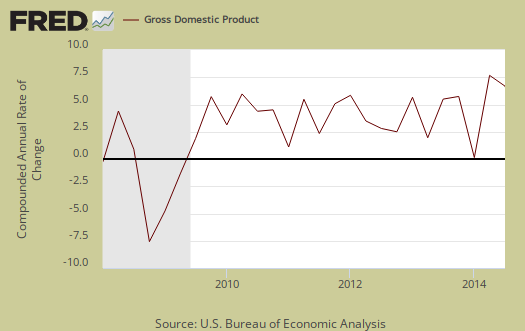

Third quarter 2014 real GDP came in at a strong 3.5%. This is the second quarter in a row for solid economic growth. Q1 showed a contraction Take a good look for Q3 GDP will be revised and we estimate strongly downward as imports come into the Census for tabulation. Private inventories contracted, hence investment was much less than Q2. Consumer spending was also tamer. Overall Q3 GDP was surprisingly solid.

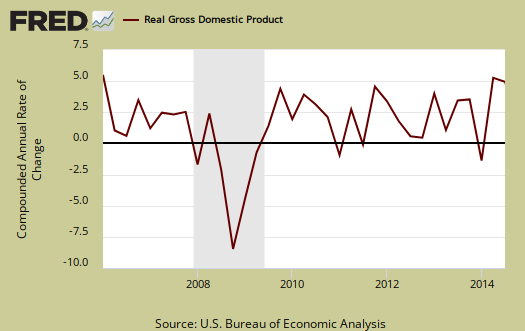

As a reminder, GDP is made up of: where Y=GDP, C=Consumption, I=Investment, G=Government Spending, (X-M)=Net Exports, X=Exports, M=Imports*. GDP in this overview, unless explicitly stated otherwise, refers to real GDP. Real GDP is in chained 2009 dollars.

This below table shows the percentage point spread breakdown of Q1 from Q2 2014 GDP major components and their spread.

| Comparison of Q3 2014 and Q2 2014 GDP Components | |||

|---|---|---|---|

|

Component |

Q3 2014 |

Q2 2014 |

Spread |

| GDP | +3.54 | +4.59 | -1.05 |

| C | +1.22 | +1.75 | -0.53 |

| I | +0.17 | +2.87 | -2.70 |

| G | +0.83 | +0.31 | +0.52 |

| X | +1.03 | +1.43 | -0.40 |

| M | +0.29 | –1.77 | +2.06 |

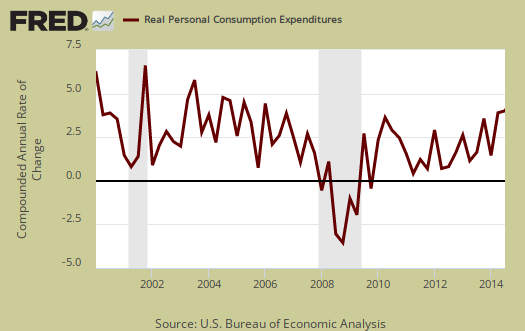

Consumer spending, C in our GDP equation was 34.5% of GDP. Durable goods were almost halved from last quarter with a 0.53 percentage point GDP contribution. In spending on services, Housing and utilities was a -0.21 GDP percentage point contribution which reflects the decreasing energy demand. Below is a percentage change graph in real consumer spending going back to 2000.

Graphed below is PCE with the quarterly annualized percentage change breakdown of durable goods (red or bright red), nondurable goods (blue) versus services (maroon).

Imports and Exports, M & X added 1.32 percentage points to Q3 GDP. Exports were 1.03 percentage points as imports was 0.29 percentage points indicating contraction. We believe the Census simply has not received and processed all of the import statistics for Q3 from trade data. This is a notorious delay in statistics. While the BEA does estimate with incomplete data, we've noticed an underestimate on imports in the GDP advance report. Regardless by how much, trade data will be revised. Revised imports could pull Q3 GDP an entire percentage point lower, although as of late domestic oil production has truly helped shrink the trade deficit.

Government spending, G contributed 0.83 percentage points to Q3 GDP. National defense spending increased 16%, causing Federal spending to give a 0.67 percentage point contribution to Q3 GDP. State and local government spending on the other hand only increased 1.3%. Below is the graph of government spending. With all of the political rhetoric blasting government spending, it helps to realize this spending adds to domestic economic growth.

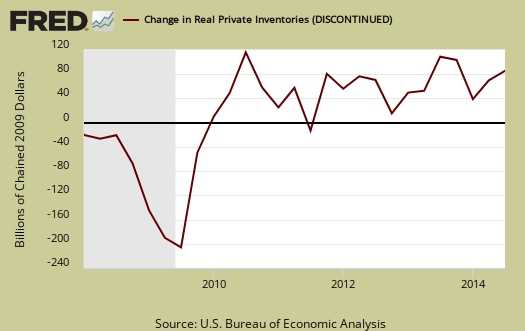

Investment, I is made up of fixed investment and changes to private inventories. Investment really leveled in comparison to Q2 and contributed only 0.17 percentage points to Q3 GDP. The change in private inventories alone contracted and gave a -0.57 percentage point contribution to Q3 GDP after a Q2 growth blowout. Below are the change in real private inventories and the next graph is the change in that value from the previous quarter.

Fixed investment is residential and nonresidential and added 0.74 percentage points to GDP. Nonresidential was 0.68 percentage points of GDP, with equipment being 0..41 percentage points. Nonresidential structures by themselves added 0.11 percentage points.

Residential fixed investment added only 0.06 percentage points to Q3 GDP. One can see the housing bubble collapse in the below graph and also how there is no meteoric recovery in terms of economic growth.

Nominal GDP: In current dollars, not adjusted for prices, of the U.S. output,was $17,535.4 billion, a 4.9% annualized increase from Q2. In Q2, current dollar GDP increased 6.8%. That is a couple of very good quarters.

Real final sales of domestic product is GDP - inventories change. This figures gives a feel for real demand in the economy. This is because while private inventories represent economic activity, the stuff is sitting on the shelf, it's not demanded or sold . Real final sales increased 4.2%. Q2 real final sales were 3.2%.

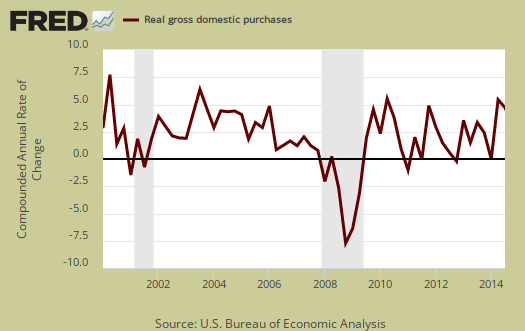

Gross domestic purchases are what U.S. consumers bought no matter whether it was made in Ohio or China.   ; It's defined as GDP plus imports and minus exports or using our above equation: where P = Real gross domestic purchases. Real gross domestic purchases increased 2.1%. Q2 was 4.8%. Exports are subtracted off because they are outta here, not available for purchase by Americans, but imports, as well a know all too well, are available for purchase at your local Walmart. When gross domestic purchases exceed GDP, that's actually bad news, it means America is buying imports instead of goods made domestically.

Below are the revised percentage changes of Q2 2014 GDP components, from Q1. There is a difference between percentage change and percentage point change. Point change adds up to the total GDP percentage change and is reported above. The below is the individual quarterly percentage change, against themselves, of each component which makes up overall GDP. Additionally these changes are seasonally adjusted and reported by the BEA in annualized format.

|

Q2 2014 GDP Component Percentage Change (annualized) |

|||

|---|---|---|---|

| Component | Percentage Change from Q2 | ||

| GDP | +3.5% | ||

| C | +1.8% | ||

| I | +1.0% | ||

| G | +4.6% | ||

| X | +7.8% | ||

| M | -1.7% | ||

Other overviews on gross domestic product can be found here,

logic behind inventories?

i understand that the change in the change in real private inventories is what is applied to the change in real GDP, but havent quite wrapped my head around the concept as to why...ie, real private inventories grew by an inflation adjusted $62.8 billion in the third quarter after growth of $84.8 billion in the 2nd quarter, and hence the $22.0 billion slower inventory growth subtracted 0.57% from GDP...still, i want to think that since inventories grew rather than shrunk, they should have added to GDP...what is the logic that makes postitive inventory growth in this case a subtraction from GDP, whereas positive growth in other forms of investment, such as equipment, will always add to GDP?

rjs

It isn't product until it is sold. As sales fall off, inventory

increases, because mfg is still happening.

If they stuff never sells, it can even become a liability.

imo

expect downward revisions to I & G

rjs

construction spending down

I said at the beginning GDP would be revised down on imports, but it has happened that other elements of GDP were revised up so significantly it wiped out the downward import effect.

My problem is the faux paus "intellectual property" and other modifications to GDP itself that occurred. How much fiction is that creating?

at least it aint hookers and blow...

it could be worse than just intellectual property...europe is including prostitution and drug dealing in their GDP figures..

the GDP technical note said that BEA assumed an increase in exports ex-gold and a decrease in imports ex gold, and that wholesale and retail inventories and nondurable manufacturing inventories had decreased in September...because of trade, WSJ says economists at BNP Paribas now track third-quarter GDP at 2.8% and J.P. Morgan forecasters think the rate will be revised to 2.9%, while the econ shops at Goldman Sachs, Royal Bank of Scotland, & Capital Economics think the rate will fall to about 3%....i'm not sure...imports of non-monetary gold were down $462 million, exports were up $740 million...i dont know how the BEA handles that..

rjs

trade will reduce GDP by 0.5 percentage points

I couldn't get to this today but as expected the trade revisions will pull down GDP.