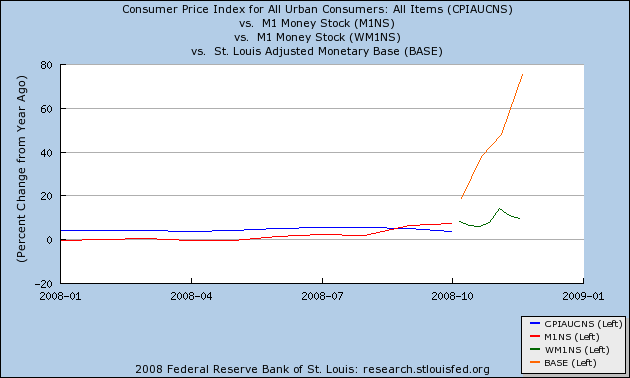

This is a follow up on my previous posts in which I discussed whether we were heading for a deflationary recession or a recovery in 2009. As we found out within the last couple of weeks, the deflationary recession is already here. But are there still grounds to believe a recovery in 2009 is possible? Money supply indicators (m1 [red, green] and monetary base[orange]) continue to indicate so as of this week's update:

It is now virtually certain that the Kasriel indicator will predict a recovery in the first half of 2009.

Update 4:

This week we got a partial answer to the query posed by the title to this series: one of my two possible outcomes was a deflationary recession (an old fashioned "bust"), featuring (-1.5%) or greater deflation on an annual or shorter basis. This week we learned that in the August-October period CPI already declined (-1.5%). Since November and December have a seasonal bias towards slightly negative (-.1 and -.2 respectively) monthly CPI readings, this deflationary recession will almost certainly last into 2009.

Update 2, Nov. 7, 2008: We got three new pieces of data this week, 2 on the monetary front, and one on the inflation front.

On the monetary front, M1 was updated weekly, increasing to ~ +8% YoY. Monetary base continues to soar, up about 60% YoY now!

Meanwhile the ISM manufacturing "prices paid" index showed that more prices are declining than increasing at the producer level:

This is our first October inflation reading, and it strongly suggests we will get another month of deflation when the PPI and CPI come out in 2 weeks.

No, I have not lost my mind, although with a slew of just awful economic data for September and October spilling out, the title of this blog entry is a contrarian statement to say the least. What I mean is, measured by the indicators of past recessions going back all the way through the Great Depression, the shallow recession that I believe started approximately last December, and primarily affected Wall Street with only a glancing blow at Main Street, ought to be ending.

Recent comments