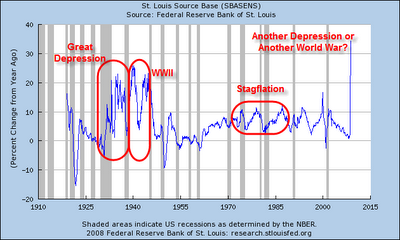

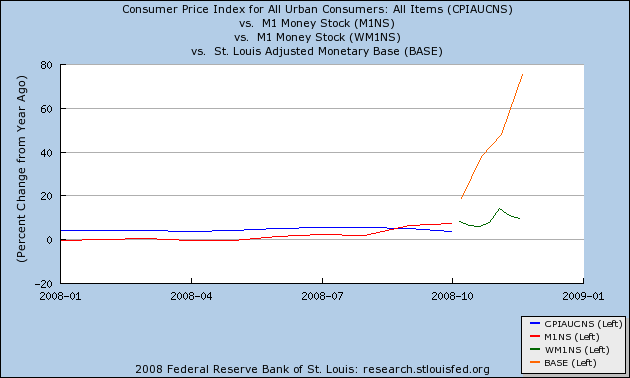

Introduction

On December 3, John Bergstrom of Bergrstrom Automotive, a major auto dealer, appeared on CNBC and said,

on about September 10, we saw our business fall off 30-35%.

A similar sudden decline in consumer spending during September was reported by Shoppertrak:

Throughout 2008, the American shopper has endured record high gasoline prices, hurricanes and flooding, and a stalled housing market in their quest to shop. While the consumer has remained fairly resilient during this time, two very recent events are dramatically impacting mall visits and consumer confidence.

- Once the financial crisis emerged at the beginning of September, retail traffic declined even further. Between August 31 and September 20, SRTI total U.S. traffic fell an estimated 9.2 percent per day....

- After the failure of Washington Mutual, President Bush’s address to the nation, the presidential debate and the initial rejection of the TARP bailout, traffic fell by an average of 10.5 percent (September 21 – 29).

- The day the TARP bailout package was rejected by congress (September 29) and the NYSE Dow Jones Industrial Average lost 778 points, consumers again responded negatively as shopper traffic fell 12 percent as compared to the same day in 2007

- Sales, which were up 4.0 Percent for the Month of July, and up 3.5 Percent for the Month of August, fell 1.0 percent in September – "the first year-over-year sales decline since March 2003."

Shoppertrak has subsequently reported that "retail sales rebounded slightly, posting a very slight 0.7 percent increase in October. sales for the week ending November 15 dropped 3.1 percent as compared to the same period in 2007." But car sales have not recovered at all. In August car sales were already down about 19% YoY. In September the loss was 21%. In October it was 23%. By November car sales had declined close to 40% from already depressed levels in 2007.

And the stock market, which was only down (-18%) from its all time high in 2007 of 1565 to 1282 at the end of August, by October 10 was down (-43%) to 899.

In the 40 day period between September 1 and October 10, the shallow recession which had crippled the housing industry and Wall Street, but left Main Street virtually intact, suddenly metastasized into a collapse of the consumer economy that some were beginning to liken to the 1930s.

This diary is "the first draft of history", an attempt to look at not only what has happened, but as best we can tell from the vantage point of several months later, why it happened.

Recent comments