The Bank for International Settlements has demanded Central Banks stop their quantitative easing in hopes of a global economic recovery. All that has happened is a stock market love affair while the real economy languishes. BIS has issued their annual report demanding nations deleverage, which is codespeak for austerity. The Bank for International Settlements is the bank of the central banks, so these ultimatums to their 58 Central Bank members are significant. The BIS demand is clear, quit quantitative easing, adding to balance sheets and issuing zero interest rates and get back to layoffs, downsizing and austerity. Those are the BIS marching orders to their members as their annual report implies Central Banks are simply staving off the inevitable with unforeseen financial consequences.

Six years ago, in mid-2007, cracks started to appear in the financial system. Little more than a year later, Lehman Brothers failed, bringing advanced economies to the verge of collapse. Throughout the ensuing half-decade of recession and slow recovery, central banks in these economies have been forced to look for ways to increase their degree of accommodation. First they lowered the policy rate to essentially zero, where it has been ever since in the United States, United Kingdom and euro area. (And where it has stood in Japan since the mid-1990s!) Next, these central banks began expanding their balance sheets, which are now collectively at roughly three times their pre-crisis level – and rising.

Originally forged as a description of central bank actions to prevent financial collapse, the phrase “whatever it takes” has become a rallying cry for central banks to continue their extraordinary actions. But we are past the height of the crisis, and the goal of policy has changed – to return still-sluggish economies to strong and sustainable growth. Can central banks now really do “whatever it takes” to achieve that goal? As each day goes by, it seems less and less likely. Central banks cannot repair the balance sheets of households and financial institutions. Central banks cannot ensure the sustainability of fiscal finances. And, most of all, central banks cannot enact the structural economic and financial reforms needed to return economies to the real growth paths authorities and their publics both want and expect.

What central bank accommodation has done during the recovery is to borrow time – time for balance sheet repair, time for fiscal consolidation, and time for reforms to restore productivity growth. But the time has not been well used, as continued low interest rates and unconventional policies have made it easy for the private sector to postpone deleveraging, easy for the government to finance deficits, and easy for the authorities to delay needed reforms in the real economy and in the financial system. After all, cheap money makes it easier to borrow than to save, easier to spend than to tax, easier to remain the same than to change.

Yes, in some countries the household sector has made headway with the gruelling task of deleveraging. Some financial institutions are better capitalised. Some fiscal authorities have begun painful but essential consolidation. And yes, much of the difficult work of financial reform has been completed. But overall, progress has been slow, halting and uneven across countries. Households and firms continue to hope that if they wait, asset values and revenues will rise and their balance sheets improve. Governments hope that if they wait, the economy will grow, driving down the ratio of debt to GDP. And politicians hope that if they wait, incomes and profits will start to grow again, making the reform of labour and product markets less urgent. But waiting will not make things any easier, particularly as public support and patience erode.

Alas, central banks cannot do more without compounding the risks they have already created. Instead, they must re-emphasise their traditional focus – albeit expanded to include financial stability – and thereby encourage needed adjustments rather than retard them with near-zero interest rates and purchases of ever larger quantities of government securities. And they must urge authorities to speed up reforms in labour and product markets, reforms that will enhance productivity and encourage employment growth rather than provide the false comfort that it will be easier later.

The report is quite offensive. They promote creative destruction and claim firing people more easily and lowering wages helps an economy. The BIS also implies to grow an economy they need to destroy worker projections, such as unions and labor laws. There is much double speak from BIS, hiding the demand that workers be squeezed, industries shuttered and somehow people will in turn get jobs in these amazing new economic sectors that will spring up. The codeword is productivity, which if one looks at labor productivity, we see lowering wages for the same economic output increases these figures.

By hindering the reallocation of capital and workers across sectors, structural rigidities put the brakes on the economic engine of creative destruction.

On austerity, the BIS targets again working people and promotes cuts to pensions and health care to reduce government budget deficits. War, privatization is never mentioned or absurd elements which are completely ineffective, such as the costs of keeping marijuana illegal. The agenda to re-create a world of serfs and elites is never ceasing, now under the claim hurting workers on a global scale will save the economy. One must wonder at this point, whose economy they are referring to?

Measures to curb future increases in pension and health care spending are key to the success of these efforts.

At the FOMC press conference, Federal Reserve chair Ben Bernanke warned the party is coming to an end on quantitative easing, with an unemployment rate target of 7%. Yet the official unemployment rate does not count the millions who are no longer part of the labor force, but actually need a job.

If the incoming data are broadly consistent with this forecast, the Committee currently anticipates that it would be appropriate to moderate the monthly pace of purchases later this year; and if the subsequent data remain broadly aligned with our current expectations for the economy, we would continue to reduce the pace of purchases in measured steps through the first half of next year, ending purchases around midyear. In this scenario, when asset purchases ultimately come to an end, the unemployment rate would likely be in the vicinity of 7 percent, with solid economic growth supporting further job gains.

While the BIS worker squeeze agenda is absurd on it's face, the BIS also has truth in their annual report. Nations have delayed real financial reform and are not investing in new industries, retraining their citizens through these industries to grow the real, production economy. Wall Street's quantitative easing crack cocaine has primarily been a rich person's benefit. The amount of QE buzz these people need to even create one new job seems not worth the artificial high quantitative easing costs down the road. To wit, the BIS reports gives warnings of incredible bond losses if interest rates and yields start to rise.

Consider what would happen to holders of US Treasury securities (excluding the Federal Reserve) if yields were to rise by 3 percentage points across the maturity spectrum: they would lose more than $1 trillion, or almost 8% of US GDP.

The losses for holders of debt issued by France, Italy, Japan and the United Kingdom would range from about 15 to 35% of GDP of the respective countries. Yields are not likely to jump by 300 basis points overnight; but the experience from 1994, when long-term bond yields in a number of advanced economies rose by around 200 basis points in the course of a year, shows that a big upward move can happen relatively fast. And while sophisticated hedging strategies can protect individual investors, someone must ultimately hold the interest rate risk. Indeed, the potential loss in relation to GDP is at a record high in most advanced economies.

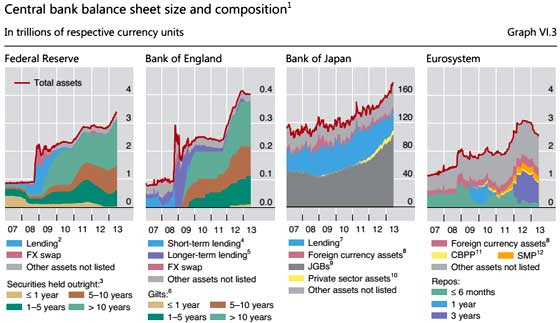

The BIS bond loss projection is scary stuff and one graph from the BIS annual report is truly stunning. Below is select Central Banks balance sheets.

Bottom line, quantitative easing is no answer, but neither are the BIS implied policies. Unfortunately FDR and uncorrupted politicians aren't around these days to save the nation and global economies. What we need is a refocus on citizens and labor instead of the never ending drone of austerity and the creative destruction agenda. If either of these policies actually worked to reboot an economy, we'd all be rising the wave of roaring GDP by now.

Comments

BIS Rides again

Ah, the BIS. This was the money laundering machine the Nazis used to move profits from looting the Jews and others. BIS continued to operate as an independent entity for the duration of WW2, facilitating funds transfers between Fascist Europe and the Allies. Many interesting stories about that if you dig a little. So now they continue their service on behalf of the plutocracy. A pox on them.

QE and its beneficiaries

The FED's pious bleats -- expressing their concern for "The Unemployed" -- are nothing more than a thin fig leaf for its actual mission of reflating banks mortgage-backed-assets and the rest of the debris from their most recent credit bubble.

See the FED's cummulative QE (blue line, left axis) and its sum-total effect on employment (red line, right axis) on http://research.stlouisfed.org/fred2/graph/?g=j0h

See that same QE effort -- and its effect on the S&P 500 (and other like financial assets) -- on http://research.stlouisfed.org/fred2/graph/?g=iQe

A perhaps more sobering look-see is in the net, after-tax profits of the financial industry (red line, right axis) as a fraction of all U.S. Corporate profits -- as compared with the blue line that shows the fraction of all remaining PAT going to all our non-financial industries on http://research.stlouisfed.org/fred2/graph/?g=iZU.

For reference, real (after inflation) interest rates are shown by the gray line (left axis).