The newly formed Consumer Financial Protection Bureau will start to oversee the companies who generate credit reports on you. That's Experian, Equifax and TransUnion plus about 30 more.

The newly formed Consumer Financial Protection Bureau will start to oversee the companies who generate credit reports on you. That's Experian, Equifax and TransUnion plus about 30 more.

This action can come none too soon. Unscrupulous debt collectors inaccurately report actions to credit reporting bureaus all the time, especially for Medical bills. Getting these illegal collections or inaccuracies and errors off of one's credit report is next to impossible. Credit reporting agencies simply do not respond it seems to challenges. Experian, as an example, doesn't even have a phone number! Of course you can sue them, but even small claims court is not for the faint of heart and it's not guaranteed one will win, even when being in the right.

One of the biggest problems turning up on credit reports are medical bills. Who does not know billing from Medical facilities is loaded with errors, duplicates and mistakes? Yet more and more Medical companies are turning into the sellers of debt and even bring debt collectors into the Medical practices themselves. That's sloppy, inaccurate medical debt, often for services subpar or not rendered. Literally the health care sector is in the business of selling debt, demanding loan shark interest rates, almost the minute you walk out the door from their facility.

Rodney Anderson, a mortgage banker in Plano, Tex., said he started to notice in 2008 that more of his customers were being hurt by these medical delinquencies. So he kept notes on 5,100 loan applicants over 10 months. He found that 2,200 had at least one medical debt that lowered their credit score, and many of them were unaware of the damage.

“It’s the same thing over and over,” said Mr. Anderson, executive director of Supreme Lending. “You just don’t let $100 go to collections to ruin your credit.”

One study found 30 million Americans in 2010 were dealing with collection agencies over medical bills. What is more odious, debt collections agencies refuse to remove their abuse of one's credit report, even when the debt is proved to be paid:

Surprisingly, even after the bills have been paid off, the record of the collection action can stay on a credit report for up to seven years, dragging down credit scores and driving up the cost of financing a home. An estimated 3.4 million Americans have paid-off medical debt lingering on their credit reports, according to the Access Project, a research group funded by health care foundations and advocates of tougher laws on medical debt collectors.

The Federal Reserve found in a recent study half of credit events on reports are medical bills, that's obscene! We have the health care sector turning into debt traders instead of taking care of people!

According to studies published in the Federal Reserve Bulletin, more than half of all accounts in collections on credit reports are medical in nature. Medical collections accounts can stay on a report for up to seven years, even with NO balance due. Collections accounts are reported in the credit history section of a credit report and this section accounts for 35% of a credit score. Because of this, these fully paid “delinquent” medical bills can be devastating. According to a FICO spokesperson, a medical collection — paid or unpaid — can lower a score by 105-125 points for someone with otherwise good credit and a FICO score of 780.

The situation is so bad, literally a breast cancer survivor was jailed for a $280 medical bill. She didn't even owe the money!

In the latest example of aggressive debt collector tactics, an Illinois woman found herself jailed over a bill she didn’t even owe in the first place.

Breast cancer survivor Lisa Lindsay of Herrin, Illinois was put in debtors' prison over a $280 medical bill that was sent to her by accident. Even after Lindsay was told she didn't have to pay the bill, it was sent to a collection agency. Eventually state troopers took her from her home in handcuffs. Lindsay ended up having to pay $600 to settle the charges.

Episodes like Lindsay’s are becoming increasingly common as the number of debts referred to third-party collection agencies has doubled since 2000. Because one third of U.S. states currently allow debtors to be imprisoned, thousands of Americans have been jailed because they can't pay their bills.

Yes Virginia, America does have debtor's prison. It's so bad, hospitals and Doctor's offices are implanting debt collectors while you're trying to receive health care:

The Attorney General of Minnesota was not amused when reports surfaced that a company had slipped collectors disguised as employees into emergency rooms demanding that patients cough up dough before receiving treatment.

I understand that our hospitals are desperate to recoup an estimated $39 billion for unpaid services but what kind of world do we live in where collectors masquerading as hospital employees, perhaps in possession of personal medical information, demand that the feeble, ill, and even the dying pay outstanding medical bills they could not afford in the first place before seeking emergency care. Does the phrase "Physician do no harm" not apply when a bill is due?

Clearly the health care sector in their new found debt business is so out of control, the IRS has issued new rules to get tax-exempt health care facilities to clean up their debt collections act:

The proposed rules, issued June 22 by the IRS, would apply to the nearly six in 10 U.S. hospitals that operate as tax-exempt, nonprofit charitable hospitals. They would be required to provide additional consumer protections and services to patients who qualify for charity care and medical financial aid. If finalized, the rules would bar the hospitals from using the most aggressive debt collection tactics against low-income patients who don't pay their medical bills.

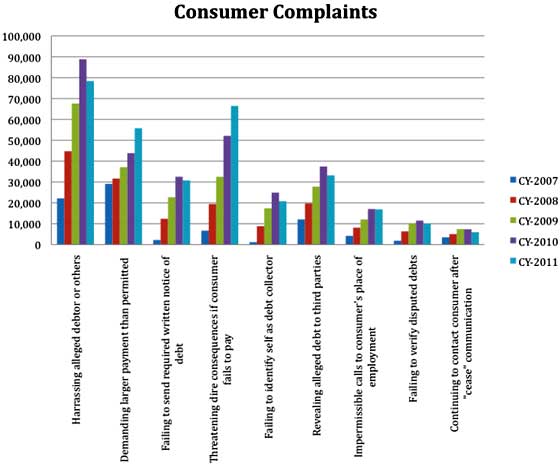

The CFPB has some startlingly statistics on debt collections in their annual report. Anyone who has been harassed by a debt collector should read this report for many goings on these days are actually illegal.

In 2011, approximately 30 million individuals, or 14 percent of American adults, had debt that was subject to the collections process.

Below is a chart on the types of complaints the FTC gets on debt collection agencies.

Of course here comes the WTO, out to rip asunder our national laws, under the guise it's somehow trade.

The greater significance of the ruling is in the precedent that it sets of a WTO member being willing to tackle another member's financial policies. Those of us who have raised the alarm about the conflict of the WTO's services agreement with financial regulation have often been told not to worry... that diplomatic restraint would keep a case from ever being launched. Even if launched, the WTO's institutional interests would keep it, the argument went, from ruling against a nation's policies.

Today's ruling totally undermines both aspects of this argument.

Today there is a bill in the Senate, the Medical Debt Responsibility Act, that will stop debt collections agencies from reporting medical bills on credit reports if the debt is actually paid. Folks, we need this bill to pass. This is outrageous to allow our health care sector turn into a bunch of debt selling collectors, ruining people's credit over $100, $200, $500 dollars when that bill has been paid.

Here's what the CFPB head, Richard Cordray said on the credit reporting agencies.

Many people’s credit ratings have taken a hit and now they are having a tough time regaining their financial footing. They are blocked from obtaining access to the credit that is often so essential to meaningful opportunity – to get an education, start a business, or buy a house.

Here are the CFPB areas of credit reporting focus, initially.

First, our oversight of the credit reporting companies will help us make sure that the information provided to them is itself reliable. Lenders and others who furnish information to the credit reporting companies are legally required to have policies in place about the accuracy and integrity of the information they report – which includes identifying consumers accurately, correctly recounting their actual payment history, and keeping their information and recordkeeping in order. Otherwise, their sloppy work becomes the true source of harm to the consumer’s overall creditworthiness. We want to deepen our understanding of the recordkeeping and reporting practices by lenders and we want to see what the credit reporting companies can be doing to test and screen for the quality of information they receive.

Second, given the number of complaints we have already heard from consumers, and the findings reached in some (but not all) reports on the subject, we want and need to know more about the accuracy of how the credit reporting companies assemble and maintain the information contained in consumer credit reports. Accuracy is critical for consumers and for markets. We recognize that achieving such accuracy takes a great deal of discipline and effort, particularly for a company that is handling and processing a huge volume of information. But because of the increasingly significant role these reports are taking on in our financial lives, the collateral consequences of mistakes can greatly harm consumers. The wrong information may cause them to be denied a loan, to be charged a much higher interest rate, or to be passed over for a job, causing them serious economic hardship. And inaccurate credit reports also deprive lenders of essential information they need to assess credit risk properly.

Third, we are keenly interested in understanding more about the problems and frustrations that consumers tell us they encounter in trying to resolve disputes about the information contained in their credit reports. Some errors may be unavoidable even in the best of systems. But when consumers find what they perceive to be erroneous information in their credit reports, they should not be burdened by unreasonably laborious processes to get errors removed from their files. There are certainly valid reasons why a credit reporting company must conduct a reasonable investigation when a consumer disputes information, and follow the procedures outlined in the law. But the harm done by errors is borne above all by consumers, and they deserve straightforward, effective, and timely mechanisms for addressing disputed items.

Bottom line, the current situation with credit reporting agencies is untenable. Anyone claiming to be a creditor is somehow allowed to make a claim on your credit report. Yet you, the individual, try to get bogus information and claims off of your financial history, find it is next to impossible.

What people need to do is contact the CFPB, submit a complaint about medical bills being inaccurately listed on your credit report. You can get a free copy on your credit report here from the FTC. Truly, anyone who had any medical care knows insurance companies fire off multiple reimbursement notices and on and on. Meanwhile these unscrupulous medical practices are selling your bill for a cut to some unethical debt collections agency. In turn that agency is abusing credit reporting by posting these debts to your credit report. It's outrageous and must be stopped.

Let's just hope something finally happens. Today, instead of putting a gun to people's head, a new weapon is used to threat and coerce. That's your credit score.

Comments

Punishments and deterrence will depend on size of offenders

Like everything else with America's law enforcement + regulatory regime, punishments and outcomes will depend on the size of the offenders. Like the SEC, CFTC, DOJ, Congress, and state AGs, the amount of protection given to consumers and the punishment given to offending banks, billers, and debt collectors will depend on the offender. If the offender is large enough to donate to Congressmen + have its own lobbyists, its own PR staff, and law firms staffed with former regulators, then it will be subjected to, at worst: 1) a few scripted moments in a Congressional hearing regarding billing and debt collection practices; 2)a wrist slap from the Protection Bureau; 3) a solemn promise to try to never do it again in the next 30 days; and 4) a fine that is a fraction of the profits gained from the infrations.

All smaller transgressors will face possible investigations and possible massive fines. In some cases when the Protection Bureau wants to appear like it actually enforces the law, it may bankrupt a very small shop and seek immediate headlines.

For example, examine the massive differences in how money laundering for violent cartels is prosecuted depending on whether it's done by individual suspects and small companies vs. large banks; trading with Iran is prosecuted whether it's done by an individual, a small firm, or a multinational (ranges from being labeled a traitor and going to federal prison + forfeiture all the way to a wrist slap and keeping profits); securities fraud with lifetime bans for individuals vs. minor wrist slaps for large firms by FINRA and the SEC; price-fixing small vs. large firms; commingling and theft of funds by a solo attorney or small brokerage vs. MF Global; etc. for precedent regarding the two standards.

The Cruel Facts about the Credit Bureaus

Had some problems with a creditor a year or so ago and let me tell you what I discovered after much frustration. As the economic populist has provided me some substantial insights, I spent some time on this.

First off, a reality check. The only REAL credit report you get is the free one recently mandated by law (see below link). Anything you buy from Experian, Transunion or Equifax has a clause in their 'contract' stating that the content of the purchased report may or may not reflect all the content in your ACTUAL credit report. If you compare the content of the free( ACTUAL) report with the on- demand purchased credit reports you might find they differ substantially.

Since at the time I was literally checking my credit every few days I found that the content of the purchased reports were changing over time. In particular you may find a whole host of unwanted organizations checking your credit. These will show up on the ACTUAL (once a year) report but not on your purchased report. In fact credit inquiries would appear on my purchased reports then vanish several days later on new reports.

RULES FOR DEALING WITH CREDIT BUREAUS (CB) / THE RULES

1. All correspondence must be done by certified mail (overnight express or return stub signature type). There is a statutory three day response period for the CB to reply to 'valid' issues.

Many of you may not be aware that basic certified mail (dark green label-cheap, they scan it in) no longer provides 'proof of delivery' for many large organizations. The online tracking will only show that the letter was mailed. I believe they are just dumping the basic certified mail at large banks and credit organizations without even scanning the signatures in. Your only actual proof of delivery will be if the letter is rejected and you receive it back. Most such large organizations have a post office at their facility. My attempts to obtain signatures using basic certified (the green sticker they place on the letter) were unsuccessful. If anyone thinks otherwise, please post your thoughts. I believe this is a major news story since it's been going on for years now.

2.Use the telephone only sparingly and NEVER EVER use the internet to contact a CB. Whatever few rights you have under US law are waived if you use the internet. Your screen-shots or printed online reports will be next to worthless in court or in any correspondence.

3.) If you have a complaint regarding a creditor, the credit bureau considers the listed account to be the 'property of the creditor'. The creditor can change its content at will at anytime (for instance you may close an account then several years later find it in default). Remember, the creditor pays the CB, and hence you are an unwelcome, pesky intruder to the proceedings. The CB does not certify the accuracy of the data, anymore than YouTube certifies its video content.

4)Don't waste your time contacting the Federal Trade Commission. They'll take a complaint but will do nothing about it since they do not act on the behalf of individual consumers. Their staff are nice but ignorant and you may receive false addresses and telephone numbers just to get you off the line. They seem completely unaware how the CBs operate. The FTC is a complete joke.

EXPERIAN – the worst of the worst. Consider it a criminal entity.

Experian purchased TRW and is a large multinational organization. It thus could care less about US laws. While Equifax and Transunion provide both telephone numbers and addresses, Experian will shut you down and lock you out if your problem is too complicated.

Prepare to have your phone routed to an operator-free phone tree if Experian decides you are too much trouble.

Experian only provides an address to contact them on the front of your once a year govt mandated free report. In order to accept your complaint in writing Experian requires a copy of your license or passport and several bills from your current address. The address is only valid for something like 30 or 60 days, then it changes.

When I used my one shot to contact Experian in writing I provided extensive documentation of criminal wrong-doing by a large bank. Guess what happened? They asserted the bills and passport I sent them were fraudulent and that if I contacted them again they would refer me to the FBI!

Hence with Experian you may end up being able to see your credit report via outside parties but be unable to do anything about the errors.

I suggest you first focus on Equifax then Transunion if you have any creditor issues. Both of these companies were responsive, though you'll find unreasonable anomalies with all of them.

There's More!

It gets even worse! I discovered from an attorney that it is not necessary for most financial organizations to even submit your account info to a CB in a timely manner. Hence you will not be able to dispute the content of the report until after it goes seriously into arrears.

A common tactic of credit card companies is to delete your account, threaten you by mail for money, then much later re-post all the negative data later after the account it sold.

See how clever that is? You can't complain to a CB about an account that isn't even listed! The end game is the defaulted account is sold off to a third party, who then sues you in state court. The original creditor is now absolved of any responsibility of dealing with you since they no longer own the account. Considered this a laundering of disputed accounts.

If you do go to court over the mis-information the Supreme Court mandated the most you can get from the falsely reported info is $1000+ attorney fees. That's a Scalia invention.

Hope the above helps someone.

Your real report is only available to you once a year at the below address. I suggest you have it mailed.

www.ftc.gov/bcp/edu/microsites/freereports/index.shtml

Thanks for the post, Driveby.

Thanks for the post, Driveby. Read and registered.

The business of fraud in this country know no limits.

Excellent Post as Always Robert

I recently was denied a new bank account over an old bank debt paid off 3 years ago. I have an account with the bank who they say I still owe money to! I have moved to a better economic climate so I needed a local bank.

I called the branch where I knew the asst manager and he affirmed that yes the debt was paid some time ago and gave me a number to their internal division where I could find out why it was suddenly reporting as unpaid. They started harassing me and asking where I worked, who my employer was (my business folded)etc. I asked if they were learning impaired since the conversation started with me explaining this was concerning a debt paid 3 years ago. They continued to harass so I called the asst manager back and asked that they send me a letter on their bank stationary with the details and contact info etc.

Hence I was able to open a local account but it still reports as unpaid. I cannot speak to anyone at the credit agency which is reporting that false info so it stands till the incompetents decide they will change it.

it's incredible, I suggest filing a complaint

with the new CFPB. Literally we are having not just identify theft run rampant, ruining people's credit, but false situations like you mention and it's happening everywhere.

It's no wonder people cannot get mortgages with these goings on. And the credit bureau's don't do anything either. Experian is like some sort of criminal enterprise as are the others. I mean literally, OWS has some exposure on them.

What I'm amazed is this post didn't get much traction and it really should. (consider sharing it around). Although there is so much outrageous stuff happening every day it's hard for people to keep track of it all.

HuffPo

Robert do you submit your posts to Huffpo as stories?

Some of these would garner a lot of attention in the right light and would draw more readership here. You pop up in Google News feeds for some of my watched topics.

I will post this on a few places where it will draw some eyes.

HuffPo and others

I don't cross post, mainly because this is EP site articles, for EP and we have ads running on EP. If I do that what's the point of EP? But sometimes stories get buried and this is one.

Understood

I was thinking more about you personally getting your views to a bigger audience. Most of the bloggers I read there post a link to their own blogs.

we could use more authors here

People disappear for various reasons, then, due to being a news source, for quality control, I had to change the site rules so author accounts are requested. We had people literally putting up a raw link as a "post", not exactly Journalism level quality writing there.

Possibly I should do that but it takes a lot of time just to write here so why stretch myself thin? I think it would be better if we could invite some great writers to come post here, who don't own their own sites.

But bottom line, The Economic Populist does get reasonable traffic. If you want to help promote certain articles, please do. Reddit it seems likes some of our stuff but reddit is it's own community, they for the most part discuss articles on the site itself, but hop over around the Internets to read the individual pieces.

I'd love to find more quality authors to contribute as well. If you see authors who have in depth, accurate articles, want more exposure, including cross posts, invite them and let me know. Reality is solid authors are few and far between with a hell of a lot of fluff and puff out there and that includes the major financial press.

Finally, I do periodically refute lobbyist bullshit snow. We've got it raining down on us in spades at the moment, on flooding the labor market with more foreign guest workers. Literally they are claiming there is a trucker shortage. Good freaking God, 28 million people needing a job and they are claiming there is a shortage. The training time to drive a semi is two weeks of classes and then some trucker in training initial runs. Out of 28 million people they cannot offer to train a few?

Stuff like this infuriates me, we are in such trouble as a labor force and this is the treatment we get, anybody but an American.

Shortage of Drivers

That's incredible about not training Americans.

I can't understand why Whirlpool moved nearly 100% of their manufacturing overseas and I can buy a washer and dryer made in Germany by union labor and shipped here but the US can't compete?

I see your point on the other and I have some time these days so I'll start promoting a bit - soft promotion to get some more eye balls here and posters.

Trucker "shortage" is a ruse to get Mexican trucks all over USA

Purely coincedental because companies and lobbyists and politicians never lie, but the "shortage" talk seems to be gathering weight at the same time the US DOT is allowing Mexican truck drivers to come further into the US under NAFTA. And wouldn't you know it:

"Supporters hail the agreement as an end to tariffs that have cost U.S. companies more than $2 billion. They say it will create thousands of jobs and spur trade between the two nations. SUPPORTERS [emphasis added] include top U.S. transportation officials, the nation's largest trucking industry trade association, businesses that export to Mexico and the U.S. Chamber of Commerce. . . Patrick Kilbride, the Chamber's senior director for the Americas, could not provide specifics on how jobs will be created. " USA Today from August 2, 2011.

It's sad when a PR tool cannot even back up his lie with another lie quickly. Surely an unemployed American could take Mr. Kilbride's job and do a better job, right? But perhaps honesty isn't wanted at the Chamber.

So "shortage" talk is just a way to get Mexican truck drivers to undercut American drivers. But if you ask those same people, Americans who cannot find jobs should just go to trucking school, or go to the oil fields in North Dakota, or become an engineer, or go to law school, or home health care, or something. No matter what field they recommend or what career they tell you is "wide open and booming," they will do everything they can to screw over American workers and those seeking work to undercut wages and replace Americans.

Golly, I sure hope Mexico isn't a major point of origin and transit nation for drugs and violent criminals seeking entry, because that would be a major threat to our national security, correct? DOT should really talk to DHS and the DOJ - they might have something to discuss. Are all Mexican drivers subject to tough licensing and regs just like we are? Hmmm . . .

So when our national security and economy is further threatened, don't go blaming the unemployed or your fellow struggling Americans, we know who to blame - include top U.S. transportation officials, the nation's largest trucking industry trade association, businesses that export to Mexico and the U.S. Chamber of Commerce. These people want the perks and money made on the backs of fellow Americans, they get the full blame. Enjoy.

America, it's being carved up for dinner by oligarchs and their puppets.