to determine the new ratings, I left the meeting with the knowledge that the then current ratings were wrong and no longer reflected the best opinion of the rating agency.

This information was critical for the few CDOs in my pipeline, which were being hyper-aggressively pushed by the bankers. Our rating methodology for these transactions used the ratings which were about to be downgraded as a basis for our ratings. If the underlying ratings were wrong, the ratings on these CDOs would be wrong too. I believed that to assign new ratings based on assumptions which I knew to be wrong would constitute securities fraud. I immediately notified my manager and proposed a solution to this problem.

My manager declined to do anything about the potential fraud, so I raised the issue to a more senior manager. As a result of my intervention, a procedure for lowering subprime bond ratings going into CDOs was announced on September 21, 2007. I believe that this action saved Moody’s from committing securities fraud. Because of the culture, I knew what I did would possibly jeopardize my role at Moody’s.

Just about a month later, in mid-October, another periodic market share email was sent to the Managing Directors in my group. Along with the email, our business manager noted that our market share dropped from 98% plus to 94% in the third quarter. My manager immediately replied to the email and demanded an accounting of the missing deals.

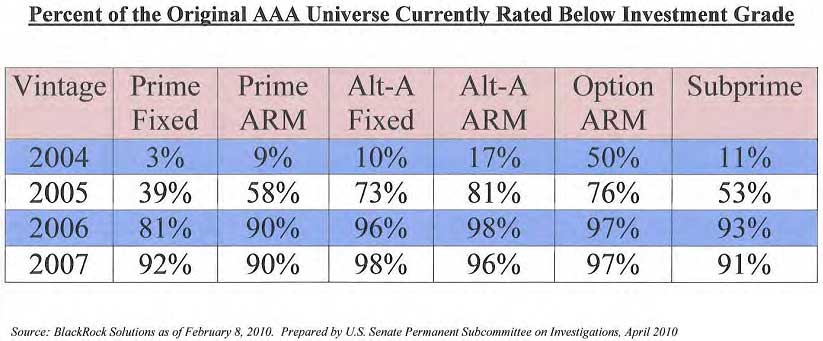

This was the most disturbing email I had ever received in my professional career. A few days before, Moody’s had downgraded over $33 billion in subprime bonds. At the time, this was the largest ever single downgrade at Moody’s. However, as a direct result of the October 07 and additional downgrades, over $570 billion of ABS CDOs would be downgraded through the end of 2008.

Despite the massive manifest errors in the ratings assigned to structured finance securities and the market implosion we were witnessing, it appeared to me that my manager was more concerned about losing a few points of market share than about violating the law.

In late October, less than a month after that email and less than two months after I intervened, my manager asked me to leave the group. I was given a smaller position with less responsibility and less pay in another group. I believe that this demotion was in retaliation for my earlier actions in September.

I believe you Anita! Seriously, anyone working in the private sector knows the pressures to do the corporate party line and if you don't, no matter how disastrous the consequences if you do....then you are at least fired and probably threatened with a confidentiality, NDA agreement violation to boot.

Another Moody's VP Richard Michalek, testified. Most interesting is how the blame ended up at the feet of the quants, the ones writing the mathematical models for ratings. But here is the crux of the fraud:

While we did not unquestionably accept assets with ratings solely from other agencies, we did unquestionably accept the Moody's ratings on the assets. We continued to accept these ratings even after it was known (or should have been known) that due to increased deal flow and a lack of resources, some of the outstanding Moody's ratings on RMBS assets were extremely stale, and therefore less reliable.

Moody's built their house of cards knowing they were adding ratings on bad, invalid, other Moody's ratings.

As the deal flow began to slowly increase after the 2001 recession, the role and use of “precedent” - relying on a prior Moody's-rated transaction as a “template” for the instant transaction being reviewed – steadily became more important.

Now check out who got this guy fired. The Banksters, who didn't like his ratings!

During my tenure at Moody's, I was explicitly told that I was “not welcome” on deals structured by certain banks, however, I never saw a 'list'. I was told by my then-current managing director in 2001 that I was “asked to be replaced” on future deals by Chris Ricciardi, who headed the structured group at CSFB, and then at Merrill Lynch. Years later, I was told by a different managing director that a CDO team leader at Goldman Sachs also asked, while praising the thoroughness of my work, that after four transactions he would prefer another lawyer be given an opportunity to work on his deals. I also understand that Lehman Brothers requested my “rotation”, as did UBS. When Mr Ricciardi left CSFB to head the structured group at Merrill Lynch, I was co-incidentally “re-assigned” off of a Merrill Lynch deal on which work had not yet begun, even though I had never worked on a Merrill CDO before. In each case, I never was assigned to that bank's CDO deals again.

Aha, don't like the Sheriff, run 'em out of town!

The committee has released a 24MB file of exhibits (download! that's huge!) In going through them a few excerpts for your outrage pleasure:

Of the top clients, the guys who pay for the ratings, of the agencies, we have Merrill Lynch as #1 and Citigroup as #2. Recall Merrill Lynch was in a shotgun marriage with Bank of America and Citigroup is still in financial trouble, with major holdings by the U.S. Treasury.

If you can believe this, currently the Senate Reform Bill does nothing in separating the banks, financial institutions from paying the ratings agencies directly.

Let's see, if the one's paying the bills are the ones you are supposed to be objectively evaluating and that evaluation means billions of dollars. What could possibly happen?

The video of the hearing, in it's entirety, is here.

Comments

This Was Obvious

I knew this in 2008. People are talking this up now like its something new. New for the media maybe.

I also knew AIG was tanking in July 2008.

Sure is not new, but a good story deserves repeating

But the reason to amplify it in a hearing is because they are going to pass Financial Reform and there is nothing in there to stop these obvious conflicts of interest, then the same stuff is still going on to this day. The banksters are still their customers, the ones paying their bills.

We're seeing a lot of rehash of material and I believe it was Barry Ritholtz who especially pounded on the credit ratings agencies, wrote about a lot of this, before the meltdown hit.

Of course these poor guys who were canned because they dared pipe up is new. One has to give them a break or anyone who gets fired, their career probably destroyed, simply because they are trying to do the right thing, often their actual job description.

That's why I'm summing it all up in "Blogger speak". It's not new, although some of this evidence I have not seen before (the 24MB). They need to separate out completely credit ratings agencies from who actually pays them, in my view.

Reverse Engineering of Ratings

A New York Times article, points to the hiring away of a credit rating agency's (Fitch) derivatives modeling expert. Then the silly rating agencies gave the Banksters their evaluation models, making it much easy to game a CDO.

Now hiring away someone so you can reserve engineer a technique is pretty common actually in engineering. One works around their own patents all of the time. That said, I think there should be a series of NDAs, confidentiality agreements and I also believe the ratings agencies should have some sort of intellectual property protection on their own proprietary models.

In tech at least, walking into a competitor with any documents, code, well anything owned by the past company can get you into huge trouble and most are ethical, would never do such a thing. That said, if someone write a technique, odds are they can design around that very design to something new.

But the bottom line here is CDOs by their nature cannot be verified and thus easily rigged and that is without knowledge of how the credit ratings agencies are assessing them.

Why no Transperancy on Mortagage Baskets of CDOs?

CDOs derive ultimately from packages of mortgages.

The collateral for these instruments is the mortgage basket. Each of these mortgages has a debtor with a credit rating. It is relatively simple to come up with a combined credit score for the CDO if you base it on the weighted average of the credit score for all of the mortgages representing the CDO.

Rating can be done anonymously without compromising the privacy of the debtors. If it is not done by the banks or rating agencies, we will never learn the risks and the sorry history of this decade will repeat itself.

This proposal is politically naive. Mortgages have demographics and ethnicity like everything else and there lies a mine field.

Burton Leed

A SnapShot of Merrill Lynch in 1997 - World of DADT Finance

Consulting for ML's CMA account in 1997, I asked a IT manager how M: could skirt the rules of Glass Stegull so casually. Keep in mind, we are a couple of years before Graham-Leach. The manager said,

"We just thumb our noses at Glass-Stegull"

He went on to explain how ML allows its clients to invent any kind of transaction they can wet-dream. The relevance to IT was that this activity (a fig leaf term), was blowing out all the DASD channel I/O to the point where they needed much more high-throughput DASD.

The 'reform' Bill promises a return to Glass Steagull. How will GS fix these sick scenes? All of this is not new, its is part of the sickness we call Capitalism.

Burton Leed

reform bill does not return Glass-Steagull

Not the last version I reviewed. We're got our classic "compromise" coming in the Senate and I'll bet dollars to donuts it's corporate lobbyist loophole ridden. I suggest we all try to find out what the latest is, but be aware, even in a debate on the house floor, at the last minute, one can get a "managers amendment" which is passed by "voice vote" and it can change a bill entirely. Also, even after a bill is passed, they will send "conferees" to "resolve the differences" between the Senate and House version. Literally, after amendments have passed by an overwhelming majority in both houses, these conferees have and can rip out those amendments. They did this on H-1B amendments in a bill a couple of years ago.