The Federal Reserve's consumer credit report for March 2012 shows a 10.2% annualized monthly increase in consumer credit. Revolving credit increased, 7.8%, and nonrevolving credit surged 11.3%. The Credit Kraken continues it's rampage, after a hiatus in February, mainly on the backs of people going to school.

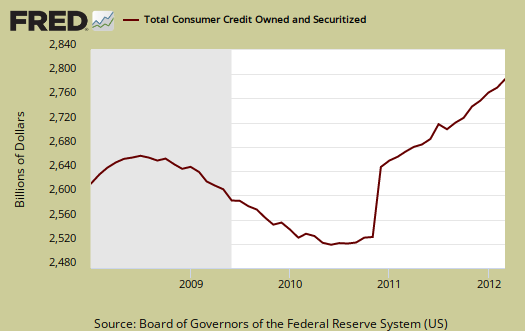

Overall consumer credit increased $21.36 billion dollars to $2.5423 trillion, seasonally adjusted. Revolving credit increased $5.1 billion while non-revolving increased $16.1 billion, the largest amount since November 2001. Revolving credit are things like credit cards and non-revolving are things like auto loans and student loans. Mortgages are not included in this report.

For Q1 2012, overall consumer credit increased 7.7% annualized and the reason for the increase is again non-revolving credit, which jumped a whopping 11.4% for Q1. Revolving credit decreased, 0.1% for the quarter.

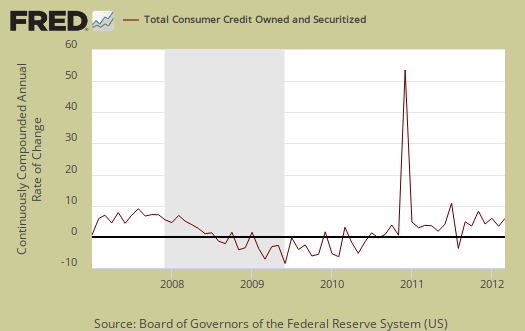

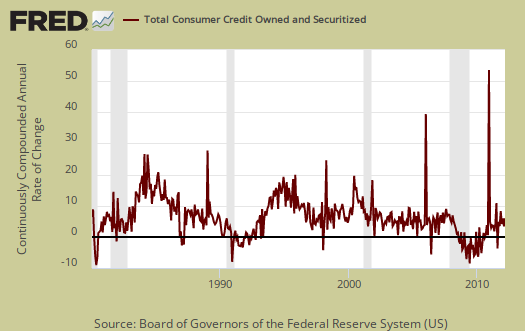

The report gives percent changes in simple annualized rates, also known as a continuously compounded annualized rate of change. To put this change in perspective, at simple annualized rates, consumer credit increased almost to this level in the last 10 years. Consumer credit, annualized, increased 9.3%, in September 2004, 9.2% in October 2004, 9.2% in February 2002 and 18.2% in November 2001. Below is the graph of the monthly annualized percentage changes in consumer credit going back to 1980.

From the above graph we can see outstanding consumer credit drops correlate to recessions. This report does not include charge offs and delinquencies, which hit another low in March:

US credit card charge-offs dropped slightly in March, as the charge-off rate index fell three basis points below its February level, to 4.94%, according to Moody's Credit Card Indices.

"The charge-off rate index is at its lowest point since the second quarter of 2007, down by more than 55% from its 2010 peak," says Jeffrey Hibbs, a Moody's Assistant Vice President and Analyst.

"Some originators have started loosening their underwriting criteria, but so long as they don't add receivables from new accounts to securitizations, the credit mix in trusts won't deteriorate from current levels. Still, we expect the steady decline in the charge-off rate to come to an end, albeit gradually, and find a floor of around 4% by early 2013."

The delinquency rate index and the early stage delinquency rate fell to respective record lows of 2.73% and 0.72% in March, underscoring the exceptionally strong credit quality of securitized credit card receivables today.

Below is total consumer credit.

The increase was due to student loans. Federal government nonrevolving credit, which includes student loans increased another $6.9 billion to $460.2 billion, not seasonally adjusted. The federal government started making 100% of guaranteed student loans in July 2010. People went more into debt, clearly, to pay for the soaring, absurdly high, educational costs. Student loan rates are about to double and Congress is of course roadblocking legislation to stop the increase. Additionally, student loans do not provide much economic stimulus as most of the funds go directly to tuition.

Below is non-revolving credit, seasonally adjusted, annualized percentage change.

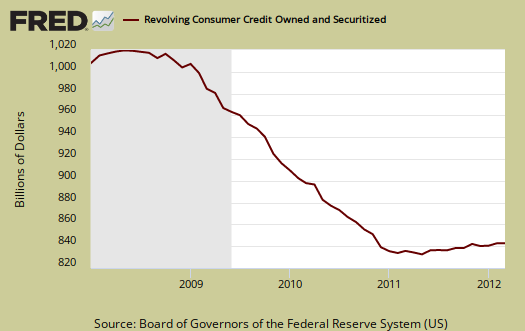

Revolving credit, think credit cards, are back up for March after declines in February and January. Below is revolving credit, raw totals. Charge offs are not included in this report. These numbers are seasonally adjusted.

Other press claimed the increase is due to a better economy. Sorry folks, people don't go into more debt unless they have to, although offering up more debt implies banks think people can pay it back. Students who have reasonable tuition and can get part-time jobs don't go into absurdly high debt. Parents who have careers and savings to help their kids pay for college don't go into debt either.

Compliment

Your article above is an informative and concisely written piece with good supporting economic details. I thought that you / or your readers would find the Wall Street community's discussion on this matter as well as other topics of interest: http://www.wallstreetoasis.com/blog/record-consumer-credit-numbers Our community consists of aspiring / current finance professional users so feel free to use it as a follow up if you like or as an expansion of traffic and readership. I hope all is well and keep up the good work!

thank you

If anyone is wondering why all of the different values, i.e. increased $21.4, $21.3 and $21.36 on overall credit, the Fed publishes data to 1 decimal place and it appears they concatenate instead of round. One can dig around and find the original data and it goes to more decimal places of accuracy. I personally don't know what to think about that, come on Fed, be consistent, are you rounding or not?

On your site, we do take cross posts, articles of interest and we hope EP readers are jumping around the Internets and yes we do love links back to EP!