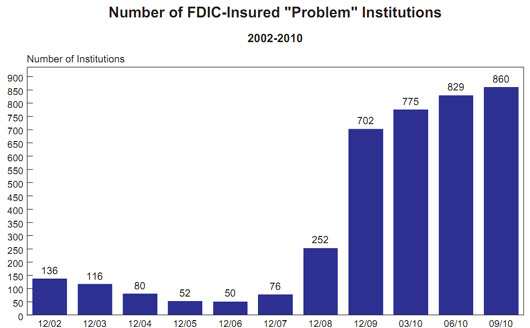

The FDIC announced the problem bank list, which is one step from walking the plank, being seized and shut down, grew to 884 from 860 in Q4 2010. Problem banks are now 11.5% of the 7,657 banks and savings institutions covered by the FDIC.

From the FDIC press release:

The number of institutions on the FDIC's "Problem List" rose from 860 to 884. Total assets of "problem" institutions increased to $390 billion from $379 billion in the prior quarter, but are below the $403 billion reported at year-end 2009. The rate of increase in the number of "problem" banks has declined in each of the past four quarters. Thirty insured institutions failed during the fourth quarter, bringing the total number of failures for the full year to 157.

The FDIC believes bank failures in 2011 will be less than the 157 of 2010. To date, there have been 22 bank failures in the first 7 weeks of 2011. Projecting the current 2011 closure rate onto all of 2011 would be 167. Wikipedia is keeping a tally of closed banks. This time last year, we had 20 bank failures.

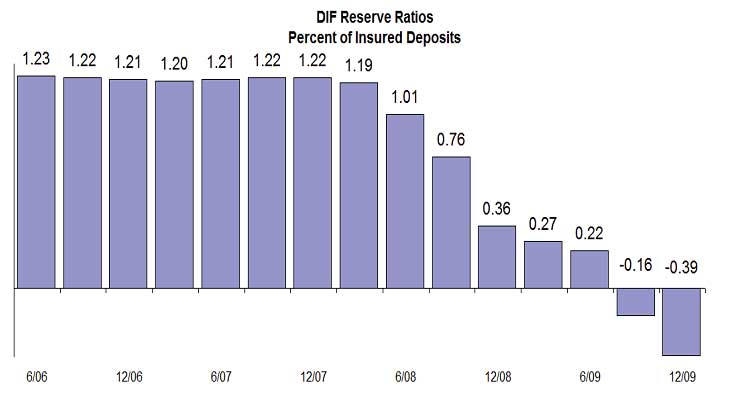

The Deposit Insurance Fund is still in the red and went from a negative balance of -$8 billion to -$7.4 billion.

Here's the weird story. While bank failures and problem banks sprout up like mushrooms, the FDIC is reporting record Q4 profits of $21.7 billion. In Q4 2009, the aggregate commercial banks reported a $1.8 billion dollar loss.

Recent comments